Tractor Supply Company

CEO : Mr. Harry A. Lawton III

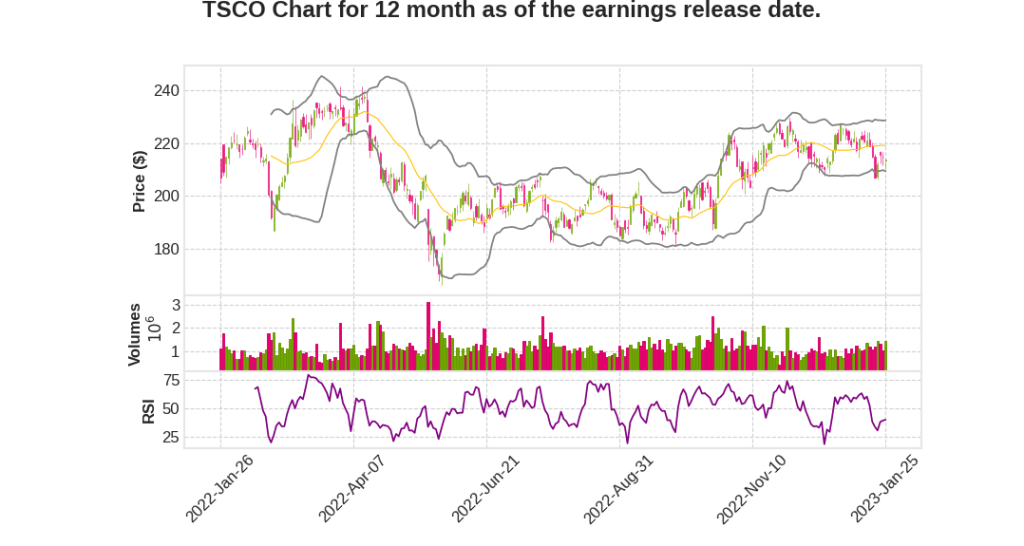

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 20.7% YoY | 22.6% | 25.6% | 2023-01-26 |

Hal Lawton says,

Revenue and Earnings

- Record sales growth of 11.6% and diluted earnings per share growth of almost 13% for FY2022

- $14.2 billion in revenue and over $1 billion in net income

Comparable Store Sales Growth

- FY2022 Q4 comparable store sales growth of 8.6%

- Strong ticket growth of 6.3% and transaction count increase of 2.3%

- Consumable, usable, and edible products outperformed overall comp sales results for the seventh consecutive quarter, running at about 3x the rate of overall comp sales growth

Neighbor’s Club and Credit Card Sales

- Neighbor’s Club membership exceeded 28 million members and represented nearly 75% of sales for the year

- Launched Tractor Supply, Visa Credit Card which allows customers to earn more on their everyday purchases, both in-store and anywhere Visa is accepted

- Crossed over $1 billion in private label credit card sales

Supply Chain and Sustainability

- Moved more than 8 billion pounds of consumable, usable, and edible products through the supply chain

- Supply chain is a competitive advantage with a lower cost to serve as the world’s largest seller of back feed and food for livestock in campaign and animals

- Committed to achieving net 0 emissions across all operations by 2040

- Announced a three-year water conservation goal to conserve 25 million gallons of water by 2025

2023 Outlook

- Anticipate continuing to operate in an ever-challenging and changing macro environment with flat to modestly positive real growth

- Believe inflation has peaked, but will remain sticky as we move through the year

- Confident that the business will remain resilient and build on the strong track record of consistent and stable growth across all economic environments

Kurt Barton says,

Impact of winter storm on Q4 2022 earnings

- The Winter Storm Elliott provided about a 2 percentage point benefit to Tractor Supply’s comp sales in mid-December 2022

- Profitability of winter storm events is lower due to the mix of products and higher incremental operating costs

Gross margin and operating expenses

- Gross margin improved by 28 basis points for Q4 2022, reaching 34% of sales

- Price management actions and other margin-driving initiatives offset the pressures from product cost inflation, higher transportation costs, and product mix

- Transportation costs may have peaked in Q4 2022

- SG&A expenses, including depreciation and amortization, increased by 14 basis points YoY to 25.1%, primarily due to transaction expenses and early integration costs associated with the acquisition of Orscheln Farm and Home, strategic growth initiatives, and investments in team member compensation and benefits

Guidance for fiscal year 2023

- Tractor Supply forecasts net sales of $15 billion to $15.3 billion, including at least $300 million in sales from Orscheln

- Comparable store sales growth is anticipated to be in the range of 3.5% to 5.5%

- Gross margin expansion of about 20 to 40 basis points from supply chain benefits and a moderation in both product cost increases and the mix impact of C.U.E.

- SG&A is expected to deleverage modestly due to strategic growth initiatives, depreciation and amortization relating to strategic growth initiatives, and the opening of a new distribution center

- Operating margin is forecasted to be 10.1% to 10.3%

- EPS is forecasted to be $10.30 to $10.60

- Capital expenditures are forecasted to be $700 million to $775 million, with about 80% for growth initiatives

Long-term outlook

- Tractor Supply’s outlook for 2023 is consistent with their long-term EPS guidance of 8% to 11%, adjusting for the 53rd week benefit and the Orscheln acquisition accretion

- Tractor Supply plans to open approximately 70 new stores in 2023 and remains committed to returning cash to shareholders through a growing dividend and share repurchases

Q & A sessions,

Consistent Performance

- Tractor Supply has a track record of delivering positive sales growth for over 30 consecutive years.

- They have consistent traffic growth across economic cycles and are planning for positive traffic growth in 2023.

- Tractor Supply’s queue product categories are driven by livestock feed and other products. They are entering new product categories through their Garden Center transformations.

Reliable

- Tractor Supply is a need-based, demand-driven business, which sets them apart from other retailers.

- The company’s Neighbor’s Club program has increased high-value customers by nearly 50%, which has increased spending reliability.

Sustainable

- Tractor Supply has added tens of millions of new customers in the past three years, with over 13 million members added since 2019 alone.

- The millennial customer base, which makes up nearly a quarter of the US population by 2032, is showing accelerated rates of home ownership and household formation, which supports sustainable outlook for the company.

- Rural revitalization is driving net migration out of urban areas towards the rural lifestyle, which appeals to millennials and their passions and hobbies.

Comp Sales Guidance for 2023

- Tractor Supply expects comp sales for 2023 to be between 3.5% and 5.5%

- They expect a blend of transacts and inflation to be stronger in the first half and moderate in the second half.

- Tractor Supply is taking significant share in the marketplace and expects share gain to continue in 2023.

Investment Cycle and Margin Rate

- Tractor Supply is in the midst of an investment cycle, with this year and last year being the two biggest peaks.

- The company anticipates growing sales and earnings at a significant rate even during this investment cycle.

- They expect opportunities to increment up on their operating margin towards that higher end in the coming years.