Eli Lilly and Company

CEO : Mr. David A. Ricks

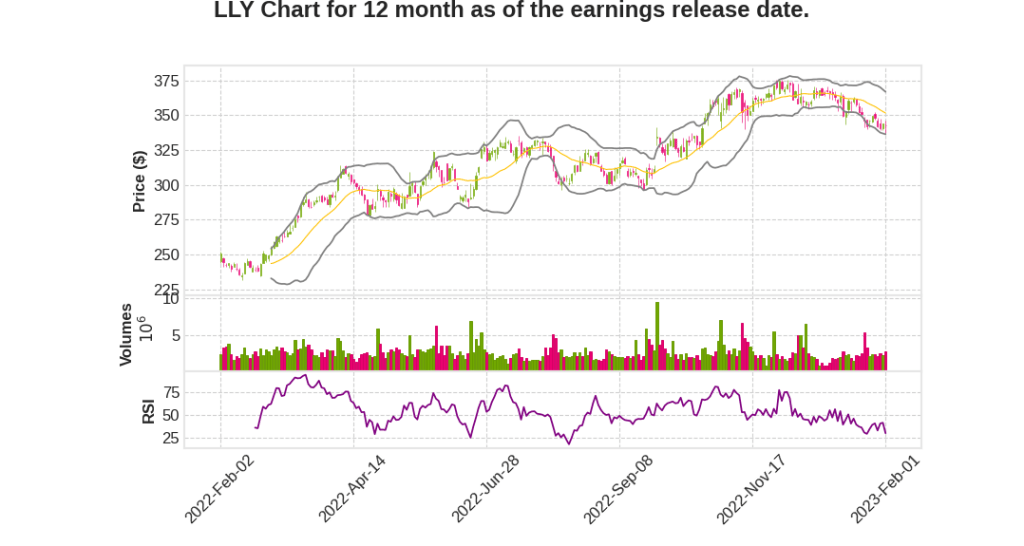

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -8.7% YoY | 10.3% | 12.7% | 2023-02-02 |

Anat Ashkenazi says,

Financial Performance

- 10% growth for core business in Q4 on a constant currency basis, driven by strong volume growth.

- COVID-19 antibody revenue declined 96% YoY from approximately $1.1 billion in Q4 2021 to $38 million in Q4 2022.

- Revenue excluding COVID-19 antibodies grew 2% or 5% on a constant currency basis in FY 2022.

- Non-GAAP gross margin was 80.5% in Q4, an increase of approximately 440 basis points.

- Marketing, selling, and administrative expenses increased 3% in Q4.

- R&D expense for the quarter increased 5%, driven by higher development expenses for late-stage assets.

- Operating income declined 7% compared to Q4 2021, driven by lower revenue, partially offset by lower operating expenses.

Geographical Revenue Growth

- US revenue declined 10% in Q4. Excluding COVID-19 antibodies, revenue grew 11% in the US.

- Revenue in Europe increased 8% in constant currency driven primarily by volume growth.

- Revenue in Japan decreased 6% in constant currency, revenue growth in Japan continues to be negatively impacted by decreased demand for several products that have lost patent exclusivity.

- Revenue in China grew 2% in constant currency.

- Revenue in the Rest of the World increased 11% in constant currency this quarter.

Key Growth Products

- Key growth products grew 21% and accounted for 70% of our revenue this quarter.

- Verzenio sales in the quarter grew 100%, driven mainly by the edge of an indication.

- Jardiance sales grew 42% and the product retains the leadership position, in a competitive market globally.

- Mounjaro’s strong launch uptake continues, underpinned by differentiated efficacy profile.

- As we expand payer access, the proportion of paid scripts for Mounjaro should continue to increase.

Effective Tax Rate and Financial Guidance

- Effective tax rate for 2022 was 10.3%, and for 2023, it is updated from 16% to approximately 13%.

- EPS range on a GAAP basis for 2023 is $7.90 to $8.10, and on a non-GAAP basis, it is $8.35 to $8.55.

- The midpoint of the 2023 revenue guidance range represents roughly 7% of growth or 50% growth for our core business excluding COVID-19 antibodies.

Pipeline Update

- This year holds tremendous promise for us to help patients as we execute on the current wave of potential launches while maintaining our commitment to invest in and progress future innovation.

- We expect this ongoing focus on disciplined execution and investment will help drive top-tier revenue growth through 2030.

Dan Skovronsky says,

Key Pipeline Assets and Approvals

- Lilly advanced late-stage assets including tirzepatide, donanemab, pirtobrutinib, mirikizumab, and lebrikizumab to key regulatory submissions.

- Mounjaro for type 2 diabetes was launched in mid-2022 and received approval for pirtobrutinib, now known as Jaypirca.

- Potential to launch two new immunology assets with mirikizumab and lebrikizumab by the end of 2022.

- Phase III readout for ganitumab expected mid-year.

- NEXT wave of assets that have entered or will soon enter Phase III registrational trials include SERD in breast cancer, weekly insulin for diabetes, remternetug in Alzheimer’s disease, Orforglipron, and Retatrutide in diabetes and obesity.

Diabetes and Cardiometabolic Disease

- The EMPA-KIDNEY Phase III trial showed a significant benefit of Jardiance, in reducing the relative risk of kidney disease progression or cardiovascular death by 28% compared with placebo in people with chronic kidney disease.

- QWINT-1, a Phase III study comparing fixed dose escalation of Lilly’s weekly insulin to Insulin Glargine, in insulin-naive type 2 diabetes patients has been initiated.

- Advanced two assets into Phase II, that aim to lower Lp(a), a well-known risk factor for atherosclerotic cardiovascular disease.

Oncology

- Jaypirca is the second product approved from Lilly’s 2019 Loxo Oncology acquisition.

- FGFR3 program recently dosed its first patient.

- Dosed the first patient in EMBER-4, our second Phase III trial for imlunestrant, our oral SERD.

- sNDA has been submitted to the US FDA to potentially expand our adjuvant indication beyond the currently indicated Cohort 1 KI-67 greater than 20% population.

Immunology

- Potential FDA approvals later this year for mirikizumab in ulcerative colitis and lebrikizumab in atopic dermatitis.

- Exciting proof-of-concept results for our PD-1 agonist antibody peresolimab in rheumatoid arthritis at the ACR conference in November and we have now initiated a global dose-ranging Phase IIb study.

Neuroscience

- Phase III TRABLASER-ALZ-2 study in Q2 of this year for donanemab as a new treatment for people with early symptomatic Alzheimer’s disease.

- Lilly has advanced into Phase II P2X7 inhibitor for chronic pain.

Q & A sessions,

Obesity Market Potential

- Obesity is a huge problem in the US and around the world, with 100 million Americans and one billion people worldwide potentially affected

- Injectables alone may not be able to address the entire market, and orals are necessary to match the safety, tolerability, and efficacy of injectables

- Single mechanism, single incretin agonists are not as effective as dual agonism for tirzepatide or triple agonism with GGG, and the company is working on oral solutions that bring additional incretin activity to patients in a pill

FDA CRL and ARIA

- The FDA issued a CRL for the company’s product, which focused on the 12-month exposure and did not discuss issues like ARIA

- Rates of asymptomatic radiographic-only ARIA are difficult to compare across drugs, and the focus should be on rates of symptomatic ARIA and serious adverse events resulting from ARIA

- In TRAILBLAZER-1, the numbers were similar to other members of the class, while in TRAILBLAZER-4, the numbers looked very good. The level of concern over ARIA is not high.

Clinical Trials and Endpoints

- The company feels more confident than ever before that ADAS is the right way to go as a primary outcome endpoint, with more homogeneity in effect compared to CDR Sum of Boxes

- If the company were to hit one outcome and not the other, it wants to understand why that happened and investigate other secondaries

Manufacturing Capacity Expansion

- The company is making substantial investments in manufacturing sites, with $3.3 billion of investment just this year, and substantial expansion of capacity across the globe to support not just Mounjaro but the rest of the portfolio

- Several products are part of the same manufacturing network, and the same auto-injector platform, which helps build capacity across the Lilly portfolio