AT&T Inc.

CEO : Mr. John T. Stankey

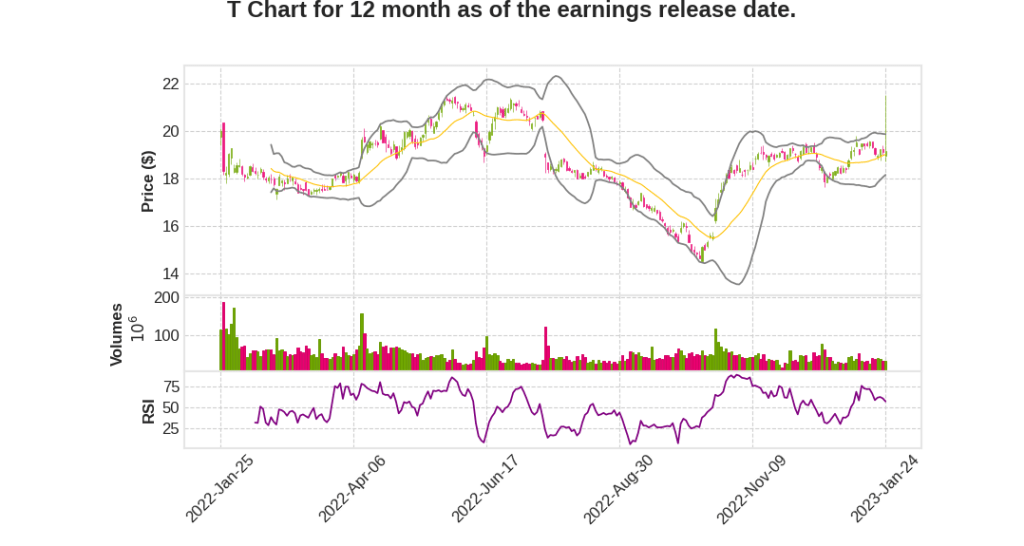

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -23.5% YoY | 3.0% | -563.8% | 2023-01-25 |

John Stankey says,

Wireless growth

- Delivered 656,000 postpaid phone net adds in Q4 2022 and nearly 2.9 million for full year

- Increased postpaid phone base by nearly 7 million to 69.6 million subscribers

- Improved postpaid phone ARPU by nearly $1 over the past 2.5 years

5G Expansion

- Reached 150 million mid-band 5G POPs, more than double the initial 2022 year-end target

- Expect to reach more than 200 million people with mid-band 5G by the end of 2023

Fiber focus

- Had more than 1.2 million AT&T Fiber net adds in 2022

- Fifth straight year with more than 1 million AT&T Fiber net adds

- Now at an inflection point where fiber subscribers outnumber non-fiber DSL subscribers

Cost transformation

- Achieved more than $5 billion of $6 billion plus cost savings run rate target

- Expect benefits of cost transformation to increasingly fall to bottom line in 2023

Balance sheet

- Reduced net debt by about $24 billion in 2022

- Commitment to providing an attractive annual dividend remains firm

David Barden says,

Impact of Industry Normalization on AT&T

- High correlation between 9 million postpaid phone nets a year and resuscitated growth of AT&T over the last 10 quarters.

- Pension to disproportionately assume that a tide that goes out on industry growth will be disproportionately allocated to AT&T.

- The impact of industry normalization on AT&T and whether it is realistic.

Copper Decommissioning and Fiber Initiative

- Copper decommissioning is a huge topic in markets like Canada where they have widely overbuilt their copper plant.

- The timing and magnitude of the benefits from copper decommissioning and fiber initiative.

- Whether it is too early to start talking about this as a tailwind in something like ’24 or is it really with us?

Q & A sessions,

Geopolitical and Economic Factors

- The company has taken a conservative stance in its guidance for Q4 2022 due to the unstable geopolitical environment and economic pressures.

- The company expects to continue dealing with pressures in areas such as energy, wage and employment, and longer-term contract renewals.

- The swing factor for the company’s performance is a significant and unforeseeable geopolitical disruption.

Capital Deployment and Return Characteristics

- The fiber portfolio is viewed as a portfolio of options for capital deployment where the return characteristics are most optimal.

- The Gigapower announcement is a new model that the investor base is unfamiliar with, and the company will provide 12 months of penetration information to demonstrate acceptable returns.

- The company intends to balance out return characteristics through the Gigapower initiative and capacity coming in from out-of-region builds that are subject to BEAD funding, which may have a different return profile.

- The company sees fixed wireless as a tool in the toolbox for areas with less densely populated areas, where it makes sense to deploy it as an acceptable substitute for fiber deployment.

Market Performance and Health

- The company dismisses the thesis that the market structure and function today is different from its performance over the last 2.5 years and believes that the industry is healthier than expected.