Principal Financial Group, Inc.

CEO : Mr. Daniel Joseph Houston

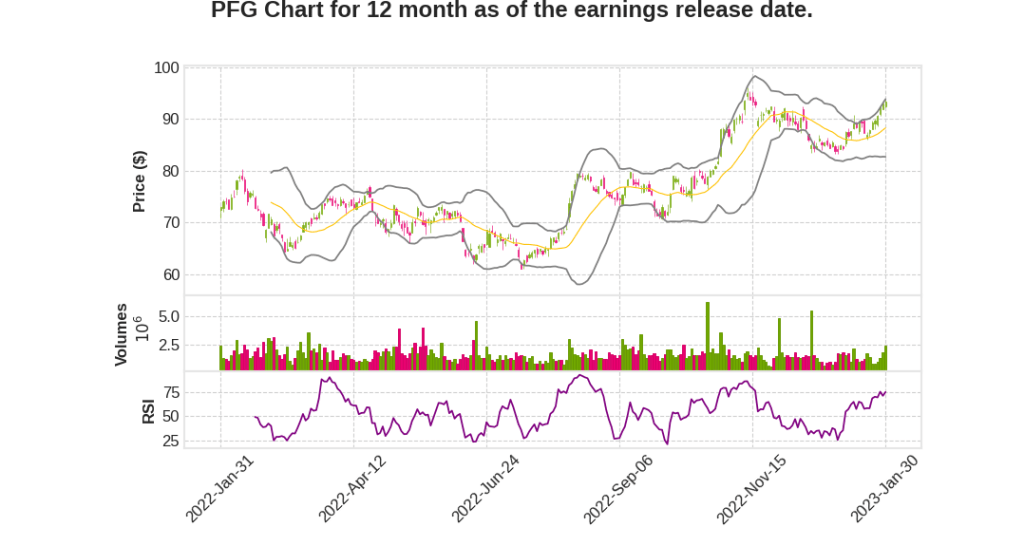

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -23.7% YoY | -103.5% | -96.9% | 2023-01-31 |

Deanna Strable says,

Financial Performance

- Full year reported net income attributable to principal was $4.8 billion, excluding income from exited businesses net income was $1.5 billion for the full year with manageable credit losses of $48 million.

- Fourth quarter non-GAAP net income, excluding exited businesses was $504 million with $12 million of credit losses.

- Full year non-GAAP operating earnings was $1.7 billion or $6.66 per diluted share including $422 million or $1.70 per diluted share in the fourth quarter.

- Compared to full year 2021, we increased earnings per share 2% as the benefit from share repurchases and strong customer growth was partially offset by macroeconomic pressures on earnings.

RIS-Fee Business Unit

- RIS-Feeâs margin improved in the fourth quarter, but end of the year below guidance as the benefit from IRT expense synergies was more than offset by unfavorable market performance, which pressured fees and net revenues throughout the year.

- Through the end of 2022, weâve realized more than $80 million of run rate expense synergies and are well on track to realize the full $90 million in 2023.

PRT Pipeline

- We completed $1.9 billion of pension risk transfer sales in 2022, including more than $750 million in the fourth quarter. The PRT pipeline remains very strong as we head into the first quarter.

Capital and Liquidity

- We ended 2022 with $1.5 billion of excess and available capital.

- We returned $2.3 billion to shareholders in 2022, including nearly $1.7 billion of share repurchases and more than $640 million of common stock dividends.

LDTI Implementation

- LDTI goes into effect in the first quarter. Importantly, this doesnât change our underlying economics, free cash flow generation or our capital position, but it will have an impact on our reported financial results.

- The most notable impact to total company non-GAAP operating earnings is a change to the geography of some variable annuity fees, moving the hedging related fees below the line. This will reduce our operating earnings by approximately $60 million on an annual basis with no corresponding impact to net income, free cash flow generation or our capital position.

Pat Halter says,

Operating margins and revenue

- Q4 operating margin was 36.8%, down from Q3’s 38.4% due to lower average AUM in terms of fee generation caused by investor risk aversion and volatility.

- Management is focused on aligning expenses with revenue and eliminating activities that aren’t producing growth and revenue contribution for the organization.

Expense management

- The focus is on managing expenses and aligning them with revenue, given the challenging marketplace.

- The management team is disciplined in expense management and will continue to invest in talent where necessary for long-term growth and revenue for the organization.

- Severance expenses in Q4 were around $5 million, and expenses for the year were up around 2% year-over-year.

Client interest and growth centricity

- The team is focused on serving clients well and investing where the organization can maintain long-term growth and revenue.

- The distribution is important to the organization’s growth, and private investment capabilities will be further developed.

Q & A sessions,

VA Business and LDTI Process

- Managed $9 billion enforce block of VA business

- Split fees between hedging and non-hedging fees based on better information through LDTI process

- VA business is a key part of the retirement franchise

- $60 million expected enterprise impact from LDTI with additional impacts on operating earnings

Outlook and Excess Capital

- $2.3 billion full year results, slightly lower than $2.5 billion to $3 billion outlook due to macro pressures

- Excess capital in holdco and lifeco was virtually $300 million at the end of the year

- Volatility and uncertainty on 2023 led to a decision to be prudent in capital deployment and management

- Approach to capital deployment and management consistent with 2022

Net Investment Income and Expenses

- Positive impact from higher interest rates on new investments, cash, escrow and PGI

- Credit back out to customers in BC&S line in RIS

- Bank and trust business in RIS benefits from higher interest rates

- Expenses aligned with revenue changes, good progress on realization of synergies in RIS and managing stranded costs

Investment Performance and Flows

- Real estate experienced a slowdown in new investment activity in Q4 due to market conditions but has a deep strong pipeline of committed capital

- Net cash flow for 2022 was $3.9 billion, up from $2.9 billion in 2021

- Fixed income investments in preferred, high yield, and emerging market debt performed well on Morningstar performance on one, three, and five-year basis

- Real estate debt and private credit space saw strong performance and expected flows in the second half of 2023

Portfolio Resilience to Recession Environment

- Disciplined bottom-up perspective on commercial mortgage and fixed income portfolios

- Top-down stress analysis of portfolio