Amcor plc

CEO : Mr. Ronald Stephen Delia B.Sc., MBA

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

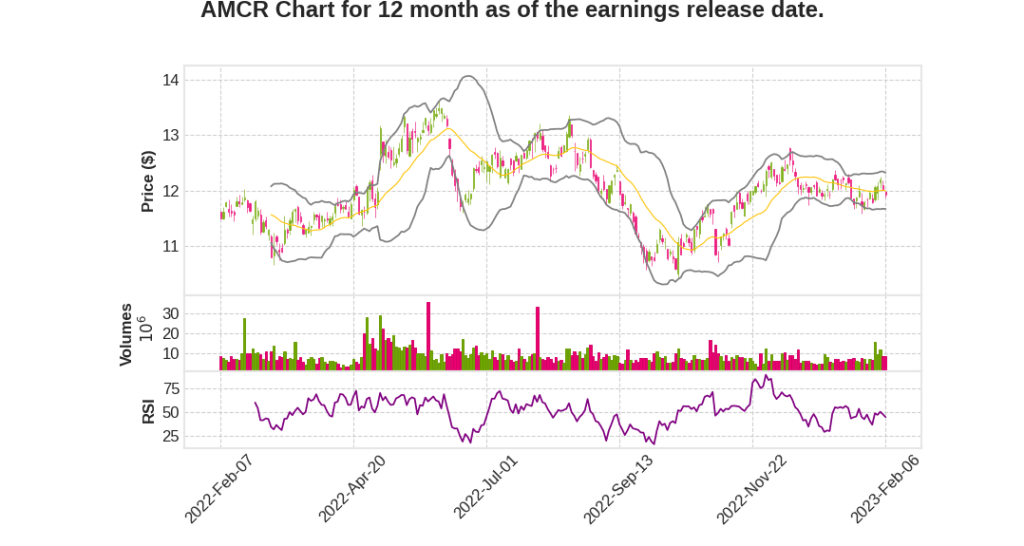

| 2023 Q2 | 3.8% YoY | 68.4% | 109.5% | 2023-02-07 |

Michael Casamento says,

Flexibles Segment

- Reported first half sales grew 5%, which included recovery of higher raw material costs of approximately $460 million, representing 9% of growth.

- Sales grew 3% for both the first half and December quarter, driven by favorable price mix benefits of 4%, partly offset by modestly lower volumes.

- Sales across higher-value priority segments remained strong, collectively growing at high single-digit rates through the first half and contributing to positive price/mix.

- Strong growth in businesses in India and Southeast Asia, particularly in health care and media end markets, helped limit the impact of lower volumes in some business units across categories.

- Margins remained strong at 12.6% despite the 120-basis-point dilution related to increased sales dollars associated with passing through higher raw material costs.

Rigid Packaging Segment

- First half sales increased by 12% on a reported basis, which included approximately $210 million or 13% of sales related to the pass-through of higher raw material costs.

- Organic sales declined by 1% for the half, reflecting 2% lower volumes, partly offset by a 1% price/mix benefit.

- Overall volumes declined by 5% in the December quarter, with the beverage business in North America and Latin America impacted by lower consumer demand and customer destocking.

- The Specialty Containers business delivered good performance with solid volume growth from health care, dairy, and nutrition end markets.

- Adjusted EBIT for the Rigid segment in the first half increased 7% on a comparable constant currency basis with our teams being able to adjust to evolving market conditions and improve operating cost performance.

Cash on the Balance Sheet

- Adjusted free cash flow for the December quarter was $338 million, in line with last year.

- Cash outflow of $61 million for the half-year was lower than last year, largely reflecting the unfavorable impact on the working capital cycle related to higher levels of inventory and higher raw material costs.

- The company repurchased $40 million worth of shares in the December quarter and expects to repurchase up to $500 million in total through the 2023 fiscal year.

Outlook

- The company is maintaining its guidance range for adjusted EPS of $0.77 to $0.81 per share, assuming current foreign exchange rates prevail through the balance of the year.

- The company expects earnings growth of approximately 3% to 8% on a comparable constant currency basis, comprising approximately 5% to 10% growth from the underlying business and a benefit of approximately 2% from share repurchases; partly offset by a negative impact of approximately 4% related to higher estimated interest and tax expense.

- The company expects a negative impact of approximately 3% related to the divestiture of its three plants in Russia.

Ron Delia says,

Key Messages

- Amcor delivered a strong first half and second quarter despite ongoing challenges in the macroeconomic environment.

- 95% of Amcor’s portfolio is exposed to consumer staples and health care end markets, which positions the company well through economic cycles.

- Amcor reaffirmed their guidance ranges for fiscal ’23 but expects to be toward the lower end of their EPS guidance range due to the demand outlook becoming increasingly volatile.

- Amcor remains focused on executing against their strategy for long-term growth, which supports their compelling investment case.

Financial Highlights

- First half reported net sales were up 6%, which includes approximately $670 million of price increases related to higher raw material costs.

- Excluding the impact of raw material costs, organic sales were up 2% on a constant currency basis, and volumes were 1% lower.

- Positive price/mix performance more than offset modestly lower overall volumes, reflecting generally softer and more volatile demand as well as customer destocking in parts of the business.

- The business delivered an 8% increase in both adjusted EBIT and EPS for the first half.

- Reported net sales growth for the December quarter was 4%, and 1% on an organic basis. Adjusted EBIT and EPS each grew 7%.

- Amcor returned approximately $400 million of cash to shareholders through a combination of dividends and share repurchases in the first half.

- Amcor’s return on average funds employed is at 17%, and the company has increased planned repurchases for fiscal ’23 by up to $100 million.

Q & A sessions,

Health care segment

- Global health care packaging business with more than $1.8 billion in annual sales covering both Flexible and Rigid Packaging formats and evenly split between medical device and pharmaceutical packaging.

- Health care is a strong contributor to Amcor’s growth profile from both a volume and mix standpoint.

- Amcor is investing to capture more growth by localizing thermoforming production in Europe and opening a dedicated health care greenfield plant in Singapore.

- The recent acquisition of Shanghai-based MDK enhances Amcor’s leading position in the broader Asia Pacific medical packaging market by adding product capabilities and a complementary customer base.

Sustainability

- Amcor is well positioned as a leader in the industry in package design with nearly 100% of their rigid packaging and specialty cartons products and more than 80% of their flexibles products designed to be recycled or have a recycle-ready alternative.

- Amcor is increasing their long-term off-take commitments to meet ongoing demand for more recycled material and to support infrastructure and technology development.

- Recently announced partnerships with ExxonMobil and Licella provide another point of differentiation and value, which can be applied across all end markets.

Volume outlook

- The demand outlook for the second half is volatile and cautious with mixed volumes in October and November, a softening in December, and some improvement in January.

- The swing factor for maintaining the guidance range will be volumes, which could be anywhere from up a couple of points to down low single digits.

- Cost savings activities and offsets to the divestment of the Russian earnings underpin the outlook that Amcor has reaffirmed.