AbbVie Inc.

CEO : Mr. Richard A. Gonzalez

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

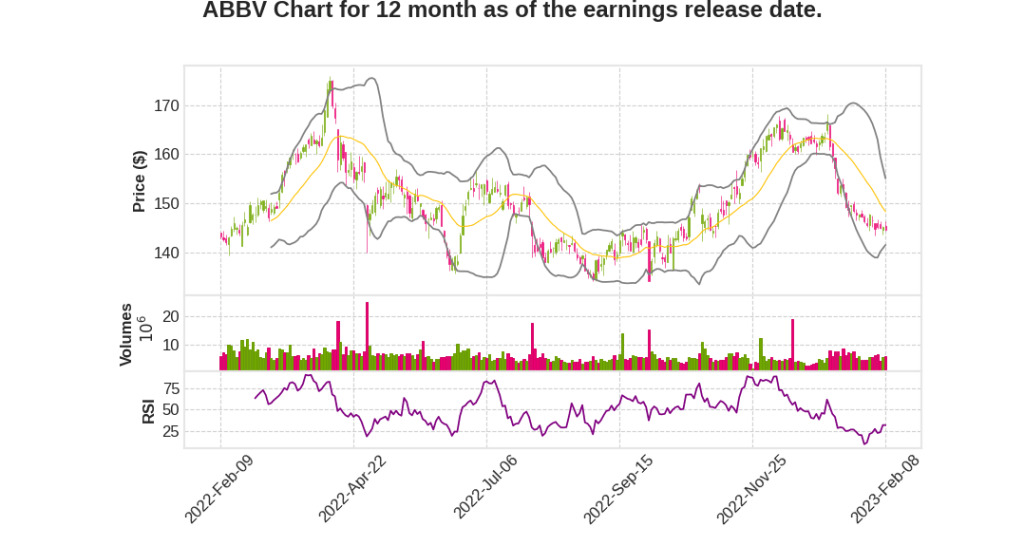

| 2022 Q4 | 1.6% YoY | 13.2% | -38.9% | 2023-02-09 |

Jeff Stewart says,

Immunology Segment

- SKYRIZI and RINVOQ delivered combined operational growth of 70% and contributed more than $2.3 billion in sales this quarter.

- SKYRIZI exceeded initial full year guidance by more than $750 million.

- SKYRIZI’s total prescription share of the U.S. biologic psoriasis market increased to more than 28%.

- RINVOQ’s global prescriptions are ramping nicely across all approved indications, including atopic dermatitis and ulcerative colitis.

- We are making excellent progress with the U.S. launch of SKYRIZI for Crohn’s disease.

HUMIRA Sales Performance

- Global HUMIRA sales were approximately $5.6 billion, up 6% on an operational basis.

- The U.S. performance showed 9.9% growth partially offset by a 16.9% operational decline internationally due to biosimilar competition.

- Broad formulary access for HUMIRA has been secured, encompassing more than 90% of all covered lives in the U.S.

Hematologic Oncology Segment

- Total revenues were $1.6 billion, down 11.2% on an operational basis.

- Imbruvica global revenues were approximately $1.1 billion, down 19.5% due to challenging market and share dynamics attributed to the pace of COVID recovery and increasing competition.

- Venclexta global sales were $56 million, up 12.2% on an operational basis, driven by robust share gains in the EU and Asia.

Neuroscience Segment

- Vraylar sales were up 15.5% on an operational basis, reflecting increasing market share, primarily in bipolar 1 disorder.

- Vraylar was recently approved as an adjunctive treatment for major depressive disorder, marking its fourth approved indication and adding a new substantial opportunity for growth.

- The oral CGRP portfolio contributed $249 million in combined sales this quarter, reflecting growth of nearly 30%, with strong prescription demand for both Ubrelvy and QULIPTA.

Future Launches

- ABBV-951 represents a potentially transformative next-generation therapy for advanced Parkinson’s disease and a $1 billion-plus peak sales opportunity. The launch is planned for later this year in the U.S., Europe, and Japan.

- QULIPTA is pursuing commercial approval in the U.S. as a preventative treatment for patients with chronic migraine.

Rick Gonzalez says,

Revenue Growth

- Total net revenues of more than $58 billion were up by 5.1% on an operational basis, driven by the growth of SKYRIZI and RINVOQ which generated nearly $7.7 billion of combined sales in 2022.

- SKYRIZI and RINVOQ are expected to exceed the peak revenues achieved by HUMIRA by 2027, with significant growth expected through the end of the decade.

Robust Pipeline

- AbbVie has a pipeline that includes more than 80 programs across all development stages.

- Several new products like venetoclax in multiple myeloma and MDS, epacritumab across B-cell malignancies and Teliso-V, a new treatment option in non-small cell lung cancer, will collectively support growth in the middle of the decade.

Financial Position

- AbbVie has maintained a strong financial position to fully invest in innovative science and commercial initiatives across their therapeutic categories to drive long-term growth.

- The company has also used that financial position to support a robust and growing dividend which has increased by 270% since its inception.

2023 Guidance

- Anticipated 2023 adjusted earnings per share of $10.70 to $11.10.

- Expected headwind from direct biosimilar competition with U.S. HUMIRA sales down approximately 37%.

- Robust performance from SKYRIZI and RINVOQ which are expected to collectively generate $11.1 billion of revenue.

- Revenue pressure in IMBLUVICA, partially offset by strong sales growth of venetoclax.

- Transient economic impact primarily in the U.S. on aesthetic procedure growth, affecting near-term performance for toxins, fillers, and body contouring.

Q & A sessions,

erm growth of the company, and we are in a position to drive strong growth with our current assets and pipeline. We have a low LOE exposure and have paid down the incremental debt from the Allergan acquisition, giving us more capacity for business development. We focus on therapeutic growth areas, including immunology, oncology, neuroscience, eye care, and aesthetics. We are active in business development and will continue to look for opportunities that can help us round out a category we are in. On the HUMIRA tail, we expect to see erosion in 2024, but a stable tail to develop in 2025 and 2026. HUMIRA’s decline in OUS markets is driven by different countries going biosimilar at different periods, leading to double-digit declines, but stability is expected in the long term.