Martin Marietta Materials, Inc.

CEO : Mr. C. Howard Nye

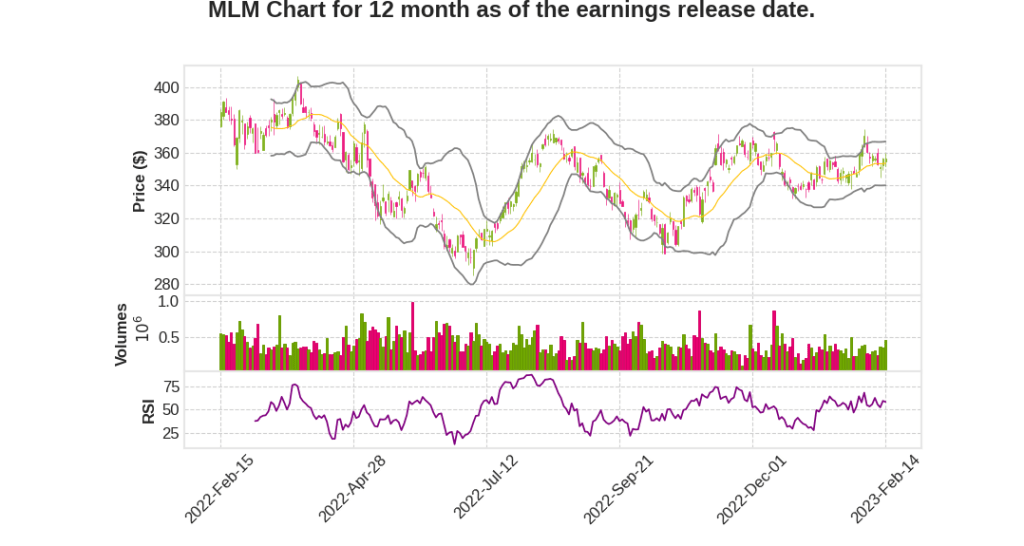

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -1.3% YoY | 26.3% | 17.9% | 2023-02-15 |

Jim Nickolas says,

Record-breaking Results in Building Materials Business

- The building materials business achieved record products and services revenues of $5.45 billion, a 13.4% increase over last year.

- The product gross profit also reached a record of $1.34 billion, an 8.1% increase.

Success in Cement Business

- The Texas cement business achieved an all-time record top and bottom-line results with product revenues increasing by 21.8% to $602 million.

- Product gross profit also improved by 30.1% to $204 million, with product gross margin expanding by 210 basis points to 33.9%, despite significant energy cost headwinds.

- Shipments since 2019 are up 8%, while product revenues are up 37%, demonstrating the team’s commitment to commercial excellence.

Midlothian Plant Initiatives

- The Midlothian plant has several initiatives underway to improve production capacity including the installation of a new finish mill expected to be completed in Q3 2024.

- Conversion to less carbon intensive Portland limestone cement, also known as Type 1L, is complete at both Midlothian and Hunter plants, resulting in growing production volumes by 5% in 2022 compared to 2021 levels.

- The conversion to Type 1L is expected to provide an additional capacity expansion of 5% in 2023.

Decline in Ready Mixed Concrete Product Revenues and Gross Profit

- Ready mixed concrete product revenues declined 17% to $931 million, and product gross profit declined 27.2% to $70 million, driven primarily by the divestiture of Colorado and Central Texas operations and partially offset by contributions from the acquired Arizona operations impacting prior-year comparability.

- Increased aggregates and cement costs also weighed on gross margin, which declined 100 basis points to 7.3%.

Net Debt-to-EBITDA Ratio

- Exiting the year with a strong balance sheet, the net debt-to-EBITDA ratio was 2.5 times.

- Capital allocation priorities remain focused on prudent investments in attractive upstream acquisitions, organic growth initiatives and returning capital to shareholders.

Ward Nye says,

Q4 2022 Highlights

- Aggregates shipments decreased 12% against the prior year quarter due to weather impacts.

- Aggregates pricing increased 16.5%, providing tailwinds into 2023.

- Aggregates gross margin expanded and improved gross profit per ton shipped by 25% over the prior year quarter despite weather impacts.

Full Year 2022 Results

- Consolidated products and services revenues of $5.7 billion, a 13% increase.

- Consolidated gross profit of $1.4 billion, a 6% increase.

- Adjusted EBITDA of $1.6 billion, a 5% increase.

- Double-digit pricing growth across all building materials product lines.

- Inflationary pressures impacted operating costs and affected product gross margin, which declined 160 basis points to 24.9% for the year.

Aggregates Performance

- Total aggregate shipments increased 3.3% to 208 million tons.

- Aggregate pricing increased 10.6% or 10% on a mix adjusted basis.

- Texas cement market experienced robust demand and tight supply with record yearly shipments of 4.2 million tons and pricing growth of 16.9%.

Targeted Downstream Businesses Performance

- Ready mixed concrete shipments decreased 25.4% and pricing increased 11.3%.

- Asphalt shipments increased 28.4% and pricing improved 23.6%.

2023 Outlook

- Expect meaningful pricing acceleration and margin expansion in 2023 due to multiple commercial actions enacted in 2022 and broad customer support of January 1st, 2023 price increases.

- Favorable Texas cement commercial dynamics expected to continue based on market trends and success of January 1st price increases.

Q & A sessions,

Expected Impact on Stock Movement

- Martin Marietta’s prospects for 2023 and beyond are expected to be positive, building upon the foundation established in 2022.

- Historic legislation including the Infrastructure Investment and Jobs Act, Inflation Reduction Act, and CHIPS Act are expected to support multiyear demand for Martin Marietta products across infrastructure and heavy nonresidential construction sectors.

- State and local governments’ highway, bridge and tunnel contract awards grew 24% to a record $102 billion in 2022, indicating future demand.

- The company anticipates flat aggregates shipments at the midpoint of guidance, as increased infrastructure investment, coupled with robust activity from heavy nonresidential projects of scale, will insulate product shipments from a residential slowdown and a related moderation in light commercial construction.

- Martin Marietta expects aggregates pricing growth of 13% to 15%, with the midpoint at 14%, which does not include any midyear price increases.

- Consolidated adjusted EBITDA is expected to be $1.8 billion to $1.9 billion or a 15.6% growth year-over-year at the midpoint.