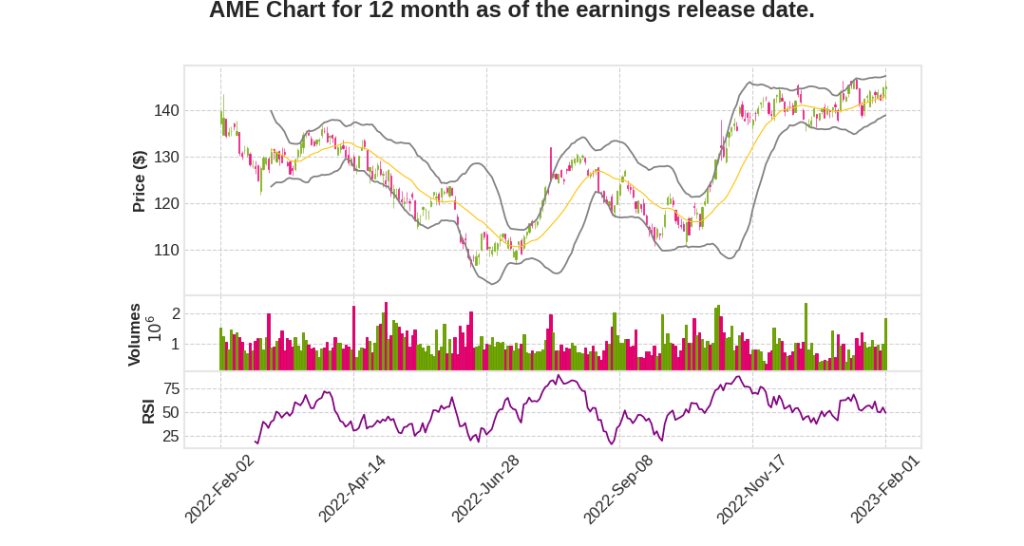

AMETEK, Inc.

CEO : Mr. David A. Zapico

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 8.1% YoY | 10.2% | 9.8% | 2023-02-02 |

Dave Zapico says,

Strong Q4 and Full-Year Results

- Q4 sales grew by 8% and organic sales grew by 9%

- Operating income and EBITDA for the quarter were both records

- Full-year sales increased by 11%, operating income increased by 15%, and EBITDA increased by 15%

- Overall and organic sales for 2023 are expected to be up mid-single-digits compared to 2022

Exceptional Performance Across Business Groups

- The Electronic Instruments Group had sales growth of 10% and operating income of $307 million in Q4

- The Electromechanical Group had organic sales growth of 8% and operating income of $115 million in Q4

- Both groups reported impressive operating margins that were up from the prior year

Strong Organic Growth and Investments in Growth Initiatives

- Organic growth initiatives were successful across businesses

- Investments in research, development, and engineering, and sales and marketing are expected to increase by $90 million in 2023

- The Vitality Index was an outstanding 27% of sales in 2022

- Zygo and its partnership with the Lawrence Livermore National Laboratory’s National Ignition Facility was highlighted as an example of innovative advanced technology solutions

Supply Chain Issues and Inflation Management

- Improvements in the global supply and logistics are being seen

- Inflation remains elevated but improvements compared to 2022 are being seen

- The company is confident in its ability to offset inflation with price increases and proactively manage its supply chain

Confident Outlook for 2023

- Record backlog and proven operating capability support outlook for 2023

- Overall and organic sales for 2023 are expected to be up mid-single-digits compared to 2022

- Diluted earnings per share for 2023 are expected to be in the range of $5.84 to $6, up 3% to 6% compared to 2022

- Q1 sales are expected to be up mid-single-digits with adjusted earnings up 4% to 7% versus the prior year

Bill Burke says,

Financial Highlights and Guidance

- Record level operating performance and high quality of earnings in Q4 and FY2022

- Flat G&A expenses in Q4 compared to the prior year, while for FY2022 G&A expenses were up $6 million, primarily due to higher compensation costs

- Anticipated modest increase in G&A expenses for 2023 compared to 2022 levels, remaining at approximately 1.5% of sales

- Effective tax rate in Q4 was 18.9% and expected to be between 19% and 20% for 2023

- Capital expenditures were $58 million in Q4 and expected to be approximately $114 million for 2023, or about 2% of sales

- Expected depreciation and amortization to be approximately $325 million in 2023

- Operating working capital was 18.9% of sales in Q4

- Cash flow in Q4 was excellent, with operating cash flow of $385 million, up 37% versus Q4 2021

- Total debt at year-end was $2.39 billion, down from $2.54 billion in 2021

- Gross debt-to-EBITDA ratio at year-end was 1.2 times and net debt-to-EBITDA ratio was 1.1 times

- Well-positioned for growth initiatives with strong financial position, proven growth model, and world-class workforce

Q & A sessions,

Geographical Outlook

- Strong broad-based growth across most geographies, with Europe up 12% and the US up 10% organically.

- Asia was flat due to China headwinds, with notable strength in aerospace and defense and process, while China was down low double digits.

- China situation is expected to turn around in the second half of 2023 as the reopening occurs.

Market Segments Summary

- Process businesses were up high single digits in Q4, with organic sales up 10%, and growth expected to be up mid-single digits for 2023.

- Aerospace & Defense businesses had a very strong finish to the year, with overall and organic sales up mid-teens.

- Power & Industrial businesses were up high single digits in Q4, with mid-single-digit organic growth expected for 2023.

- Automation & Engineered Solutions market segment had overall sales up low-single digits in Q4, with mid-single-digit organic sales expected for 2023.

Orders and Backlog

- Overall orders were up 1.5% in Q4, with a 10th straight positive book-to-bill quarter and an all-time record backlog of 50% of annual sales.

- Expectation of customers returning to more normalized ordering patterns as the supply chain is improving.

2023 Outlook

- Expect to grow in each quarter of the year, with about four points of price and 3.5 points of inflation offset by about 50 basis points.

- Supply chain shortages are expected to abate in 2023.

- Expect longer cycle aerospace and defense businesses to be a bit stronger than the balance of the portfolio.

Market and Growth Opportunities

- Healthcare, semiconductor, research, and oil and gas are expected to continue doing well in the future.

- Expecting a bigger pipeline than historically due to less money around the system to bid up deals.

- Disciplined acquisition process with deals meeting traditional financial hurdles and providing strong returns on the capital deployed.