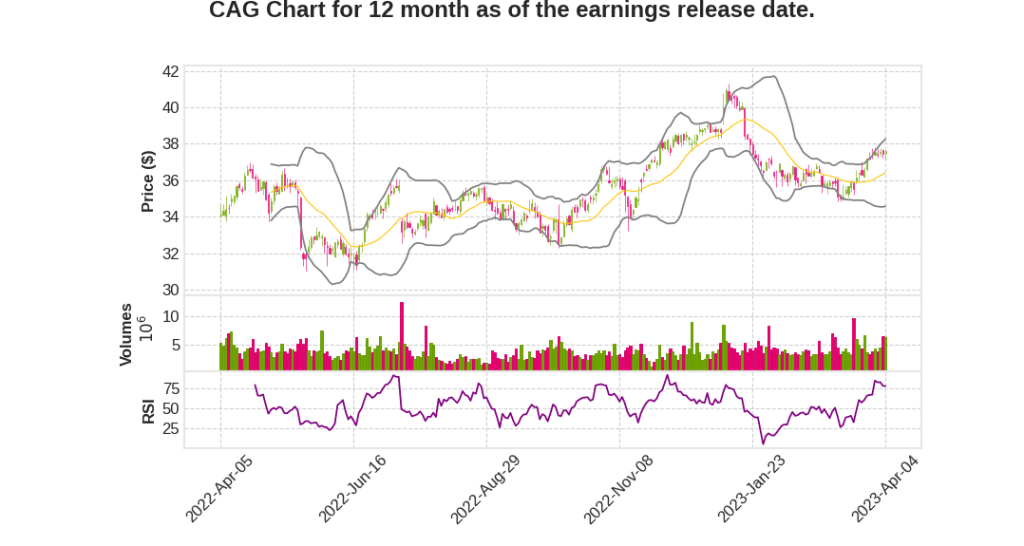

Conagra Brands, Inc.

CEO : Mr. Sean M. Connolly

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | 8.3% YoY | 34.2% | 38.6% | 2023-04-05 |

Sean Connolly says,

Margin Recovery and Pricing Strategy

- Margin recovery is the company’s top priority for FY23.

- They are focusing on inflation-justified pricing, supply chain improvements, and pruning low-margin volume.

- Q3 delivered a second consecutive quarter of strong gross margin recovery, with adjusted gross margin of 28.1%, a 409 basis point increase YoY.

- The company’s pricing execution is excellent, and elasticities remain muted and consistent.

Top Line Performance

- Organic net sales of $3.1 billion, a 6.1% increase YoY.

- Adjusted operating margin of 16.9%, a 321 basis point increase YoY.

- Adjusted EPS rose 31% to $0.76 per share.

- Retail sales grew by 5.5% compared to Q3 last year and 24.7% compared to three years ago.

Supply Chain and Manufacturing Disruptions

- Supply chain improvements are ongoing, and service levels are exceeding 90%.

- Manufacturing disruptions impacted certain categories, including canned meals and sides, canned pasta, canned beans, canned chili, canned meat, and fish products.

- Despite this, volume performance led near-end peers versus pre-pandemic baseline.

- The root causes of the disruptions have been largely resolved, and volumes are expected to rebound sequentially.

Domain Performance

- Frozen: strong retail sales growth on both a one- and three-year basis, improving 4% and 23%, respectively.

- Snacks: drove a 7% increase in retail sales compared to Q3 FY22 and a 39% increase over Q3 FY20.

- Staples: increased retail sales 7% compared to Q3 FY22 and 20% compared to the same period three years ago.

Guidance

- Organic net sales growth of 7% to 7.5%, adjusted operating margin of 15.5% to 15.6%. and adjusted EPS growth of $2.70 to $2.75.

- Confidence in the path ahead, moving past supply chain disruptions, and seeing improvements in sales trends.

Dave Marberger says,

Organic Net Sales Growth

- Organic net sales increased by 6.1% due to inflation-justified pricing and continued muted elasticities.

- 15.1% improvement in price/mix from inflation-justified pricing actions.

- Volume declined by 9%, and 8% of it was explained by Conagra’s favorable 0.54 elasticity factor. The remaining one percentage point volume decline is mostly from the supply chain disruptions.

Segment Performance

- Net sales growth across all four reporting segments with a 4.7% increase in net sales in the Grocery & Snacks and Refrigerated & Frozen segments.

- The International segment saw organic net sales up by 9.5%, but reported net sales were up by 7.7% due to the unfavorable impact of foreign exchange.

- The Foodservice segment grew by 17.3% in the quarter.

Adjusted Margin Bridge

- Strong margin recovery with a 10.9% margin benefit from improved price/mix during the quarter and realized a 1.8% benefit from continued progress on supply chain productivity initiatives.

- Continued inflationary pressure with 8% gross market inflation impacting operating margins by 5.9% and a negative impact of 2.8% from market-based sourcing.

- Higher investment in A&P and adjusted SG&A during the quarter reduced margins by 0.4% and 0.5%, respectively.

Adjusted Operating Profit and Margin by Segment

- Adjusted operating margin expansion in each segment despite some ongoing supply chain challenges.

- Total adjusted operating profit increased by 30.8% to $522 million during the quarter.

Fiscal ’23 EPS Guidance

- Raised fiscal ’23 EPS guidance and narrowed the ranges for organic net sales growth and adjusted operating margin with only one quarter remaining in fiscal ’23.

- Total gross inflation of approximately 10% for fiscal ’23 and expect gross inflation to continue for the full calendar year 2023.

- Net leverage ratio is expected to remain approximately 3.65x, and anticipate CapEx spend of approximately $370 million for fiscal ’23.

Q & A sessions,

Inflation and Pricing

- Navigating inflation cycles is predictable and mechanical.

- Conagra experienced a lag in Q2, but margins recovered as pricing caught up.

- Inflation-justified pricing, supply chain improvements, and value over volume strategy facilitated margin recovery.

Innovation and Growth

- Conagra plans to pursue sustained growth through innovation.

- Frozen performance was 100% driven by innovation and premiumization.

- Conagra will not pursue the opposite approach of the value over volume philosophy.

Q4 Guidance

- Conagra feels good about where they sit, and their plan is working.

- Supply chain is improving, but not all the way back, and they plan conservatively.

- Unit performance remains consistent, and elasticities remain benign.

Frozen Segment

- Conagra’s frozen business has sustained market share trends since 2016 despite the noise in the quarter and year-on-year deceleration.

- Pricing correctly in an inflationary environment and getting off legacy promotions drove the expansion in the frozen refrigerated segment.

- Scale and innovation are central to Conagra’s strategy to drive profit and margin improvement.

Net Sales and Margins

- Conagra delivered organic net sales of $3.1 billion in Q3, a 6.1% increase over the prior year period.

- Adjusted gross margin and operating margin increased significantly over the third quarter of last year.

- Conagra’s pricing execution is excellent, and elasticities remain muted and consistent.