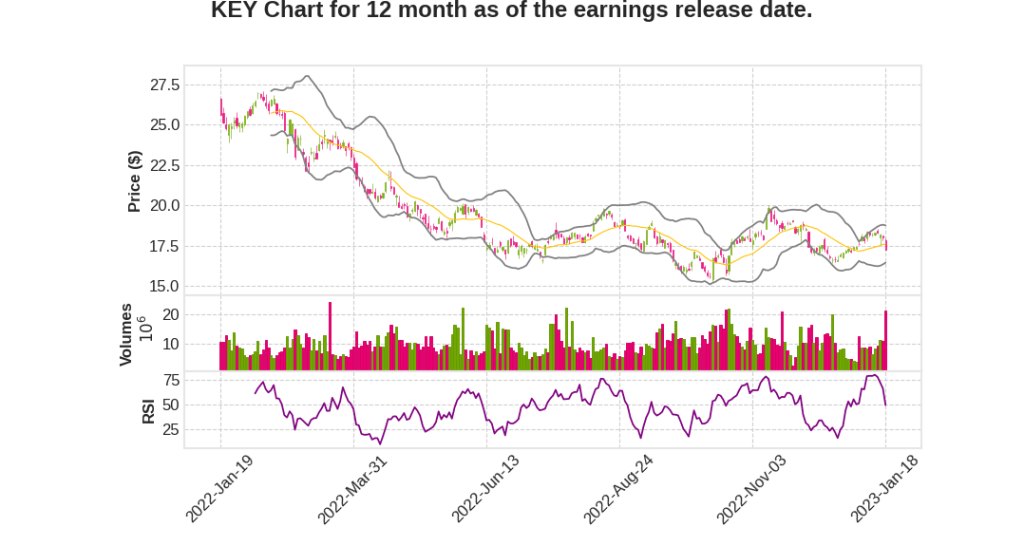

KeyCorp

CEO : Mr. Christopher Marrott Gorman

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -2.3% YoY | -100.0% | -41.5% | 2023-01-19 |

Don Kimble says,

Net income and loan growth

- Net income from continuing operations for Q4 2022 was $0.38 per common share, down $0.17 from the prior quarter and down $0.26 from last year.

- Average loans for the quarter were $117.7 billion, up 18% from the year ago period, and up 3% from the prior quarter.

- Commercial loans increased 17% from the year ago quarter, driven by growth in commercial and industrial loans and commercial real estate balances.

- Consumer loans increased 22% reflecting growth in consumer mortgage and Laurel Road.

Deposits and interest rates

- Average deposits totaled $145.7 billion for the Q4 2022, down 4% from the year ago period, and up $1.4 billion or 1% compared to the prior quarter.

- Interest-bearing deposit costs increased 49 basis points from the prior quarter, and cumulative deposit beta was 19% since the Fed began raising interest rates in March 2022.

- Approximately 60% of Key’s balances were in core consumer and escrow deposits, and over 80% of commercial deposits were from core operating accounts.

Net interest income and noninterest income

- Taxable equivalent net interest income was $1.2 billion for Q4 2022, compared to $1.0 billion in the year ago period and $1.2 billion in the prior quarter.

- Noninterest income was $671 million for Q4 2022, compared to $909 million for the year ago period and $683 million in the third quarter.

- The decline in noninterest income from Q4 2022 reflects a $151 million decline in investment banking and debt placement fees, along with a $35 million reduction in other income, primarily from market-related gains in the year ago period.

Expenses and credit quality

- Total noninterest expense for Q4 2022 was $1.16 billion, down $14 million in the year ago period and up $50 million from last quarter.

- Net charge-offs were $41 million or 14 basis points on average loans for Q4 2022, which remain near historical low levels.

- Our provision for credit losses was $265 million for Q4 2022, which exceeded net charge-offs by $224 million.

2023 Outlook and long-term targets

- Average loans are expected to be up between 6% and 9%, and average deposits will be flat to down 2%.

- Net interest income is expected to be up between 6% and 9%, reflecting growth in average loan balances and higher interest rates.

- We expect noninterest expense to be relatively stable with the benefit of the cost takeout opportunities.

- Net charge-offs will be in the 25 to 30 basis-point range, well below the through-the-cycle range of 40 to 60 basis points.

- Long-term targets remain unchanged: Key expects to continue to make progress on these targets by maintaining the moderate risk profile and improving our productivity and efficiency, which will drive returns.

Chris Gorman says,

Key Points from KeyCorp’s Q4 2022 Earnings Call

- KeyCorp reported earnings of $356 million or $0.38 per common share, which included $265 million of provision for credit losses.

- Consumer business has continued to grow with younger clients being the fastest-growing segment.

- Commercial business has also expanded with over 80% of deposits from core operating accounts.

- Net interest income increased by 2% from Q3 due to relationship-based loan growth and stable deposits.

- Credit quality remained strong with net charge-offs as a percentage of average loans of 14 basis points.

- KeyCorp plans to continue executing on their differentiated business model and strategy, expanding their presence in fastest-growing markets and targeted industry verticals.

- The company will benefit from their balance sheet and interest rate positioning with significant upside over the next two years.

- KeyCorp will maintain their strong credit quality by reducing expenses and accelerating cost takeout plans in 2023, targeting a 4% reduction relative to full year 2022 level.

Q & A sessions,

Continued Investment

- The company will continue to invest in critical areas of the business, focusing on growth markets and younger customers.

- The company plans to increase its banker population by 25% by 2025.

- The company is committed to growing its members from 50,000 to 250,000 through investments in areas such as public service loan forgiveness and income-based repayment gain.

Credit Metrics and Reserve Build

- The company built a reserve due to the macro view of the economy slowing and the probability of a mild recession increasing.

- CECL models, which are forward-looking, indicate a significant impact on the company’s mortgage book due to declining home prices.

- The company is monitoring potential risks associated with leverage finance and real estate in B and C class office spaces and retail.

Results and Outlook

- The company reported earnings of $356 million or $0.38 per common share, with continued growth in both consumer and commercial businesses.

- Net interest income was up 2% from the previous quarter, reflecting continued relationship-based loan growth.

- The company originated over $1.5 billion of Laurel Road loans last year and increased household members by over 30%.

- The company raised a record $136 billion of capital for its clients in 2022, and credit quality remained strong.

Fee-Based Businesses

- Investment banking and debt placement fees were up from the previous quarter but down from the year-ago period, reflecting broader capital markets trends.

- The pull-through rates were adversely impacted by market uncertainty.

- The company has solid pipelines, particularly in M&A, but more activity is moving onto its balance sheet.

Priorities for 2023 and Beyond

- The company will continue to execute on its digital affinity bank and offerings for doctors and nurses.

- The company will maintain its moderate risk profile while supporting its clients and returning capital to shareholders.

- The company plans to focus on expanding relationships and offering the best execution with both on- and off-balance sheet solutions.