Pinnacle West Capital Corporation

CEO : Mr. Jeffrey B. Guldner

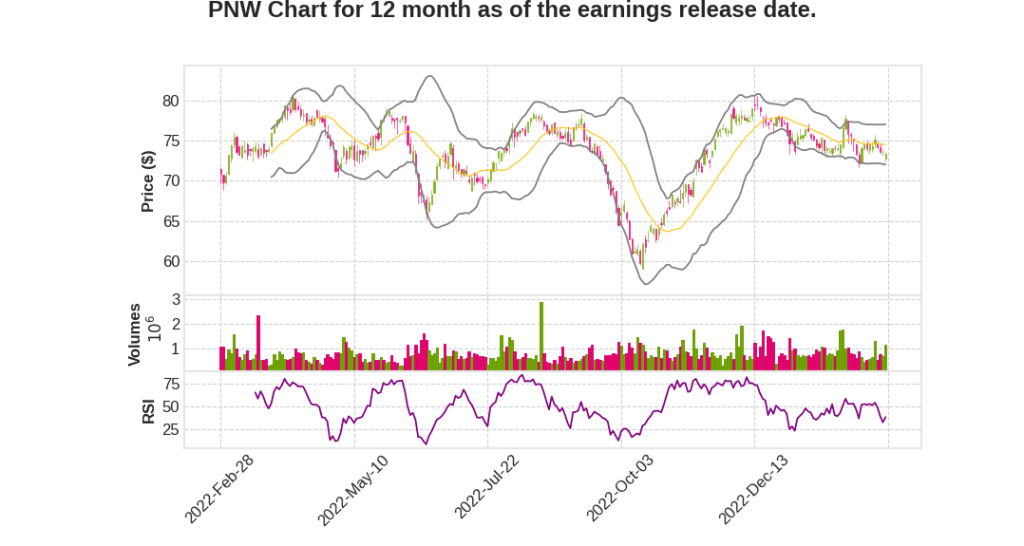

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 26.3% YoY | -26.5% | -187.5% | 2023-02-27 |

Andrew Cooper says,

Fourth Quarter 2022 Results

- Lost $0.21 per share, down $0.45 compared to fourth quarter 2021, due to lower net income from no longer deferring the costs related to Four Corners SCR and Ocotillo modernization project, an impairment charge relating to a Bright Canyon energy equity investment, lower LFCR revenues, higher O&M and interest expense, and unfavorable rate case decision.

- Beneficial weather and customer and sales growth partially offset the negative drivers in the fourth quarter.

Full-Year Results for 2022

- Earned $4.26 per share, down from $5.47 per share in 2021 due to the negative rate case outcome, Bright Canyon impairment charge, higher O&M, and higher interest expense.

- Beneficial weather and customer and sales growth partially offset the negative drivers for the year.

Financial Outlook for 2023

- 2023 earnings guidance range is $3.95 to $4.15 per share, comparable to the weather-normalized 2022 guidance range of $3.90 to $4.10 per share.

- Expect steady customer growth and robust sales growth, particularly in the C&I segments as economic diversification takes hold in areas such as semiconductor hubs and other large manufacturing and distribution.

- Expect weather-normalized sales growth range to be 3.5% to 5.5% for 2023.

- Higher benefit expense, interest expense, and plant D&A to be the headwinds for 2023.

- Expect the benefit expense to be a $0.33 headwind for 2023 as compared to 2022.

- Expect higher interest expense year-over-year as the Federal Reserve continues to raise interest rates.

- Updated the capital plan to $5.3 billion from 2023 to 2025 with rate base growth at an average annual growth rate of 5% to 7%, independent of any rate case outcome and directly related to loan growth and the needed investments in more resilient infrastructure.

Jeffrey Guldner says,

Key points from PNW Q4 2022 Earnings Call Transcript

- The previous rate case outcome had a significant impact on the company’s financials, but they have met or exceeded nearly every target they set for themselves

- The company has made progress in improving regulatory relationships and has seen constructive actions and decisions by the new regulatory bench

- The pending rate case is scheduled for hearing in early August, and the company aims to do what is right for the people and prosperity of Arizona by working collaboratively with the commission

- The company’s field team executed exceptionally well in 2022, prioritizing safety and achieving significantly lower employee injuries compared to previous years

- The company’s generation units performed extremely well, with a summertime equivalent availability factor of 95% and a capacity factor of 100.2% at the Palo Verde Generating Station

- The company’s customer experience improved significantly in 2022, with ratings from customers making it among the most improved utilities in the nation for both residential and business customer satisfaction

- The company procured over 2,100 megawatts of clean and affordable energy resources towards their goal of reaching 100% clean carbon-free energy by 2050

- Electricity capacity markets are tightening across the West, creating challenges for the company, but they believe in their ability to provide long-term value to both customers and shareholders

Q & A sessions,

Forecast for Q4 2022

- The forecast is driven by a diversified group of manufacturing, data center customers, and overall C&I growth in the service territory.

- There is an identified customer, TSMC, which is a considerable part of the large customers contributing to 2%-4% of the 3.5%-5.5% growth.

- 5%-7% earnings growth rate is expected through 2026.

Cost Management

- The sales growth rate in 2022 is expected to help mitigate inflation and O&M pressure.

- Cost levers will be used to manage the O&M pressure and keep a close eye on the macroeconomic environment and specific customers.

- Regulatory recovery is one path that the company continues to look at.

- Pension expense from a historical period is being considered as an option in the last rate case.

Investment Strategy

- The company has kept up with the necessary investments for load growth on the system.

- Opportunities around the generation side and tax credit framework set up by the IRA present the opportunity for more optimized mix the self-build.

- The clean tracker proposal could allow for more flow-through of clean investments.

- Further optimization of the mix of generation is possible after the rate case.