The Coca-Cola Company

CEO : Mr. James Robert B. Quincey

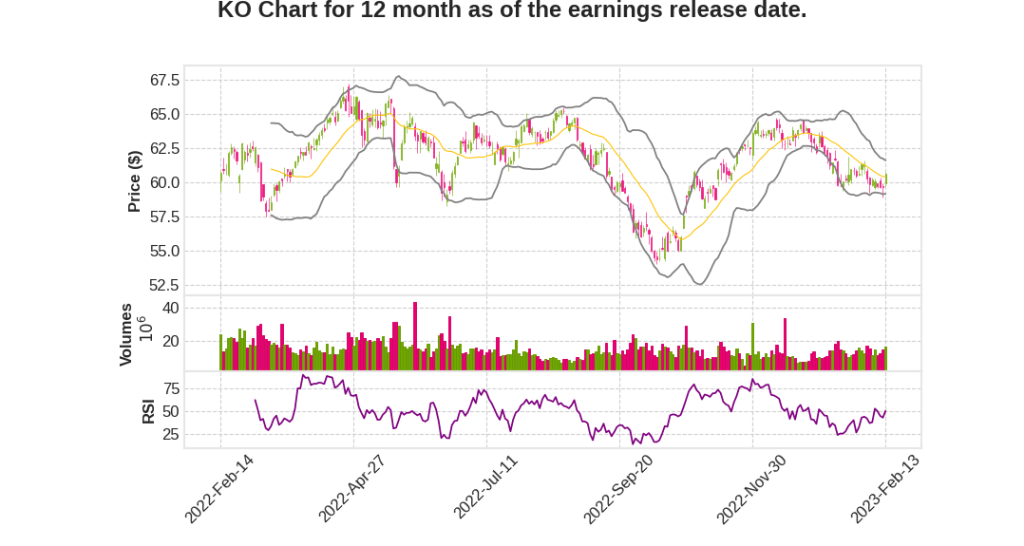

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 7.0% YoY | 29.4% | -16.1% | 2023-02-14 |

James Quincey says,

Q4 2022 Performance

- Delivered 15% organic revenue growth in Q4 with strong growth across operating segments.

- Robust volume growth across many markets, but more than offset by suspension of business in Russia and impact on consumption due to varying levels of pandemic restrictions and surge in COVID cases in China.

- Maintained consistent volume growth relative to 2019 and gained both volume and value share for the consolidated business for both the quarter and the year.

2023 Outlook

- Uncertainties remain in the macro economy due to economic policies, consumer demand, inflation, supply chain, war, and geopolitics.

- Focused on delivering key objectives including pursuing excellence globally and winning locally, investing for the long-term health of the business, and generating US dollar EPS growth to deliver value for shareholders.

- Executing more efficiently and effectively on a local level while maintaining flexibility on a global level.

Marketing Strategies

- Linking occasions and passion points to drive engagement and create immersive experiences for consumers.

- Harnessing enhanced capabilities to win locally and tying beverages to consumption occasions.

- Leveraging passion points locally through partnerships and driving consumer interest and action through digital experiences.

- Delivering new and unexpected innovation by leveraging Gen Z insights.

Sustainability

- Driving growth of low- and no-calorie beverages, providing smaller package choices, and setting new industry-leading goals for refillable or reusable packaging and cooler energy efficiency.

- Investing in nature-based water solutions and linking diversity equity inclusion performance measures to executive annual incentive program.

- Using leadership and scale to drive change while delivering results and building resilience.

John Murphy says,

Revenue and Earnings

- Organic revenue growth of 15% in Q4 2022.

- Price/mix growth of 12%, driven by pricing actions, revenue growth management initiatives, and favorable channel and package mix.

- Comparable EPS of $0.45 was in line with last year despite higher-than-expected currency headwinds.

- Guidance for 2023 predicts organic revenue growth of 7% to 8% and comparable earnings per share growth of 7% to 9% versus 2022.

- Expects per-case commodity price inflation in the range of a mid-single-digit impact on comparable cost of goods sold in 2023.

- Expects comparable EPS growth of 4% to 5% versus $2.48 in 2022.

Marketing Investments

- Continued to significantly accelerate marketing investments to engage and retain existing consumers and new consumers.

- Higher costs across the P&L, increased marketing, and currency headwinds resulted in a comparable operating margin expansion of 65 basis points for the quarter.

Cash Flow

- Delivered free cash flow of $9.5 billion, a decline of 15% versus the prior year.

- Underlying cash flow generation remains strong, and the three-year average free cash flow conversion ratio is above 100%, ahead of their long-term target.

- Expects to generate approximately $9.5 billion of free cash flow in 2023 through approximately $11.4 billion in cash from operations less approximately $1.9 billion in capital investments.

Balance Sheet and Tax Dispute

- Net debt leverage of 1.8 times EBITDA as of the end of 2022, which is below their targeted range of 2 to 2.5 times.

- The ongoing US income tax dispute with the IRS will not have a bearing on their ability to deliver on their capital allocation agenda and drive long-term business growth.

- Expects an approximate two to three-point currency headwind to comparable net revenues and an approximate three to four-point currency headwind to comparable earnings per share for full year 2023.

Operating Environment

- Expects the operating environment to remain dynamic in 2023.

- Expect price mix to moderate through the year as they cycle their pricing initiatives from the prior year.

- Expect to see elevated inflation across their operating costs.

- Expects to see higher net interest expense given their effective exposure to floating rate debt.

- Due to their reporting calendar, there will be one less day in the first quarter and one additional day in the fourth quarter.

Q & A sessions,

can have a good discussion with the customers. When it comes to specific regions, there are different dynamics at play. In Europe, there has been a spike in inflation due to conflict, leading to softening consumer demand. In the US, the situation is moderating without causing a hard landing with good momentum in the business. Latin America is doing well, but some places continue to have very high inflation and economic problems. In Asia, the reopening of China is expected to be positive for the business, India is doing well, and ASEAN is expected to come back up. In terms of pricing, the focus is on earning the right to pay price and delivering value to consumers through marketing, innovation, RGM, pricing, and packaging work, and execution. The goal is to sustain pricing and work with customers to ensure it works for them and ultimately for consumers.