Eaton Corporation plc

CEO : Mr. Craig Arnold

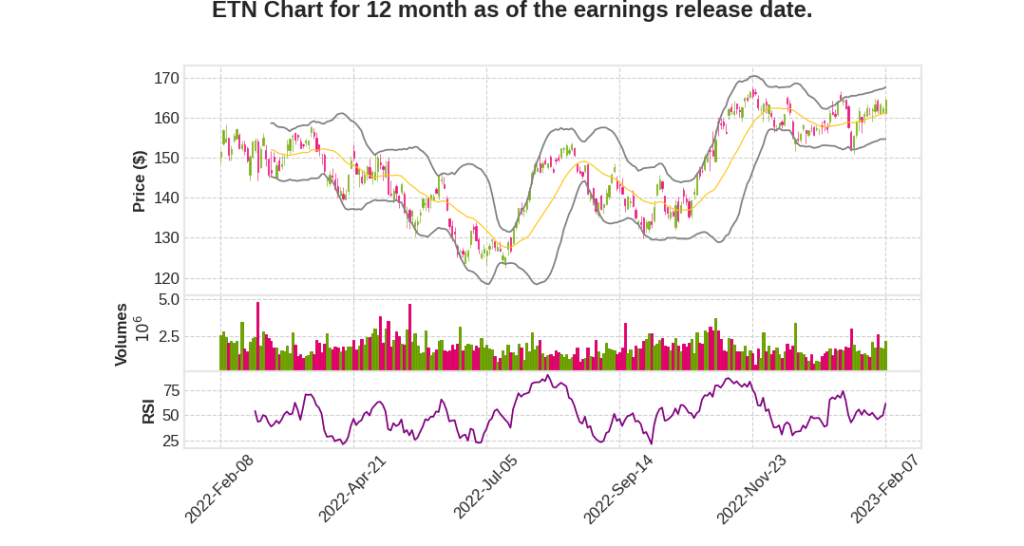

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 12.2% YoY | 32.8% | 31.2% | 2023-02-08 |

Tom Okray says,

Q4 2022 Financial Performance

- Revenue increased by 12% with 15% organic growth, partially offset by a 4% foreign exchange headwind and 1% net impact from acquisitions

- Operating profit grew 21% and adjusted EPS grew 20%

- All-time record adjusted earnings of $825 million and adjusted EPS of $2.06

- Electrical Americas set all-time records for sales, operating profit, and margin with organic sales growth of 20%

- Aerospace posted all-time record sales and operating profit with organic growth of 11%

Working Capital Efficiency

- Investments in working capital to support orders and backlog for Electrical and Aerospace businesses

- Net working capital to orders and inventory reduced significantly from 2019 to 2022

- Inventory as a percentage of backlog roughly cut in half from end of 2019 to end of 2022

2023 Guidance

- Organic growth guidance of 7% to 9%, with Electrical Americas and Aerospace at 8% to 10% and eMobility at 35%

- Segment margins guidance of 20.7% to 21.1%, a 70-basis point improvement at midpoint from 2022

- Adjusted EPS guidance of $8.04 to $8.44, a 9% growth over 2022

- Operating cash flow guidance of $3.2 billion to $3.6 billion, a 34% increase at midpoint over 2022

- Share repurchase guidance of $300 million to $600 million

Market Outlook

- End-market growth assumptions provided on Q3 earnings call and updated by Craig in the presentation

- Tremendous visibility and confidence in 2023 outlook due to increased backlog and strong organic growth

Craig Arnold says,

Quarterly Performance Highlights

- Generated adjusted EPS of $2.06 for the quarter and $7.57 for the year, both all-time records in each period

- Q4 adjusted EPS was up 20% from prior year

- Sales were $5.4 billion, up 15% organically

- Q4 margins of 20.8% were up 150 basis points from prior year, near the high end of our guidance range

- Record segment margins of 20.2%, up 130 basis points from prior year

- Orders continue to remain very strong, with Electrical orders up 25% and Aerospace orders increased 24%

- Generated record free cash flow in the quarter with adjusted free cash flow up 41%

Performance Highlights for Last Year

- Exceeded three of four key financial metrics

- Posted 13% growth for organic revenue, which was actually more than 60% above original guidance at the midpoint

- Record margins of 20.2% in 2022, 10 basis points above original guidance at the midpoint

- Adjusted EPS of $7.57 was $0.07 higher than the midpoint of original guidance

- Missed free cash flow guidance for the year due to higher levels of sales and orders, and the record backlogs

Market Dynamics and Growth Outlook

- Eaton is positioned at the center of major trends including the need to transition from fossil fuels to renewables, electrification of the economy, and digitalization

- Eaton predicts that the long-term growth goals of 5% to 8% annual growth will be exceeded due to market dynamics and government stimulus spending

- U.S. and EU programs will expand Eaton’s addressable market by some $11 billion to $14 billion over the next 5 years

Financial Performance and Shareholder Returns

- Eaton has delivered higher growth, higher margins and better earnings consistency over the past decade

- Eaton has significantly outperformed benchmarks in total shareholder returns for 3, 5 and 7 years

Q & A sessions,

Market Assumptions for 2023

- 85% of markets expected to see positive growth

- Commercial and institutional segment expected to have strong growth

- Residential market expected to be the only down market

- Data center market expected to remain strong with mid-teens growth over next 3 to 4 years

Company Performance

- 13% organic growth with record orders and backlog

- 2022 was a year of record profits, margins, adjusted earnings and EPS

- 20% increase in adjusted EPS growth in Q4 indicates positive indicator for 2023

- On track and likely ahead of schedule for delivering 2025 goals for revenue, margins, free cash flow, and adjusted EPS

Global Business Growth

- Mid-single-digit growth expected for Global business in face of typical recession

- China and Asia market could be stronger than anticipated

Inventory and Distributor Performance

- No inventory destocking to speak of

- Some inventory adjustment taking place with European distributors

- U.S. and Asia market still tight

Organic Growth Opportunities

- Plenty of organic growth opportunities to grow the enterprise

- Opportunistic approach to acquisitions

- Entered into joint ventures to shore up strategic position in China