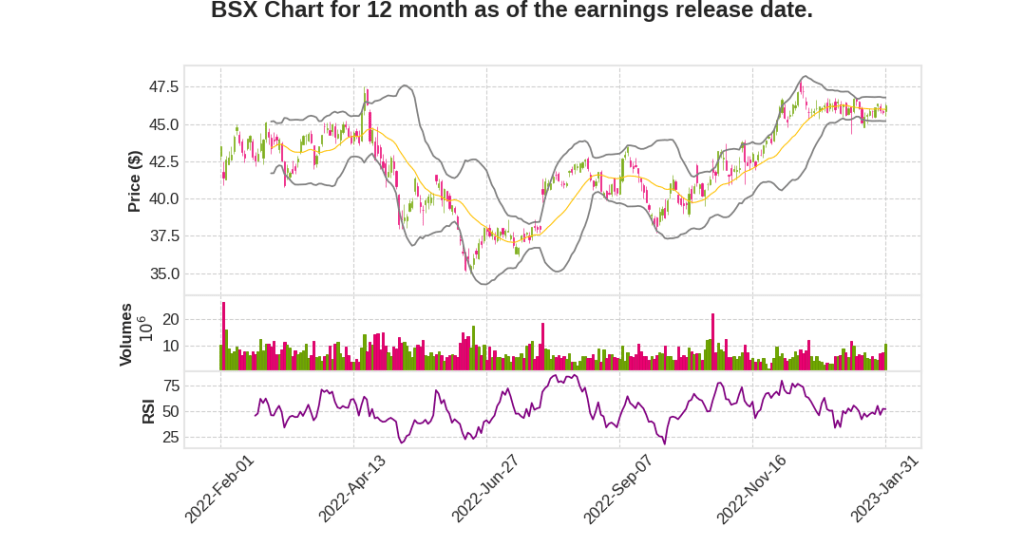

Boston Scientific Corporation

CEO : Mr. Michael F. Mahoney

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 3.7% YoY | 192.2% | 50.0% | 2023-02-01 |

Mike Mahoney says,

Q4 2022 Earnings Report Summary

- Excluding the one-time Italy reserve, growth is at +9%

- High-end sales and EPS

- Delivered top-tier revenue growth

- Improved margins in 2022

2023 Guidance

- 6%-8% guidance for the full year

- Expect a little bit of a headwind on the CRM side

- China is expected to deliver excellent double-digit growth but potentially not as fast as in ’22

Dan Brennan says,

Macroeconomic environment and Headwinds

- The 375 headwind seen in 2022 is expected to remain similar in 2023 due to the macroeconomic environment.

- The supply chain organization has been high-performing and is expected to continue to be so.

Analysis of 2023

- The annual operating plan process and guidance preparation process have detailed the analysis of 2023.

- The supply of materials and the cost of materials is still uncertain and choppy.

- Freight costs are expected to be less as fuel prices and oil prices are coming down.

- The direct labor piece is expected to annualize in 2023.

Prudent Guidance

- The guidance in February assumes a similar headwind to last year for a prudent course.

- The macroeconomic help in 2023 is uncertain, and there is no expectation of getting a lot of it.

- It would be great to get help, but it is best to prepare without it.

Q & A sessions,

Strong Performance of Urology and Endoscopy Businesses

- The urology business has shown strong global performance and is growing faster in the US, with extensive investments made in commercial, R&D, and acquisitions.

- Endoscopy is also expected to have similar results over the next few years, and the integration of Lumenis has been successful.

Headwinds and Tailwinds for Margin Improvement

- Headwinds include a tougher comp than normal, lower growth in China, and CRM growth more in line with the market in 2023.

- Tailwinds include strong momentum across businesses, potential growth in EP in Europe and Japan, and the success of products like WATCHMAN and ACURATE neo2.

- The company expects to have a strong year in EP, depending on when cryo gets approved in the US.

Growth and Market Share of WATCHMAN

- WATCHMAN grew 24% for the full year, and the company expects 25% growth in 2023.

- The procedure is profitable for hospitals and has a leading platform, and the next-gen WATCHMAN platform is expected to come out in about a year.

- ACURATE neo2 is doing extremely well in Europe and is expected to be approved in the US in 2024.

Potential Impact on P&L

- The company expects a 6-8% healthy top line, with leverage opportunities throughout the P&L.

- Gross margin may have a slight headwind from FX, but the company still expects it to increase through volume improvement programs and R&D efficiencies.

- The goal is to have a 50 basis points contribution to the P&L on top of the 2022 results, excluding the Italian sales reserve.