Genuine Parts Company

CEO : Mr. Paul D. Donahue

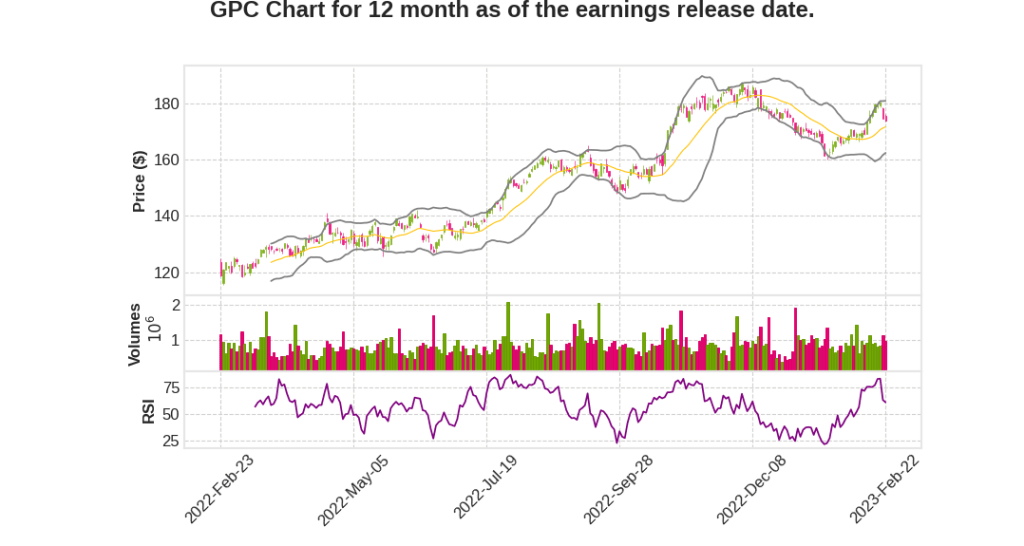

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 15.0% YoY | 2.8% | -0.6% | 2023-02-23 |

Will Stengel says,

Global Automotive Segment

- Total sales for the global automotive segment were $3.4 billion, an increase of approximately $243 million or 7.6% versus the same period in 2021

- For fiscal year 2022, Global Automotive segment sales was $13.7 billion, an increase of 8.9% from 2021

- Mid to high single digit levels of inflation were experienced during the fourth quarter

- U.S. Automotive business grew sales by approximately 11% with comparable sales growth of approximately 8%

- Canadian business grew sales approximately 15% in local currency, with comparable sales growth of approximately 13%

- European team delivered sales growth of 19% with comparable sales growth of approximately 8%

- Asian Pacific automotive business, sales in the fourth quarter increased approximately 10% in local currency from the same period in the prior year with comparable sales growth of approximately 7%

Global Industrial Segment

- Total sales at Motion were $2.1 billion, an increase of approximately $478 million or 29.6%

- Comparable sales growth, which excludes the benefit of KDG, increased approximately 17% in the fourth quarter versus last year

- Sales at Motion were $8.4 billion, an increase of $2.1 billion or 33.2%

- Global Industrial segment profit was approximately $887 million, and segment operating margin was a record 10.5%, an increase of 110 basis points from 2021 and up 240 basis points from 2019

- We completed several bolt-on acquisitions primarily consisting of small automotive store groups during the fourth quarter that increased local market density in existing geographies

Strategic Initiatives

- Investment and focus in strategic initiative pillars translate into a better customer experience, profitable growth, operational excellence and a differentiated team culture

- Category management strategic initiatives had an ongoing positive impact

- Improved insights are driving data-driven decisions around strategic pricing and sourcing, which have contributed to margin expansion performance

- Strategic initiatives around pricing, category management and supply chain are driving increased productivity and profitability, which is reflected in the strong margin expansion delivered in 2022

- Our acquisition pipeline is active, and we will remain disciplined to pursue transactions that advance our strategy, deliver profitable growth and create long-term value

Financial Performance

- Global Automotive segment operating margin was 8.6%, an increase of 30 basis points versus the same period in 2021

- Global Automotive segment profit was $1.2 billion and segment operating margin was 8.7%, an increase of 10 basis points from 2021 and up 110 basis points from 2019

- Industrial segment profit in the fourth quarter was $230 million or 11% of sales, representing a 150 basis point increase from the same period last year

Bert Nappier says,

Total Sales Growth

- Total GPC sales were up 15% or $720 million to $5.5 billion in Q4 2022, reflecting an 11.1% improvement in comparable sales, including mid-single-digit levels of inflation and an 8% contribution from acquisitions.

- Sales for the full year were $22.1 billion, up 17.1% from 2021, driven by our core business combined with acquisitions

- We expect total sales growth for 2023 to be in the range of 4% to 6%, with Automotive and Industrial segments expecting a 4% to 6% increase in comparable sales.

Gross Margin

- Gross margin expanded approximately 50 basis points in Q4 2022 to 35.7%, driven by ongoing investments in pricing and sourcing initiatives.

- The gains were partially offset by moderating year-over-year supplier incentives, a shift in the mix of sales based on the strength of the industrial business, foreign currency, and inflation.

- Gross margin for the full year was 35.1%, slightly above expectations and essentially in line with the prior year.

Adjusted Net Income and EPS

- Q4 2022 adjusted net income was $292 million or $2.05 per diluted share, up 15% from 2021.

- 2022 adjusted net income was $1.2 billion or $8.34 per diluted share, up 21% from 2021.

Capital Allocation

- The debt to adjusted EBITDA is 1.7 times, which highlights financial strength and flexibility.

- $340 million was invested in capital expenditures in 2022, and $3 billion was invested in KDG.

- $719 million was returned to shareholders in the form of dividends and share repurchases.

Outlook for 2023

- We expect diluted earnings per share to be in the range of $8.80 to $8.95, representing an increase of 6% to 7% from 2022 adjusted diluted earnings per share.

- Total sales growth for 2023 is expected to be in the range of 4% to 6%.

- Capital expenditures are expected to be in the range of $375 million to $400 million in 2023.

- The Board approved a $3.80 per share annual dividend for 2023, representing a 6% increase from 2022, and our 67th consecutive annual increase in the dividend.

Q & A sessions,

Overall Guidance

- Expecting 4% to 6% top line growth, driving EPS up 6% to 7%, in the range of $8.80 to $8.95

- Margin expansion expected from both segments

- Full-year guidance looks good with solid industry fundamentals for both businesses

- Expecting growth to moderate and normalize

Cadence of the Year

- Automotive growth expected to be consistent across quarters

- Industrial stronger in the first half with high single-digit outlook, more low single digit in the second half

Margin Expansion

- Expecting gross margins to be up in the range of 20 to 40 basis points for 2023

- Teams executing core strategies on pricing and sourcing capabilities

- SG&A deleverage of 30 to 40 basis points in total offset by other efficiencies

OpEx and CapEx

- Expecting a little bit of deleverage next year due to investments in tech and talent focused on the long term

- Freight expected to see inflationary pressure, but should abate in the second half of the year

- Mid-single-digit wage increase this year, absorbing costs on the health care side

- Investments in IT to improve capabilities and modernize platforms, driving leverage outside of those investments

- Expecting a slight increase in capital next year, focused on automation and modernization of DCs in the supply chain and IT platforms