CMS Energy Corporation

CEO : Mr. Garrick J. Rochow

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

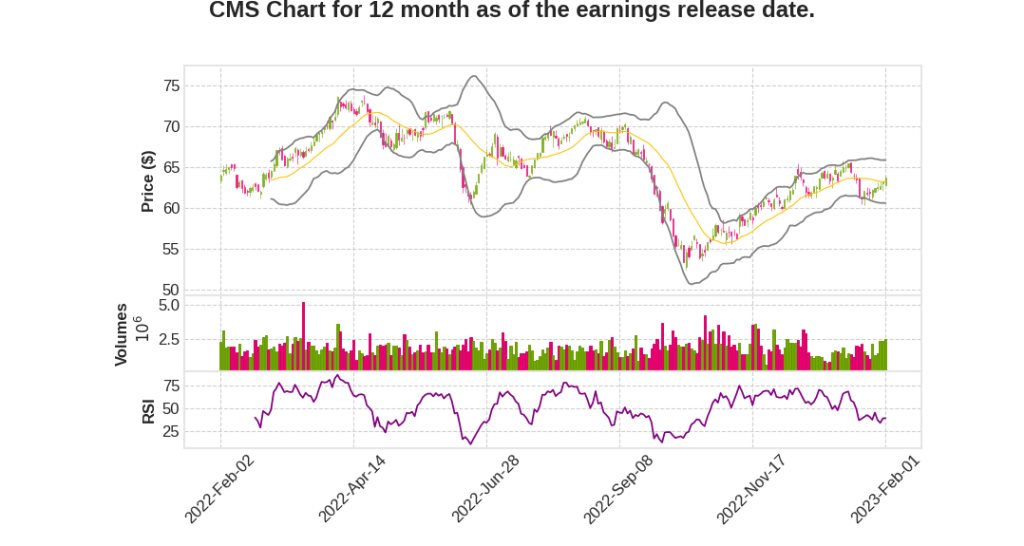

| 2022 Q4 | 12.1% YoY | 32.8% | -74.5% | 2023-02-02 |

Rejji Hayes says,

Financial Performance in 2022

- Adjusted net income of $838 million, which translates to $2.89 per share at the high end of guidance range

- Higher sales were driven by favorable weather and solid commercial and industrial load

- Higher expenses attributable to discrete customer initiatives, which reduce bills, support the most vulnerable customers, and improve the safety and reliability of the gas and electric systems

- $55 million of equity forward contracts settled as planned, and $440 million of equity forward contracts priced at a weighted average price of over $68 per share to address the parent company’s financing needs for the pending acquisition of the Covert natural gas generation facility

2023 EPS Guidance

- Raising adjusted earnings guidance to $3.06 to $3.12 per share from $3.05 to $3.11 per share

- EPS growth will primarily be driven by the utility and assume modest growth for NorthStar Clean Energy

- Normal weather amounts to $0.20 per share of negative year-over-year variance

- Anticipate $0.14 of EPS pickup attributable to rate relief, largely driven by recent electric and gas rate orders and the expectation of a constructive outcome in the pending gas rate case later this year

- $0.04 per share of positive variance attributable to continued productivity driven by the CE Way and other cost reduction initiatives

- $0.19 to $0.25 of positive variance versus 2022 stemming from usual conservative estimates around weather-normalized sales and nonutility performance, coupled with the benefits of significant reinvestment activity deployed in the fourth quarter of 2022 through regulatory filings and traditional operational pull ahead

Balance Sheet and Funding Needs

- Target solid investment-grade credit ratings and manage key credit metrics accordingly

- Settle equity forward contracts for the Covert financing in the second quarter of 2023 and have no additional planned equity financing needs until 2025

- Intend to resume our at-the-market, or ATM, equity issuance program in the amount of up to $350 million per year in 2025 through 2027

- Funding needs in 2023 are limited to debt issuances at the utility, a good portion of which has been priced and/or funded over the past several weeks

- The $825 million of utility bond financings addressed to date include the $400 million tranche of debt financing required to fund the acquisition of Covert in the second quarter

Garrick Rochow says,

Summary of CMS Q4 2022 Earnings Call Transcript

- CMS Energy reports another outstanding year operationally and financially, marking the 20th year of industry-leading financial performance, supporting their simple investment thesis that delivers for customers and investors.

- Net zero commitments backed up by a solid IRP provide certainty for investments in clean energy and highlight the supportive regulatory construct in Michigan.

- CMS Energy continues to lead the clean energy transformation by being best-in-class in the operation of their generating assets, saving customers roughly $560 million.

- CMS Energy sees significant growth in economic development, investing over $8 billion in Michigan, delivering more load growth, more jobs, and more investment, creating a strong future for the state.

- CMS Energy delivered adjusted earnings per share of $2.89 at the high-end of their guidance range, raising their 2023 adjusted full-year EPS guidance to $3.06 to $3.12 from $3.05 to $3.11 per share, compounding off of 2022 actuals, with a long-term dividend growth of 6% to 8%.

- The new five-year $15.5 billion utility customer investment plan supports safety and reliability investments in their electric and gas systems and paves the way to a clean-energy future when net zero carbon, methane and greenhouse gas emissions.

- CMS Energy has a long and robust capital runway with growth drivers outside of traditional rate base and expects incremental earnings provided by their non-utility business NorthStar Clean Energy.

- CMS Energy filed their gas case in December and will file their next electric rate case later this year with those outcomes providing further certainty for 2024 customer investments.

- CMS Energy is well positioned as it relates to the key sources of inflation including labor, materials, and commodities, with roughly $150 million in CE Way savings over the last three years and estimate over $200 million in large, episodic savings as PPAs expire and as they exit coal generation.

Q & A sessions,

Cost Reductions

- Assuming $45 million to $50 million of cost reductions due to CE Way

- Run rate now at about $45 million to $50 million due to pandemic-driven savings

- Anticipating savings from Kam 1 and 2

Non-Rate-Base Growth Drivers

- Energy waste reduction opportunities offer economic incentives

- PPAs will ramp up with more solar on contracted side attributable to IRP

- 10.7% ROE on renewable projects associated with RPS of Michigan

- Additional contribution from North Star

- Expect gradual increase in energy waste reduction

- PPAs will ramp up due to more solar

- Wind opportunity will have more front-end loading

- Steady growth at North Star

Load Growth

- Good load growth on a weather normalized basis in Michigan in 2022

- Expecting flat to slightly up overall in 2023

- Commercial up about 0.5 point and industrial between 1.5% to 2%

- Expecting limited activity at the plant beyond settlement of equity forward contracts for Covert acquisition in 2023

Financial Performance

- Adjusted net income of $838 million in 2022, translating to $2.89 per share at the high end of guidance range

- EPS growth driven primarily by utility and modest growth for NorthStar Clean Energy

- Plan for normal weather, negative year-over-year variance of $0.20 per share

- Anticipating $0.14 of EPS pickup attributable to rate relief

- Assuming $0.04 per share of positive variance attributable to continued productivity

- Assuming $0.19 to $0.25 of positive variance versus 2022 due to conservative estimates around weather-normalized sales and non-utility performance

- Targets solid investment grade credit ratings and manages key credit metrics accordingly

- Funding needs in 2023 limited to debt issuances at the utility

- De-risked financing needs for Covert acquisition