PulteGroup, Inc.

CEO : Mr. Ryan R. Marshall

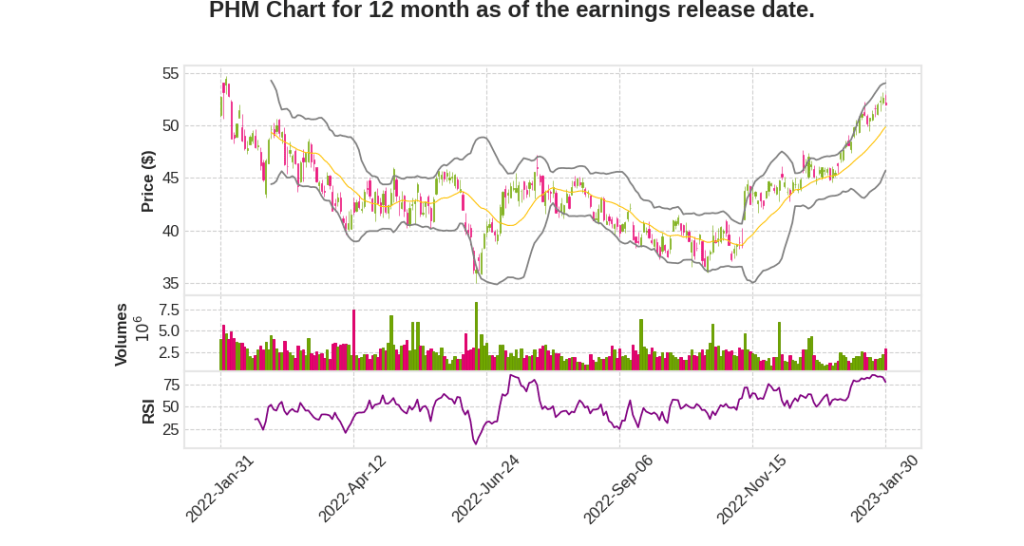

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 18.6% YoY | 35.0% | 123.4% | 2023-01-31 |

Bob OâShaughnessy says,

Home Sale Revenues

- Q4 home sale revenues increased 20% over last year to $5.1 billion

- Higher revenues were driven by a 3% increase in closings to 8,848 homes and a 17% increase in average sales price to $571,000.

New Orders and Cancellations

- Net new orders of 3,964 homes, which is a decrease of 41% from the same period last year due to ongoing softness in buyer demand

- Cancellation rate in the fourth quarter was 32% compared with 11% last year

Backlog

- Ended the quarter with a backlog of 12,169 homes with a value of $7.7 billion, compared to 18,003 homes with a value of $9.9 billion in the prior year

Gross Margins and SG&A Expenses

- Reported gross margins of 28.8%, up 200 basis points over the comparable prior year period

- Reported SG&A expense of $351 million, or 6.9% of home sale revenues

- Expect SG&A expense in Q1 to be in the range of 10.5% to 11% compared to 10.7% last year

Land Acquisition and Development

- Invested $1.1 billion in land acquisition and development in the fourth quarter, with almost 65% of this spend for development of existing land assets

- Ended the year with 211,000 lots under control, down 8% from last year and down 13% from the recent Q2 peak of 243,000 lots

- Expect total land investment to be approximately $3.3 billion in 2023

Share Repurchases and Dividends

- Repurchased 2.4 million common shares at a cost of $100 million in Q4

- Returned over $1.2 billion to shareholders through share repurchases and dividends in 2022

Ryan Marshall says,

Q4 2022 Results

- PulteGroup closed almost 8,900 homes and earned $5.1 billion in homebuilding revenues and $3.85 per share in Q4 2022.

- The company finished the year with over $1 billion in cash and a net debt-to-capital ratio below 10%.

Financial Results for 2022

- For 2022, PulteGroup’s home sale revenues increased 18% over the prior year to $15.8 billion, pre-tax earnings increased by 37% to $3.4 billion and reported earnings increased 48% to $11.01 per share.

- The company invested $4.5 billion into the business, while returning over $1.2 billion to shareholders, dividends, and share repurchases.

Market Conditions and Demand

- The Federal Reserve’s decision to hike rates 7x in 2022 and fight against inflation is successfully slowing the economy, including housing.

- For the full year, national new and existing home sales across the country fell by 16% and 18%, respectively, from 2021.

- Despite the higher rate environment dominating the national conversation, PulteGroup saw buyer demand improve as the fourth quarter progressed and can confirm this strength continued through the month of January.

- Net signups both in absolute number and absorption pace increased as the fourth quarter progressed and through the month of January.

Incentives and Affordability

- PulteGroup implemented programs that enable consumers to buy homes in today’s higher-rate environment. The cost of these programs, which might include rate buydowns, lower lot premiums, or even price reductions, can be seen in the company’s higher Q4 incentives.

- The introduction of smaller floor plans is just part of a comprehensive effort to lower overall construction costs to help offset the pressure on the sales price.

Operating Plan and Guidance

- PulteGroup plans for a consistent cadence of new starts that would include starting spec homes on a pace consistent with spec sales.

- The company’s primary focus will be to deliver strong relative returns on invested capital through the cycle.

- In planning for 2023, PulteGroup expects to have a production universe that will allow it to close approximately 25,000 homes in 2023.

Q & A sessions,

Supply Chain Disruptions and Demand Environment

- Supply chain disruptions resulted in bottlenecks and extended build cycles

- Rising interest rates push consumers to sidelines leading to a more competitive market

Favorable Supply Dynamic

- Inventory of existing homes for sale is limited with only 2.9 months of supply

Operational Changes and Financial Position

- Enough units in production to meet demand and with production plans to continue turning assets

- Strong competitive position within the markets served

- Exceptional financial position with plenty of liquidity and no debt maturities for 3 years

Cost Side

- Affordability is the biggest challenge and will continue to be the theme in 2023

- Labor is likely to be stickier than material costs

- Aggressive goals set by procurement teams to reduce overall costs

Active Adult Space

- Buyers tend to be reactive but have options

- Thin resale inventory market

- Not as rate sensitive as move-up buyers

Sales Trajectory

- Affordability is driving the sales trajectory

- Production targeted at approximately 25,000 homes to close

- Rental business targeted to have about 1,500 homes per year once fully ramped up