Mastercard Incorporated

CEO : Mr. Michael Miebach

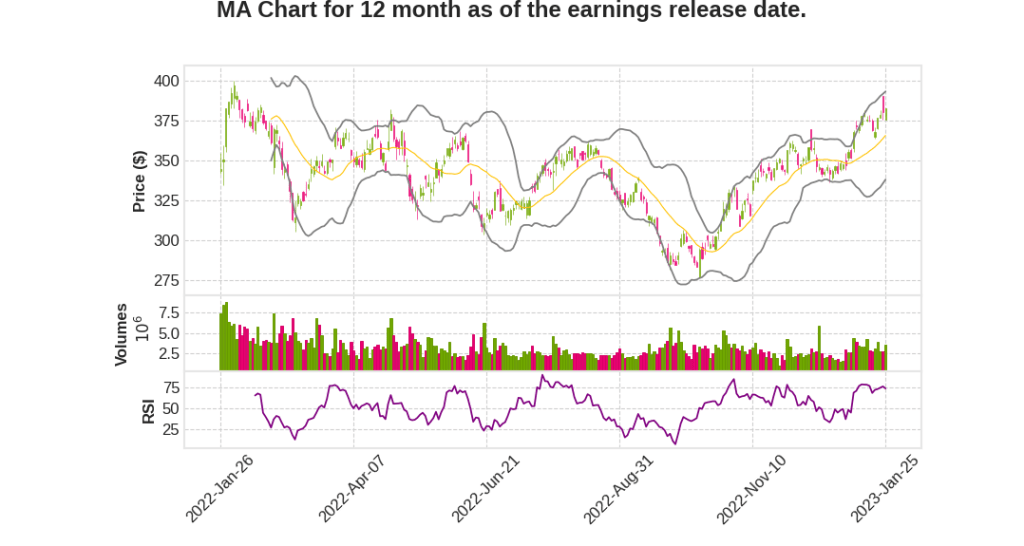

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 11.5% YoY | 8.6% | 8.7% | 2023-01-26 |

Michael Miebach says,

Financial performance:

- Q4 net revenues up by 17% and adjusted operating income up by 19% YoY, on a non-GAAP currency-neutral basis, excluding special items.

Consumer spending:

- Consumer spending has remained resilient, with key drivers being a broadly resilient labor market, rising wages, and elevated consumer savings levels.

- Spending patterns have largely normalized relative to the effects of the pandemic with the notable exception of China.

- In terms of switched volumes, domestic volumes in Q4 remained steady relative to 2019 levels with some slight moderation in the U.S. related to lower gas prices recently.

Expansion in payments:

- Mastercard won substantial new business this quarter and expanded several partnerships with banks and co-brand partners.

- Mastercard’s work in installments, tokenization, and click-to-pay is bringing innovation and thought leadership to the industry.

- Mastercard is making significant progress expanding in payments and has a strong pipeline of new programs across multiple regions.

Services:

- Mastercard’s services continue to drive growth in the core and provide differentiation and diversification for the company.

- Mastercard is expanding its services to new segments and use cases, including governments, retailers, digital partners, and financial institutions.

Embracing new networks:

- Mastercard is actively working with JPMorgan Chase to take their open banking solution to market this year, which utilizes Mastercard’s open banking platform to modernize existing ACH payments and allow customers to pay bills from their bank account in a frictionless manner.

- Mastercard is connected to more than 3,000 banks and financial institutions across 18 markets to power their open banking efforts.

Sachin Mehra says,

Revenue Growth and Acquisitions

- Net revenue increased by 17% year-over-year, supported by a resilient consumer spending and the continued recovery of cross-border travel relative to 2019 levels.

- Acquisitions contributed 1 ppt to this growth.

Operating Expenses

- Operating expenses increased 13%, including a 3 ppt increase from acquisitions.

- Excluding acquisitions, the remaining increase was primarily due to higher personnel costs to support the continued execution of strategic initiatives.

Operational Metrics

- Worldwide gross dollar volume (GDV) increased by 8% year-over-year on a local currency basis, with credit growth of 14% reflecting the recovery of spending on travel.

- Contactless now represents 56% of all in-person switched purchase transactions.

- Cross-border volume was up 31% globally for the quarter, reflecting continued improvement in travel-related cross-border spending.

Guidance for 2023

- Base case scenario for the full year 2023 is for net revenues to grow at the high end of a low-double-digit rate on a currency-neutral basis, excluding acquisitions and special items.

- For the year, we expect operating expenses to grow at the high end of a high-single-digit rate on a currency-neutral basis, excluding acquisitions and special items.

- Year-over-year net revenue growth is expected to be at the low end of a low-double-digit rate for Q1 2023, on a currency-neutral basis excluding acquisitions and special items.

Other Information

- The non-GAAP tax rate is expected to be approximately 18% in Q1 and 18% to 18.5% for the year based on the current geographic mix of the business.

- During the quarter, they repurchased $2.4 billion worth of stock and an additional $590 million through January 23, 2023.

Q & A sessions,

expected impact on Mastercard’s stock movement based on the MA Q4 2022 earning call transcript:

Resilient consumer spending through 2023

- Expectation of resilient consumer spending pattern going forward with growth at a healthy pace, but not accelerating pace

- Assumption of increase in growth in Asia Pacific with recently opening borders

Rebates and incentives

- Building in assumptions for rebates and incentives consistent with winning new and expanding business with existing customers

Cross-border and FX rates

- Fundamentals around cross-border proposition sound, but capacity constraints and elevated prices expected to impact spend

- FX rates historically have an impact on inbound cross-border spend and redirecting cross-border spend to other parts of the globe

Stable growth across regions

- Stable levels in Q4 2022 for switched volumes and transactions in cross-border, marginally up quarter-over-quarter

- Remarkably consistent growth in most regions, with China and India impacted negatively due to COVID and old card attrition, respectively

Impact of average ticket size

- Impacted by inflation, mix between card-present and card-not-present, and delivery of more services