Lamb Weston Holdings, Inc.

CEO : Mr. Thomas P. Werner

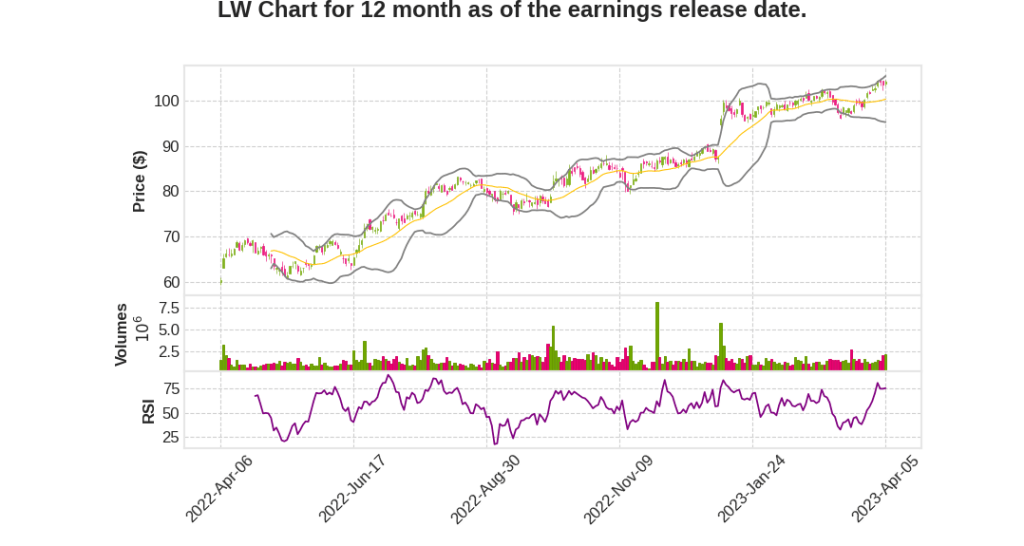

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q3 | 31.3% YoY | 99.0% | 160.4% | 2023-04-06 |

Bernadette Madarieta says,

Sales Growth

- Sales in Q3 were up 31% to $1.25 billion, and the company has increased its financial targets for the remainder of the year.

- The updated sales target for the year is $5.25 billion to $5.35 billion, up from the previous target of $4.8 billion to $4.9 billion, with $300 million to $325 million of the increase reflecting the consolidation of Lamb Weston EMEA.

- The additional $100 million to $150 million increase reflects strong results in Q3 and expected continued momentum in Q4.

Cost Inflation

- The company realized a double-digit increase in input and manufacturing cost per pound, driven by contracted prices for potatoes in North America and higher prices for open market potato purchases.

- There were also continued increases in the cost of edible oils, ingredients for batter coatings, labor, and energy.

Gross Profit and Margin

- Gross profit in Q3 increased $177 million to nearly $400 million, and gross margins expanded 860 basis points versus the prior year quarter to 31.7%.

- The strong gross margin performance reflects executing pricing actions to counter input and manufacturing cost inflation and improving customer and product mix and supply chain productivity.

- Expect a notable step down in Q4 gross margin from Q3 due to significantly higher cost open market potatoes, continued inflation for key inputs, and the impact of volume declines as a result of inflationary pressures on consumers.

Segment Performance

- Sales in the Global segment were up 33%, while the Foodservice segment grew 22%, and the Retail segment delivered another strong quarter with sales up 50%.

- Global’s product contribution margin increased to $168 million, while Foodservice’s product contribution margin increased to $143 million, and Retail’s product contribution margin increased to $83 million.

- The increased sales in the Global and Retail segments were aided in part by pricing actions across their branded and private label portfolios to counter inflation.

2023 Outlook

- Adjusted diluted earnings per share is targeted to be $4.35 to $4.50, up from the previous target of $3.75 to $4.

- Adjusted EBITDA including unconsolidated joint ventures is targeted to be $1.18 billion to $1.21 billion, up from the previous estimate of $1.05 billion to $1.1 billion.

- The full-year gross margin target excluding EMEA has been raised to 28% to 28.5%, implying a fourth-quarter gross margin target excluding EMEA of 25% to 27%.

- Expect expenses excluding items impacting comparability of $550 million to $570 million, up from the previous target of $525 million to $550 million.

- The capital expenditures estimate has been increased to between $500 million to [unknown].

Tom Werner says,

Strong Q3 Results

- Sales grew by 31%, gross margins expanded in each of the core business segments, driving strong EBITDA and EPS growth

- Revenue growth management and execution capabilities have been built to counter input cost inflation

Acquisition of Lamb Weston EMEA

- Over 1,500 new colleagues from Lamb Weston EMEA have joined the global team

- Lamb Weston EMEA adds six factories and about 2 billion pounds of production capacity to the global manufacturing footprint

- It strengthens the ability to serve customers in key markets around the world and enhances a world-class management, operating, and commercial team with deep knowledge of the frozen potato industry

Current Operating Environment

- Total restaurant traffic improved versus the prior year quarter

- QSR accounted for the entire growth in traffic, including strong growth across burger and chicken restaurant chains

- Traffic at casual dining and full service restaurants fell versus the prior year, contributing in part to a decline in the Foodservice segment’s volume

- Demand for fries and food-at-home channels remained solid

Pricing Expectations

- The environment for pricing actions to counter input cost inflation may remain generally favorable

- In the Global segment, we don’t expect any additional notable pricing actions to take effect

- In Foodservice, the year-over-year growth rate and price/mix will decelerate as we continue to lap more of the fiscal 2022 pricing and mix improvement actions

- In Retail, the year-over-year growth rate and price/mix will also decelerate as we continue to lap last year’s pricing actions

Potato Crop in North America and Europe

- Enough open market potatoes have been secured to meet production forecast until the early potato varieties are harvested in July

- Contract prices for potatoes grown in the Columbia basin are up by nearly 20%

- In North America, contract prices are largely in line with the 20% increase in the basin

- In Europe, contract prices are up significantly to reflect input cost inflation for growers

Updated Financial Outlook

- Financial targets for the year have been raised based on strong Q3 results

- Category demand remains healthy, and industry Q3 supply should remain constrained for at least the next couple of years

Q & A sessions,

rant traffic trends. Here are the key takeaways from the speech that are likely to have a significant impact on the stock’s movement:

Pricing Actions and Inflation

- Lamb Weston has taken pricing actions at the end of Q3 to counter input cost inflation and will continue to evaluate the overall inflation number as they roll up their plan for fiscal 2024.

- Crop cost is expected to be up 20%, and the company is not in a deflationary period.

- They will determine the pricing actions they may have to take, as they do every year, based on the overall input cost complex.

- The company has done a good job of offsetting inflation through catch-up pricing and will continue to do so.

Volume and Category Demand

- The overall volume of the category is expected to be good, with QSRs performing tremendously well in terms of traffic.

- The casual dining segment is seeing some softness due to economic factors, and people are trading down.

- The company has rationalized its customer and product mix over the last 12 to 15 months as part of its revenue growth management initiative.

- As the company gets its operations running back to a higher throughput level, it expects opportunities to take on more business going forward.

Capacity Expansion

- Lamb Weston has a lot of capacity coming on, with the first capacity turn off in China this fall.

- The company is evaluating how that will look in terms of production shifts from North America to China and is preparing to evaluate opportunities around the globe as it turns that capacity on.

- The company expects to have American Falls, Argentina, and other capacity turns off over the next 18 to 24 months.

Financial Performance

- The company delivered strong results in its Q3, with sales growing 31%, gross margin expanding in each of its core business segments, and strong EBITDA and earnings per share growth.

- The company raised its financial targets for the year and is continuing to build good operating momentum across each of its core segments.

Potato Crop and Contracting Process

- The company believes it has secured enough open market potatoes to meet its production forecast until the early potato varieties are harvested in July.

- The company has agreed to a nearly 20% increase in contract prices for potatoes grown in the Columbia Basin and has locked in the targeted contracted acres to be planted in that region.

- The company is in the process of securing most of the acres in its other growing regions in North America and expects to have this process completed shortly with contract prices largely in line with the 20% increase in the basin.

- In Europe, the company has secured the acres in its key growing regions and expects to complete the contracting process shortly, with contract prices up significantly to reflect input cost inflation for growers.