Archer-Daniels-Midland Company

CEO : Mr. Juan Ricardo Luciano

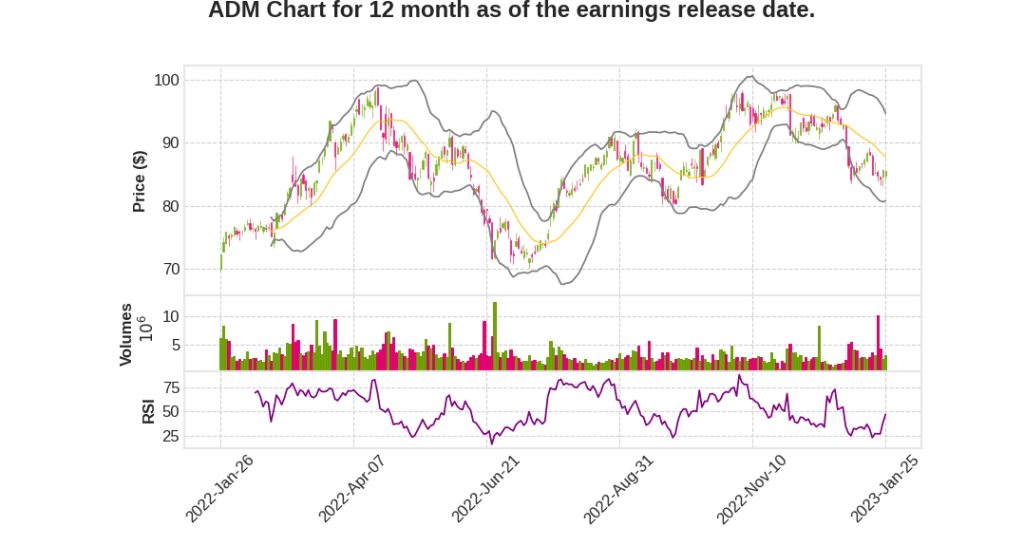

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 13.6% YoY | 0.1% | 33.4% | 2023-01-26 |

Vikram Luthar says,

Ag Services and Oilseeds

- Strong year-over-year Q4 results, partially offset by low North American export volumes

- Global trade results lower than prior year but benefiting from $110 million legal recovery

- Crushing results more than double prior year, with strong demand for soybean meal and renewable diesel

- Expect AS&O results for Q1 to remain strong, led by continued strength in crush margins and RPO

Carbohydrate Solutions

- Full year results higher than 2021, but Q4 results substantially lower due to pressured industry ethanol margins

- Starches and sweeteners sub-segment delivered much higher year-over-year results

- Expect continued solid demand and strong margins for starches, sweeteners, and wheat flour in Q1, but ethanol margins currently pressured due to high industry inventory levels

Nutrition

- Continued strong growth trajectory for full year 2022, with 18% constant currency revenue growth and 11% higher profits

- Q4 operating profits were significantly lower than prior year quarter

- Expect overall Nutrition results in Q1 to be lower than prior year’s record first quarter, primarily due to weaker margins in amino acids

- Expect Nutrition to continue on a positive growth trajectory for full year 2023, led by Human Nutrition and weighted in the back half of the year

Other Business

- Significantly higher Q4 results than prior year, driven by higher short-term interest rates and favorable underwriting results in captive insurance

- Higher unallocated corporate costs due to higher IT operating and project-related costs and higher costs in centers of excellence

- Expect corporate cost for 2023 to be around $1.5 billion, offset by higher Other business performance due to higher interest rates positively impacting ADM IS business

Financials

- Year-to-date operating cash flows before working capital up significantly versus same period last year

- Net debt to total capital ratio about 25%

- Plan to maintain capital expenditures at about $1.3 billion in 2023 and continue to have significant financial capacity

- Distributed $900 million in dividends and repurchased almost $1.5 billion of shares in 2022, planning $1 billion in opportunistic buybacks for 2023

Juan Luciano says,

Strong Q4 2022 Earnings Performance

- Adjusted EPS of $1.93 and adjusted segment operating profit of $1.7 billion in Q4 2022

- Full year adjusted EPS of $7.85 and adjusted segment operating profit of $6.6 billion in 2022

- Full year operating cash flow before working capital was $5.3 billion

Capital Allocation and Shareholder Returns

- $1.3 billion in capital expenditures and $2.3 billion return of capital to shareholders in 2022

- Announcement of a 12.5% increase in quarterly dividend to $0.45 per share

Operational Productivity Improvements

- 2022 productivity work included stabilizing plant operations and streamlining operating systems

- Multiple projects delivered to enhance operational footprint, modernization, maintenance, and capacity expansions

Innovation and Growth Initiatives

- Growth opportunities: sustainability, differentiated grain, alternative proteins, BioSolutions, microbial solutions, and microbiome modification

- Decarbonization a critical component of sustainability platform, reducing carbon intensity of assets and value chain

- Exploring opportunities around precision fermentation in microbial solutions

Future Outlook

- Robust plan for driving enduring value creation in 2023 and beyond

- Continued focus on productivity, innovation, and structural growth

Q & A sessions,

Expected Market Factors for Strong Performance

- Tight supply and demand balances in key products and regions

- Strong demand for vegetable oil, driven largely by robust demand for biodiesel and renewable diesel

- Resilient food demand driving higher volumes and margins in starches, sweeteners, and wheat milling

- Continued strong demand for ethanol, including positive discretionary blending economics

- Expected 10%+ constant currency OP growth from Nutrition

ADM’s Strong Playbook and Healthy Balance Sheet

- ADM has a strong playbook powered by deep expertise and unparalleled footprint and capabilities to manage a dynamic market environment.

- The company’s healthy balance sheet provides ongoing optionality as they continue to pull the levers under their control to deliver results.

- Positive contributions are expected from productivity and innovation initiatives across the company that will help drive value in 2023.

Continued Growth in Nutrition Business

- ADM’s nutrition business has been growing at a 20% CAGR over the last 3 years.

- The company continues to add layers of capabilities to win at the customer front.

- ADM expects bolt-on M&A and organic growth to continue, building capabilities and new capacity in 2022 that will be seen in 2023.

Strong Demand for Soybean Meal and Oil

- The demand for all oils is running harder than production globally, and renewable green diesel will have a huge pull in soybean oil.

- The meal market is growing and expected to require 20 million more tons of soybean meal by 2026, but ADM estimates only 15 million tons of supply on soybean meal.

- ADM sees this environment as highly supportive of strong and sustainable crush margins for many years.

Positive Outlook for Short-term and Long-term China Demand

- In the short-term, ADM sees China continuing to increase imports, driven by high domestic grain prices, low domestic vegetable oil stocks, and an increase in domestic pork prices.

- In the long-term, ADM sees China’s middle class increasing their protein consumption, still far from the level of consumption in the U.S., and the global population reaching 10 billion people by 2050.