Lincoln National Corporation

CEO : Ms. Ellen Gail Cooper C.F.A., F.S.A.

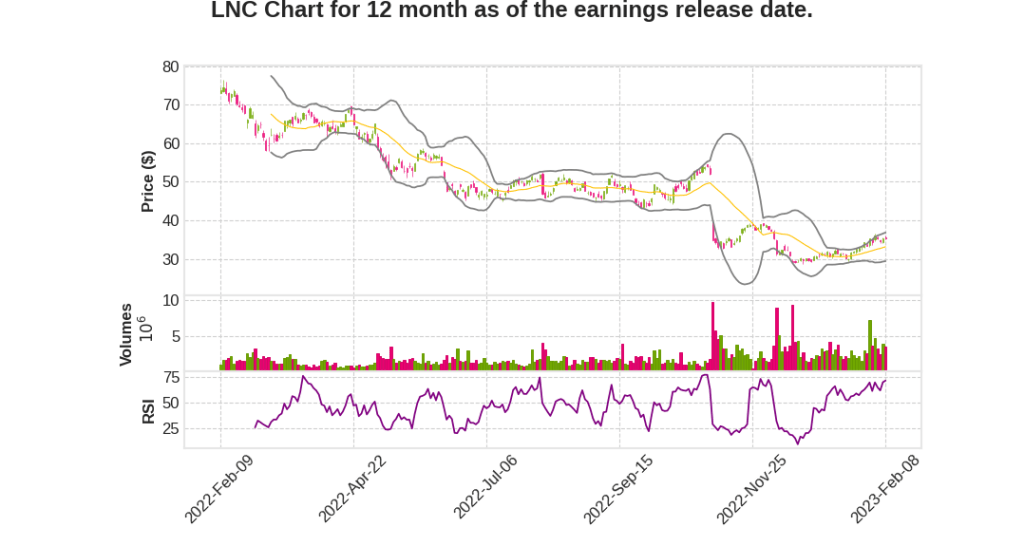

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -8.1% YoY | -100.0% | 3251.4% | 2023-02-09 |

Randal Freitag says,

Capital Position and Earnings Results

- Lincoln reported a statutory capital of $9.6 billion at year-end and an RBC ratio of approximately 383% for Q4 2022.

- The company’s cash at the holding company increased to $960 million, up $200 million sequentially.

- Lincoln reported Q4 2022 adjusted operating income of $170 million or $0.97 per share.

- Q4 2022 net income for the company was $6 million or $0.01 per share.

Life Insurance Segment Results

- Lincoln reported a Q4 2022 operating income of $46 million for its Life Insurance business, down from $80 million in the prior-year quarter.

- The drop was primarily driven by alternative investment results and the quarterly run rate impact of the third-quarter unlocking, partially offset by improved pandemic claims.

- Base spreads were 122 basis points for the quarter, down from 135 basis points in the prior-year quarter.

Annuities Segment Results

- Lincoln reported a Q4 2022 operating income of $238 million for its Annuities business, compared to $332 million in the prior-year quarter.

- Lincoln’s VAs with living benefit guarantees represent 45% of total account values, a decrease of five percentage points from the prior-year.

- Lincoln expects its diverse product portfolio, revised VA hedge program, and the benefit of higher interest rates to help drive future earnings and cash flow generation.

Group Protection Segment Results

- Lincoln reported a Q4 2022 operating income of $47 million for its Group Protection business, an increase from an operating loss of $115 million in the prior-year quarter.

- Group’s underlying margin was within our target range of 5% to 7% for the quarter and the full-year at 5.2% and 5.3%, respectively, when adjusting for the pandemic and unfavorable alternative investment income.

Retirement Plan Services Segment Results

- Lincoln reported a Q4 2022 operating income of $49 million for its Retirement Plan Services business, compared to $57 million in the prior-year quarter.

- Base spreads, excluding variable investment income, expanded over the prior-year quarter by 30 basis points. For the full-year, base spreads expanded 10 basis points.

- Lincoln expects reported spreads to be in line with 2022 results as lower variable investment income is offset by base spread expansion.

LDTI Impact

- Lincoln expects LDTI to have a minimal impact on overall operating earnings.

- Adjusted operating EPS will include an estimated $800 million of VA hedge costs.

- Lincoln estimates the impact of LDTI will increase year-end total book value by about $300 million and reduce year-end book value, excluding AOCI, by $900 million.

Ellen Cooper says,

Appointment of New CFO

- Current Chief Strategy Officer, Chris Neczypor, will become the new CFO effective February 17th.

- Chris has over 20 years of experience in the industry and a deep understanding of insurance financials.

- With Chris’ leadership, Lincoln will continue to focus on balance sheet resilience and overall drivers of the stock’s valuation.

Strategic Objectives

- Maximizing distributable earnings and improving capital generation.

- Reducing capital sensitivity to market volatility.

- Further diversifying the earnings mix.

Progress on Rebuilding Capital and Improving Efficiency

- Raised $1 billion of capital through a preferred issuance and expected to end the year with an RBC ratio of approximately 383%, an improvement towards the target of 400%.

- Focused on delivering a more capital-efficient product mix, which will require approximately $300 million less in new business capital this year.

- Fully repositioned the variable annuity hedge program to align with objectives of maximizing distributable earnings and providing explicit capital protection.

- Continued implementation of Spark, an enterprise-wide expense initiative expected to contribute run-rate savings of $260 million to $300 million by late 2024.

- Ended full-year 2022 with an underlying margin of 5.3% within the target range of 5% to 7% for group business margin expansion.

Business Unit Highlights

- Fourth quarter life sales were up sequentially in all products except terms where pricing actions were taken, and sales were up for the full year.

- Annuity sales increased 7% from the prior year quarter with positive flows reflecting continued strength in index variables and fixed index products.

- Group Protection had a year of solid top-line and overall earnings results, with premiums growing 7% for the full year.

- Despite a 7% decline in fourth quarter total deposits from a strong prior year period, full-year total deposits in Retirement rose 10%.

Q & A sessions,

Opportunities for Value Maximization

- Company is evaluating both internal and external potential solutions to maximize the value of their in-force.

- A fully dedicated team is actively evaluating external opportunities that could improve the ongoing capital position and rebuild of capital.

- An opportunity that supports enterprise strategic objectives and is good for shareholders at an appropriate price would be pursued.

Guidance for 2023

- The company has guided to a distributable earnings range of $600 million to $800 million.

- A range of $300 million to $500 million in overall free cash flow for 2023 is expected, assuming normal capital market environment.

- The company is expecting to see an improving contribution to distributable earnings of the sales mix that will continue to grow over time.

Capital Management and Allocation

- The company remains committed to returning capital to shareholders by way of dividend.

- The investment portfolio of the company is of the highest quality, and the credit deterioration is manageable in the overall realm of the portfolio in case of a hit on the credit cycle.

- The company is focused on maximizing profitable growth in a capital-efficient manner and investing in the future of the franchise.

Business Segments

- The company expects to strengthen the Life company to a target of 400% with a longer-term target.

- Linbar is in line with the company’s long-term expectations and is in a better position when thinking about future sources of capital.

- The company expects to take down $500 million of leverage with the prefunded $500 million maturity.

Headwinds in 2023

- Reinsurance costs will be higher year-over-year in 2023 due to additional settlements.

- Spread in the Life business is expected to settle down about 10 basis points before expanding in 2024 and beyond.

- Treasury lock-in programs and pre-investing resulting in short-term pain in 2023 before expanding in 2024 and beyond.