The AES Corporation

CEO : Mr. Andres Ricardo Gluski Weilert

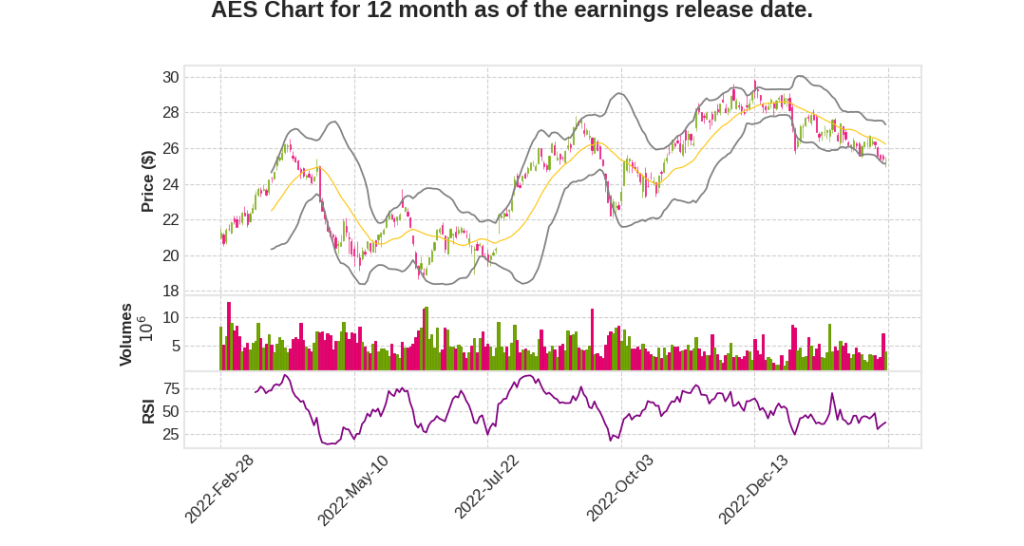

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 10.5% YoY | -1.7% | 42.1% | 2023-02-27 |

Steve Coughlin says,

Financial Performance in 2022

- Full-year 2022 adjusted EPS was $1.67 versus $1.52 in 2021, surpassing the guidance range of $1.55 to $1.65.

- Adjusted pretax contribution or PTC was $1.6 billion for the year, an increase of 149 million and a 11% growth over 2021.

- Lower PTC in the U.S. was primarily driven by the recognition of one-time expenses from previously deferred purchased fuel and energy costs at our utilities.

- Higher PTC at our South America SBU was primarily driven by our increased ownership of AES Andes and higher margins at both AES Andes and AES Brazil.

- Higher PTC at our MCAC SBU reflects the benefit from a large volume of LNG sales redirected to the international market.

Parent Capital Allocation

- Sources reflect 1.3 billion or total discretionary cash.

- Asset sales were below expectations for the year, but the company still expects to achieve its goal of $1 billion in proceeds by 2025.

- The company invested more than 700 million in growth at its subsidiaries, of which approximately two-thirds were in the U.S.

- The company allocated nearly 500 million of its discretionary cash to its dividend.

2023 Guidance and Expectations

- The company is initiating 2023 adjusted EPS guidance of $1.65 to $1.75.

- Roughly 65% of the new renewable capacity is located in the U.S, and the company expects to commission approximately 3.4 gigawatts of new renewables, which is the largest year-over-year increase in AES history.

- While the midpoint of the 2023 guidance range is below the company’s long-term annual growth target, AES is reaffirming the 7% to 9% growth rate through 2025.

- The company expects to see lower contributions from its MCAC SBU on a year-over-year basis, primarily driven by more than 200 million of adjusted PTC from LNG sales executed in 2022.

- The company expects lower margins at its Chile business this year, particularly in the first half of the year, which is a temporary impact of its Green blend and extend strategy to transition its customers from coal power to renewables.

Andres Gluski says,

Financial Results

- Adjusted EPS for Q4 2022 came in at $1.67, above the guidance range of $1.55 to $1.65.

- Strong performance across the portfolio, growth in renewables, and the benefit of embedded optionality in LNG contracts drove the accomplishment.

Construction Projects

- AES added around 2 gigawatts of new projects to its portfolio despite numerous market-wide challenges in 2022.

- Ability to execute is a source of competitive advantage contributing to long-term forecast.

PPA Signings and Pipeline of Future Projects

- AES signed 5.2 gigawatts of renewables under long-term contracts in 2022, increasing the backlog to 12.2 gigawatts.

- Pipeline of future projects increased by 25% to 64 gigawatts, including 51 gigawatts in the U.S.

- Expected to sign an estimated 14 gigawatts to 17 gigawatts PPA signings over the next three years.

Green Hydrogen and Regulatory Foundations

- AES established itself as a leader in green hydrogen and announced a partnership with Air Products to develop, build, own, and operate the largest green hydrogen production facility in the U.S.

- Developed strong regulatory foundations for future growth in the U.S. Utilities.

Guidance and Outlook

- Initiating adjusted EPS guidance of $1.65 to $1.75 for 2023 and reaffirming long-term growth rate of 7% to 9% through 2025 for both adjusted EPS and parent free cash flow of a base year of 2020.

- Expect to complete approximately 3.4 gigawatts of new projects, including 2.1 gigawatts in the U.S. in 2023.

Q & A sessions,

Optionality of Tax Credit Structures

- AES has the option to choose between Investment Tax Credit (ITC) or Production Tax Credit (PTC) for solar projects

- The tax credit structure that yields the highest return will be chosen for the project

Energy Community Adder

- Approximately one-third of AES’s pipeline is expected to qualify for the Energy Community Adder

- AES is competitively positioned to get at least the 40% level for this portion of the pipeline

Financial Performance for 2022

- AES surpassed its guidance range of $1.55 to $1.65

- Full-year 2022 adjusted EPS was $1.67 versus $1.52 in 2021

- Unplanned outages and several one-time expenses partially offset positive drivers

2023 Guidance and Expectations

- AES is initiating 2023 adjusted EPS guidance of $1.65 to $1.75

- Roughly 65% of new renewable capacity coming online this year is located in the U.S.

- Tax credits are an important component of AES’s renewables business earnings and cash flow

- 2023 growth rate is lower than the long-term trend due to conservative approach in modeling, lower MCAC SBU contributions, and lower margins at Chile business

Parent Capital Allocation Plan for 2023

- Parent free cash flow for 2023 is expected to be $950 million to $1 billion

- AES plans to invest approximately $1.7 billion toward new growth, with two-thirds allocated in the U.S.

- AES plans to allocate approximately $500 million to its shareholder dividend