HP Inc.

CEO : Mr. Enrique J. Lores

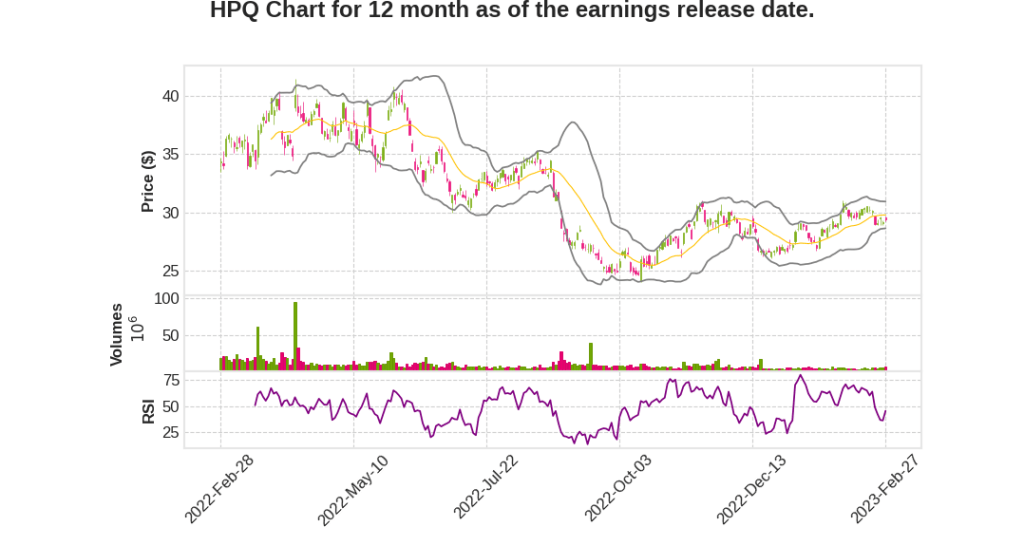

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q1 | -11.2% YoY | -38.0% | -100.1% | 2023-02-28 |

Marie Myers says,

Revenue and Margin

- Net revenue was $13.8 billion in Q1 2023, down 19% nominally and 15% in constant currency, driven by declines across each of our regions.

- Gross margin was 20.3% in the quarter, up 0.4 points year-on-year, primarily due to improved commodities and favorable print mix, partially offset by competitive pricing, including currency.

- Personal Systems revenue was $9.2 billion, down 24% or 20% in constant currency, with FX headwinds as expected.

Segment Performance

- Consumer revenue was down 36% and Commercial was down 18% in Personal Systems.

- Total Print revenue was $4.6 billion, down 5% nominally or 2% in constant currency.

Future Ready Efforts

- On track to deliver at least 40% of targeted $1.4 billion in gross annual run rate structural cost savings by the end of FY2023.

- Personal Systems targeting structural savings by streamlining the portfolio to better target customer needs.

- In Print, focus on execution and growing NPV positive units as well as the strength of the portfolio as HP navigates the supply chain environment.

Cash Flow and Capital Allocation

- Q1 cash flow from operations was nominally negative and free cash flow was an outflow of $0.2 billion, in line with expectations.

- We returned approximately $360 million to shareholders in Q1, including $100 million in share repurchases and $259 million in cash dividends.

- Expect free cash flow to be in the range of $3 billion to $3.5 billion for FY2023, with the second half of FY2023 stronger than the first.

Outlook

- For FY2023, HP expects a wide range of potential outcomes, which are reflected in their outlook ranges.

- Not expecting a significant economic recovery during FY2023.

- Personal Systems revenue is expected to remain under pressure near-term and decline sequentially by a high single-digit in Q2 2023.

Enrique Lores says,

Revenue and EPS

- Net revenue was $13.8 billion, down 19% nominally and 15% in constant currency.

- Non-GAAP EPS was $0.75, in line with previously provided outlook.

Future Ready Plan

- The plan has two primary objectives – to reduce the cost structure and develop operational capabilities to deliver long-term sustainable growth.

- Delivered on Q1 cost target and on track to deliver at least 40% of three-year savings by the end of fiscal year 2023.

Hybrid systems

- Key growth businesses grew double digits in Q1, including Hybrid systems.

- Hybrid systems business more than doubled YoY and Poly integration is going well.

- New hybrid work models are fueling demand for peripherals and other collaboration solutions.

Personal Systems

- Personal Systems revenue was $9.2 billion, down 24% or 20% in constant currency.

- Sellout to customers was higher than selling to the channel with a corresponding reduction in channel inventory.

- Commercial PC share increased by 2.8 points, and overall PC share grew by 2.5 points.

- Print revenue was $4.6 billion, down 4.5% or 2% in constant currency.

- Office hardware revenue grew 13% YoY or 5% sequentially and gained share in office quarter-over-quarter in calendar Q4.

- Instant Ink delivered double-digit revenue growth, surpassing 12 million subscribers.

Outlook

- Not expecting a significant economic recovery during fiscal year 2023.

- Expect the PC market in units may regress to pre-COVID levels in the short-term, but it will remain at a structurally higher level with more premium and high-value mix.

- Expect the overall print market to be down low-single digits this year driven by the challenging macro environment and slower-than-expected return to the office.

- Maintaining full-year financial outlook.

Q & A sessions,

Weakness in Consumer and Corporate Enterprise Space

- Continued weakness in the consumer space and recent weakening demand on the corporate enterprise space due to large companies becoming more conscious about how they use their budget, being slowly hiring people, and this has had an impact on the PC side.

Reduction of Inventory

- Reductions of inventory especially that one that addresses consumer and SMB business, the more transactional side of the business, which reflects that end-user demand has been stronger than shipments.

- Current view is that we will be getting to a normalized channel inventory situation by the end of Q2, early Q3, which means that in the second half, we will not have this headwind, and this is one of the reasons why we are optimistic about the evolution of the PC business during the year.

Changes in the Definition of the Growth Categories

- During this quarter, HP has made some changes in the definition of the growth categories because they wanted to align better how they talk about them externally to some of the internal changes they have made.

- By growth categories, HP is referring to the six businesses that they think are going to be growing faster than the core business and that they’re going to have accretive margins compared to core.

Cash Flow Outlook

- Expected cash flow to lineup with the seasonality comments that Enrique made earlier. So they expect it to be better and materially stronger in the second half of the year.

- Expect cash flow in Q2 to be roughly in line with Q1.

Sources of Cash

- PS revenue will grow on the topline in the second half of the year and contributes cash when it grows sequentially because of its negative cash conversion cycle.

- Continued inventory reductions.