Centene Corporation

CEO : Ms. Sarah M. London

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

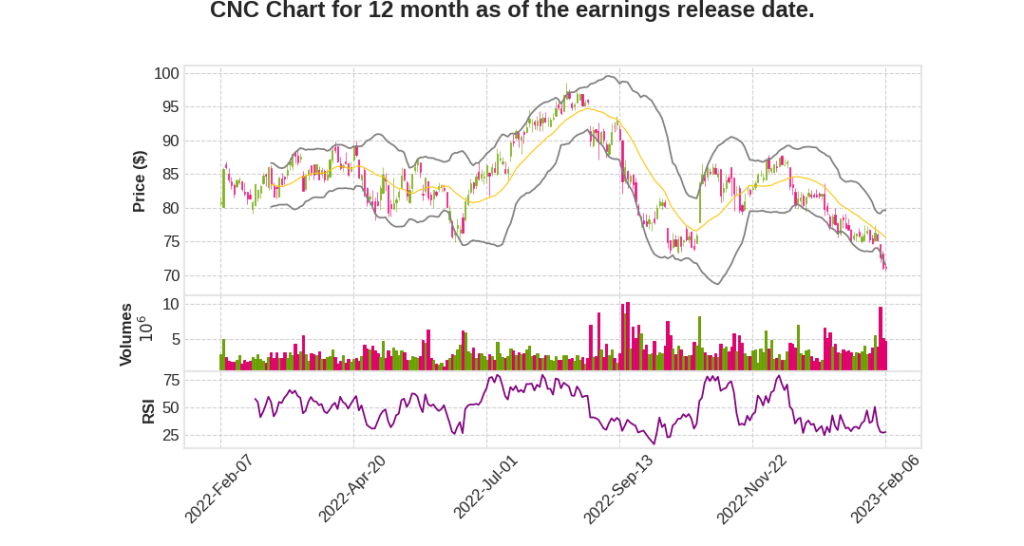

| 2022 Q4 | 9.2% YoY | -50.7% | -136.9% | 2023-02-07 |

Andrew Asher says,

Revenue Growth and Earnings

- Total revenue grew by $3 billion compared to the fourth quarter of 2021, driven by strong organic growth throughout the year.

- Adjusted diluted earnings per share of $0.86 in the quarter and $5.78 of adjusted EPS for the full year.

Medicaid and Medicare Membership Growth

- Strong organic growth throughout the year in Medicaid, primarily due to the ongoing suspension of eligibility redeterminations.

- Strong Medicare membership growth, and Medicare at 86.2% for the full year was 90 basis points better than 2021.

Commercial HBR Reduction and SG&A Expenses

- Commercial HBR was reduced by 550 basis points for the full year, driven by disciplined pricing actions and cost reduction initiatives executed in 2022.

- Adjusted SG&A expense ratio was 9.3% in the fourth quarter compared to 8.7% last year, driven by the inclusion of Magellan and increased Medicare marketing and value-creation investment spending in the quarter.

Cash Flow and Debt Reduction

- Cash flow used in operations was minus $1.6 billion in the fourth quarter, and cash flow provided by operations was $6.3 billion for the full year.

- Debt at quarter-end was $18 billion, down approximately $800 million from prior year-end, driven by senior note repurchases, and the debt-to-adjusted EBITDA came in right at 3.0x, down from 3.5x a year ago.

2023 and 2024 Revenue and EPS Guidance

- 2023 premium and service revenue should be approximately $2 billion higher than the range provided at Investor Day.

- While 2023 adjusted EPS guidance range of $6.25 to $6.40 remains unchanged, recent insights bias the company to the top half of the range.

- The company remains committed to its previously provided adjusted EPS floor of at least $7.15 for 2024, and despite the challenges in Medicare Advantage, the company aims to achieve this adjusted EPS.

James Murray says,

Impact of Proprietary Distribution Channels

- Using proprietary distribution channels has led to a reduction in complaints to CMS and lower disenrollments in the first 1.5 months of 2023

Improvement in STAR and RAF Scores

- The stability of the existing membership is expected to lead to improvement in STAR and RAF scores, which will help the overall margin profile going forward

Importance of Member Relationships

- Creating a relationship with members and explaining the benefits of the system has resulted in favorable results

- Building long-term stability of membership retention is a key focus

Q & A sessions,

PBM RFP and Investment Income

- Expecting significant tailwind from PBM RFP starting 1/1/24

- Investment income expected to be strong and continue into 2024

Marketplace and Share Buyback

- Marketplace to be larger than originally anticipated in 2024, with a positive margin position

- Expect a few billion in share buyback in late 2023, back-weighted for ’24

Medicare and Medicaid

- Medicare to be a significant headwind due to STARS and advanced notice

- Expect Medicaid HBR to experience pressure from redeterminations but have prepared for it

STARS Improvement

- Implemented steps to address issues with CTMs and disenrollments

- Positive impact on STARS expected to be seen in 2026 revenue

Value-Creation Plan

- Expect momentum in third year of value-creation plan