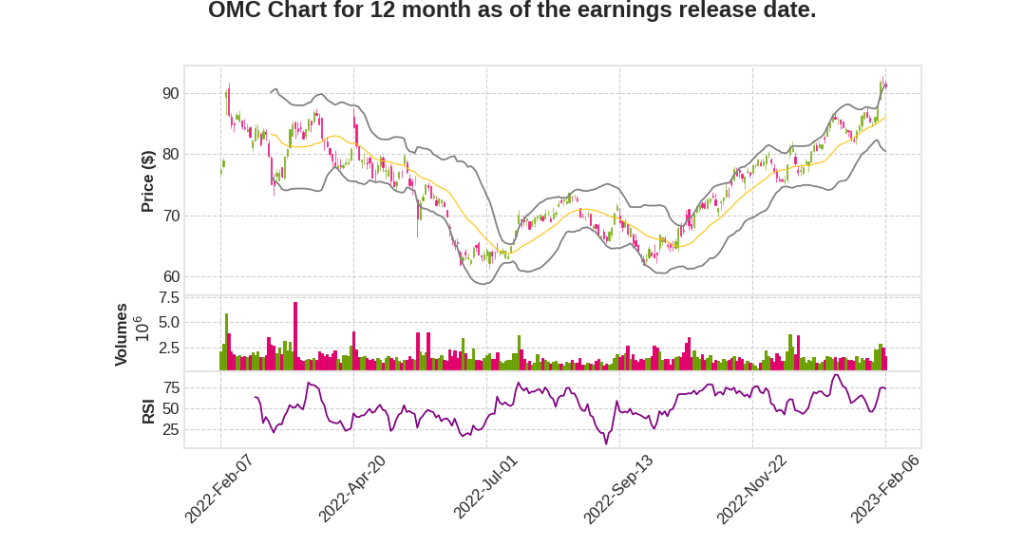

Omnicom Group Inc.

CEO : Mr. John D. Wren

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 0.3% YoY | -8.1% | 1.0% | 2023-02-07 |

Phil Angelastro says,

Revenue and Organic Growth

- Reported total revenue in Q4 2022 was flat year-over-year at $3.9 billion with organic growth of 7.2%, offset by the negative impact of foreign currency translations and net disposition revenue in excess of acquisition revenue.

- Organic growth was 9.4% year-to-date.

- Organic growth was seen across all disciplines except for execution and support, which was expected.

- Advertising & Media, Precision Marketing, Commerce & Brand Consulting, Experiential, and Public Relations showed strong organic growth.

Expenses and Profit

- Total expenses were essentially flat at $3.2 billion due primarily to the weakening of almost all foreign currencies against the U.S. dollar.

- Operating profit for Q4 2022 increased 3.2%; and on a constant currency basis, it increased 8.4%.

- The operating profit margin reached 16.6% on total revenue compared to last year’s margin of 16.1%.

Cash Flow and Debt

- Free cash flow for the year was approximately $1.8 billion, flat compared to last year.

- Net stock repurchases for the year were $594 million, at the high end of expectations.

- The $2.5 billion revolving credit facility remains undrawn.

- Return on invested capital was 28% and return on equity was 40% for the 12 months ended December 31, 2022.

Guidance

- Interest expense in 2023 is expected to approximate 2022 levels, with interest income expected to increase moderately in Q1 and Q2 of 2023 compared to the first half of 2022 and approximate 2022 levels in the second half of 2023.

- The effective book income tax rate in 2023 is expected to be approximately 27%.

- If foreign currency exchange rates stay where they were as of February 1, the impact will reduce revenue by approximately 3% in the first quarter and moderate for the remainder of 2023 to be approximately flat for the year.

- The impact from net acquisitions and dispositions will result in a reduction of revenue by approximately 1.5% in the first quarter, primarily resulting in the disposition of businesses in Russia in the first quarter of 2022.

John Wren says,

Organic Growth and Performance

- The company reported strong organic growth of 7.2% in the fourth quarter, exceeding expectations, with double-digit growth in Precision Marketing, Public Relations, and Experiential disciplines.

- Full-year organic growth was 9.4%, and operating margin for the quarter was 16.6%, increasing 50 basis points compared to the prior year.

- Earnings per share for the quarter was $2.09, up 7.2% versus the fourth quarter of 2021, with a negative currency impact on EPS of approximately 6%.

- The company generated over $1.7 billion in free cash flow and returned more than 65% to shareholders in dividends and share repurchases.

New Business Wins

- Omnicom Media Group was named L’Oreal’s U.S. media agency of record, with an estimated $1 billion in U.S. media billings.

- OMD was named media agency of record for Burberry.

- The Healthcare Group won a significant new business pitch with Merck.

Talent and Expansion

- The company added new leaders to its team, including Kathleen Saxton as Chief Marketing Officer and Alex Hesz as Chief Strategy Officer, to strengthen its position in the marketplace and identify new business opportunities.

- The company expanded its e-commerce capabilities through its partnership with Albertsons Media Collective, providing first-to-market solutions for better targeting and measuring ROI in connected TV environments.

Guidance and Caution

- The company is targeting 2023 organic revenue growth of 3% to 5% and expects its operating margin to be between 15% and 15.4%.

- The company remains cautious of macroeconomic and geopolitical factors, including the ongoing war in Ukraine, rising interest rates, and higher inflation around the world, and is actively developing plans to respond to these headwinds.

Q & A sessions,

Guidance

- The company is comfortable with 3%+ growth in the near future due to stability in client base and net new business wins.

- The company expects the wins from the latter part of 2022 to contribute to Q2 2023 and beyond.

- The company is cautious about payroll environment and planning for a full year’s cost for incremental employees.

E-commerce and Retail

- The company believes that COVID has accelerated online sales and it is only going to further increase in the future.

- The company has been building e-commerce capabilities for well over 2.5 years and it will play a vital role in future business.

Acquisitions and Divestitures

- The company is interested in mergers and acquisitions in e-commerce, geographic expansion, and skill expansion of precision marketing and healthcare groups.

- The company constantly reviews the portfolio and talks to people through M&A group about doing roll-ups in certain areas.

Automation

- The company constantly invests in automating part of the functions that they perform on a regular basis.

- All of the automation that the company is looking at enhances the capabilities and makes the job easier for best and brightest people.

Pricing Increases

- The company has had some success in going to clients and getting increases in pricing.

- The company believes that clients understand the best and brightest people that are servicing them can demand more due to inflationary periods.