Invitation Homes Inc.

CEO : Mr. Dallas B. Tanner

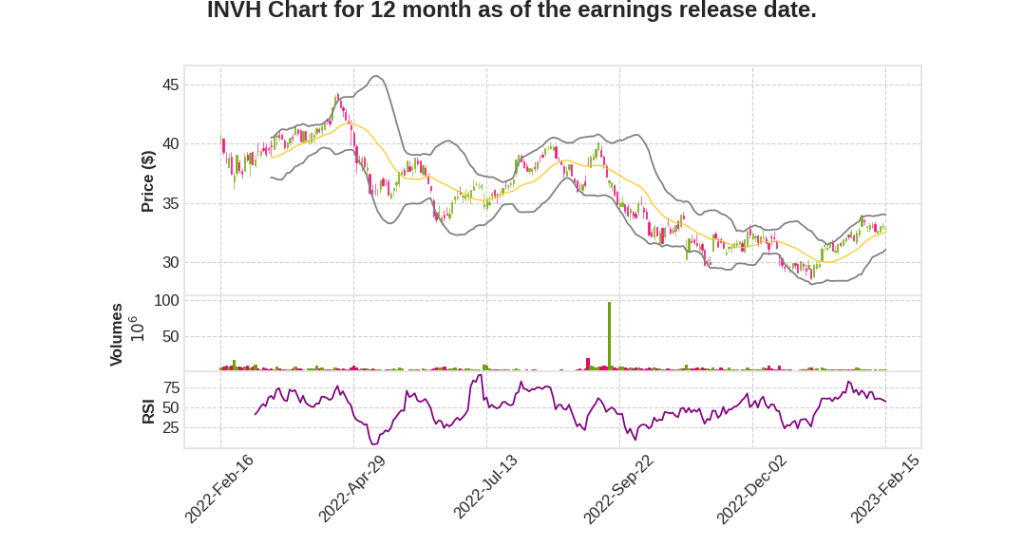

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 11.5% YoY | 16.5% | 33.3% | 2023-02-16 |

Dallas Tanner says,

2022 Performance and Expectations for 2023

- Core FFO growth of 11.6% and same-store NOI growth of 9.1% in 2022

- Ernie will be stepping down as CFO in a few months, and Jon Olsen will be taking over in June

- The U.S. needs to add more than 13 million housing units over the next seven years to address the undersupply of the past decade

- It remains challenging to deliver new supply in desirable locations, because of state and local restriction, as well as labor and material shortages

- Strong demand for single-family housing is expected to continue due to the millennial generation aging and the increased flexibility to work from home

- The lack of available supply of single-family housing and strong demand have made homeownership much more expensive today

- Leasing a home costs nearly $900 less each month than owning a home across their markets, and leasing home can save a family nearly 30% a month on their housing costs on average

- The Invitation Homes value proposition is compelling for both residents and shareholders

Differentiators of Invitation Homes

- Recently renovated, refreshed, or newly built homes in desirable locations

- ProCare, which is a resident service model that provides consistent interactions with residents throughout their time with Invitation Homes

- Best-in-class technology tools, including a mobile maintenance app, offering residents an efficient process to submit service requests

- A growing list of resident services designed to elevate their living experience

- Single-family homes are the most liquid real estate sector within the United States

- There’s typically much lower turnover in single-family rental than in multifamily with residents often staying much longer

- There’s a long track record of rent growth within SFR even during recessionary periods

- Strong balance sheet with no debt coming due until 2026

- Builder partner growth pipeline that maximizes flexibility and contributes to new housing supply while also avoiding big investments in land and a large G&A load

Ernie Freedman says,

Balance Sheet and Capital Markets Activity

- Net debt to adjusted EBITDA is at 5.7 times, and over 99% of the debt is fixed rate or swapped to fixed rate

- Weighted average maturity is at 5.6 years, and there is no debt coming due until 2026

- We achieved the investment-grade rating in the spring of 2021

Financial Results for Q4

- Core FFO increased by 10.6% YoY to $0.43 per share, and AFFO increased by 9.2% to $0.36 per share

2023 Guidance

- Same-store core revenue growth is expected to be in a range of 5.25% to 6.25%

- Same-store core expense growth is expected to be in a range of 7.5% to 9.5%, including an increase in real estate taxes

- Same-store NOI growth is expected to be in a range of 4.0% to 5.5%

- Core FFO per share is expected to be in the range of $1.73 to $1.81 and AFFO per share in the range of $1.43 to $1.51

- Acquisitions are expected to be modest, including the initial expectation for on-balance sheet acquisitions of $250 million to $300 million from their builder partners and acquisitions in their joint ventures of $100 million to $300 million

- Quarterly dividend increased by 18.2% to $0.26 per share

Q & A sessions,

Capital Investment and Supply

- Plenty of appetite with JV partners to continue to invest capital.

- Supply is relatively tight; resale supply inventory is the lowest in the last three to four years.

- Newer build stuff seems to have better return profile, but there is more angst on the builder side given the uncertain environment.

- Plenty of capital interested in investing, not a tremendous amount of opportunity real-time, but it is expected to moderate throughout the year.

- The pipeline today sits at about 2,300 homes in contract with different builder partners.

Joint Venture and Growth

- Joint venture capital will always be something that they look at on a relative basis to where their current cost of capital is from a balance sheet perspective.

- Third-party avenues, or longer-term partners, will be used to deploy capital, which will generate outsized returns.

- The approach in 2023 would be to look opportunistically to enhance and grow the pipeline and find ways to do things more programmatically with preferred partners.

- The company will explore and use venues like joint ventures, never at a way that it would impact their ability to grow the balance sheet.

- The company’s goal is to find the right balance between investing on the balance sheet and using third-party avenues.

Demand and Market

- There is a pickup in new lease growth across the 99 SFR markets, which grew about 6.5% in 2022.

- The company is bullish on the prospects of both the quality of the resident and the amount of demand for the product.

- The company is not seeing any degradation in top of funnel from the multifamily proposition outweighing the decision to go for SFR.

- Builders are being more cautious, and there are local regulatory restrictions.

Growth and Acquisition

- The company is going to find ways to build new product and bring more product into the marketplace and create strategic ventures with partners on the homebuilding side.

- There is a commitment to continue being opportunistic and buy in a one-off nature.

- There are going to be opportunities for additional M&A with small to mid-sized portfolios as operators consider their options around recapping or not, with interest rate costs being where they are.

- The company expects opportunities for consolidation in the sector in the coming years.

Guidance and Turn

- At the midpoint of guidance, the company expects a little bit of a year-over-year decline.

- The decline has to do mostly with the fact that they expect turn.