Kimberly-Clark Corporation

CEO : Mr. Michael D. Hsu

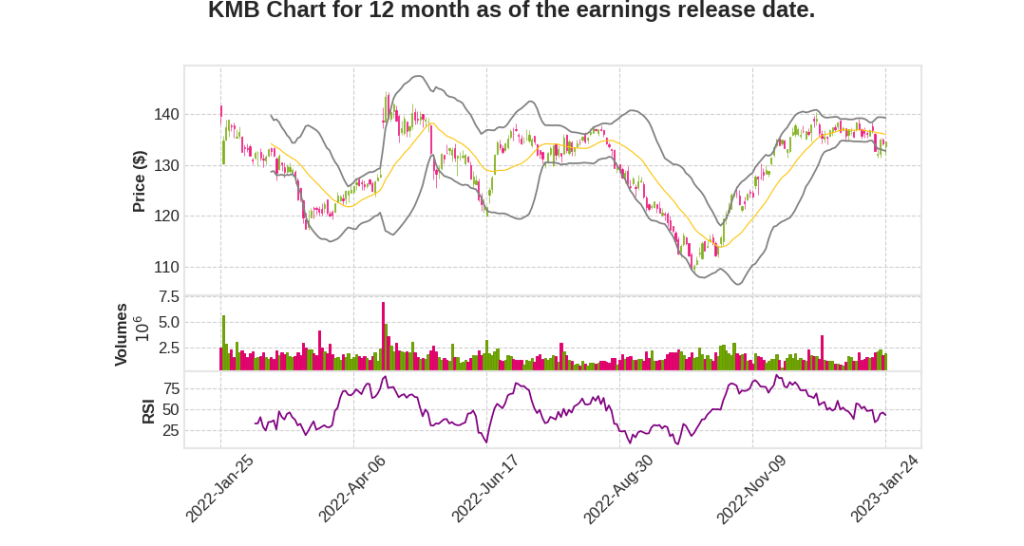

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -0.0% YoY | 36.7% | 44.2% | 2023-01-25 |

Mike Hsu says,

Organic Sales Growth

- K-C has grown business by about $1.5 billion in sales and delivered 4% average organic sales growth since 2019.

- In 2022, organic sales increased by 7% and exceeded the company’s goals at the beginning of the year.

Margin Recovery

- K-C has faced unprecedented inflation worth over $3 billion, a roughly 1,500 basis point headwind to gross margin in the past two years.

- The company has mitigated this impact by implementing broad pricing actions and generating over $700 million in cost savings.

- Gross margin stabilized in Q3 and increased year-over-year in Q4 by over 200 basis points.

- At the midpoint of the 2023 guidance range, K-C plans to improve operating margin by approximately 80 basis points, translating to 2% to 6% growth in earnings per share.

Investment in Balanced and Sustainable Growth

- K-C is scaling innovation that delivers better value, more benefits, and better care for consumers.

- The company plans to launch several initiatives in 2023, including GoodNites youth pant and performance upgrades for Huggies diapers.

- K-C intends to leverage its broad range of offerings to address the growing need for value through compelling commercial programs.

Product Obsession and World-Class Commercial Execution

- K-C introduces new products that contributed to over 60% of the company’s organic growth in 2022.

- K-C’s product obsession, advantage technology, and consumer-centric focus are enabling the company to create meaningful value and accelerate category growth.

China Market Growth

- K-C continues to post double-digit organic growth in China, despite a declining birth rate and challenging COVID operating conditions.

- K-C’s superior technology for baby and child care products supports the company’s strong portfolio and anchors its leadership in the world’s largest baby and child care market.

Nelson Urdaneta says,

Impact of Fiber Market Prices on KMB Stock

- Fiber market prices have plateaued in Q3 and have slightly turned in Q4, affecting KMB’s earnings.

- Eucalyptus, fluff, NBSK, and other components of the fiber complex are projected to be down 10% for the full year.

- Prices are expected to ease throughout 2023.

- The pulp complex is expected to be up for KMB in 2023.

- Pulp complex is half of the commodity inflation of $200 million to $300 million quoted in KMB’s guidance.

Q & A sessions,

Expected Performance in 2023

- The company plans to deliver a better performance in 2023 and build on organic growth momentum.

- The company has a robust innovation and commercial program for 2023, and consumer demand in their categories generally remains very resilient.

Pricing Actions and Investment

- New pricing actions have been announced to customers, with more planned for next year.

- The company is increasing advertising spending and investing behind robust commercial programs.

Margin Recovery and Costs

- The company expects continued progress on margin recovery and aims for the top end of the range internally.

- Reversion is expected to happen at some point, which will accelerate margin recovery.

- Selected commodities are starting to ease, and there are green shoots in costs.

D&E and Resilient Consumer Demand

- D&E performance has softened due to business approach challenges in Southeast Asia and increased competition in Vietnam and India.

- The company is still seeing a resilient consumer, and observed elasticity impacts on volume are far below what is modeled.

Overall Performance and Brand Performance

- The company feels good about overall performance and continues to see organic momentum.

- The brands are performing well, with adult care up 12% and feminine care up almost double digits.