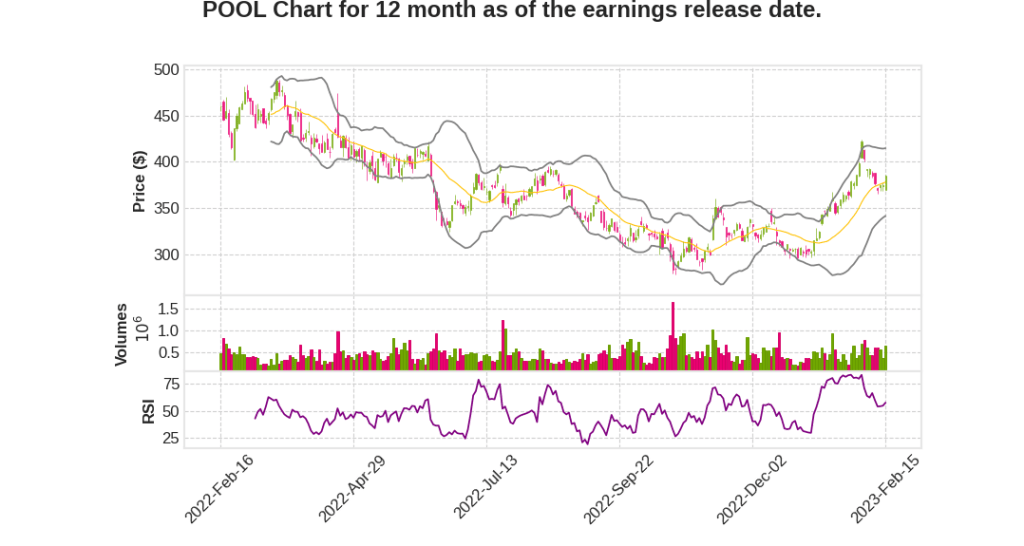

Pool Corporation

CEO : Mr. Peter D. Arvan

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 5.8% YoY | -16.1% | -31.3% | 2023-02-16 |

Peter Arvan says,

Revenue and Earnings

- POOLCORP exceeded $6 billion in net revenue, ending the year at $6.2 billion and generated just over $1 billion of operating income.

- For the full year, our base business grew by 15% in our year round markets and 8% in the seasonal markets.

Expansion and Acquisitions

- POOLCORP opened 10 new locations in 2022 and Pinch A Penny added seven new stores to the franchise network.

- POOLCORP acquired Porpoise Pool & Patio and successfully integrated it into their business model.

Market Growth and Share Gains

- POOLCORP provided best-in-class service to their customers, helping them grow their business and being the best channel to market for their suppliers.

- POOLCORP achieved results in revenue and earnings and grew their market share.

Product Sales

- Equipment, which represents about a third of POOLCORP’s sales, increased 9% for the year and 2% for the quarter.

- Base business chemical sales for the quarter were up 19% and 32% for the year, reflecting share gains, installed base growth and inflation.

- Building materials sales were up 18% for the full year.

Europe Market Performance

- Europe’s fourth quarter 2022 net sales were down 22.5% due to less favorable weather, elevated energy costs, inflation, and a slower economy.

- For the full year, we saw sales decline 15% in U.S. dollars.

2023 Outlook

- POOLCORP anticipates the value of goods and services related to the maintenance, renovation and construction of swimming pools and outdoor living to increase driven by unprecedented inflation that is now embedded in the industry.

- POOLCORP’s growing and aging installed base that will need to be maintained and remodeled, giving them confidence that 2023 will be a solid year.

Melanie Hart says,

Fourth Quarter 2022 Highlights

- The fourth quarter sales exceeded $1 billion for the second year in a row, marking steady growth.

- Gross profit percentage in the fourth quarter was 28.8%, with a 230 basis points decrease from the previous year, primarily due to import duties and taxes on certain imported chemical products.

- Operating expenses grew 7% to $208 million, and operating income declined by $21 million primarily due to lower gross profit in the quarter.

Full Year 2022 Recap

- Sales reached $6 billion, representing growth over the prior year of 17% top-line and 21% EPS growth, excluding the ASU.

- Market share growth includes 23 new greenfields opened since the beginning of 2020 and an increase in consumer interest in automating their pools, higher price point product spending, and expanded features in the backyard.

- Gross profit increased 20% and reached $1.9 billion. The gross margin improvement of 80 basis points reflects benefits from acquired sales and inventory-related gains from multiple vendor price increases throughout the year.

Expectations for 2023

- Guidance range based on flattish organic net sales to a decrease of 3% compared to 2022 as the company has lapped its larger acquisitions.

- Gross profit margin in 2023 expected to be in line with longer-term guidance of around 30% compared to the 31.3% gross margin reported in 2022.

- Operating margin expected to decline as much as 100 basis points to 150 basis points compared to 2022 full-year results.

- Cash flow from operating activities expected to exceed $800 million for the year.

Q & A sessions,

Expected decline in new pool construction

- The industry is expected to see a decline of about 16% in new pool construction in 2022 compared to 2021, with the final number to be confirmed soon.

- The company’s new construction numbers were down between 12% and 13%, indicating a pick-up in market share.

Impact of inflation on pool value

- The value of a pool has increased due to inflation, with the average pool estimated to be around $70,000.

- The value, however, varies based on geography and market demand.

Supply chain and customer experience

- Supply chains returned to almost normal in the back half of 2022, with availability not being an issue for most products.

- The company continues to take share due to its focus on customer experience and providing best-in-class service.

- Customers remain optimistic for the upcoming season, and the company’s dealers continue to provide high-end features to the pool structures.

Pricing fluctuations and long-term outlook

- Manufacturers’ prices are unlikely to retreat, and the industry does not expect wild pricing fluctuations in 2023.

- The company remains optimistic about the long-term outlook for the business, with the renovation market holding up better than new pool construction.

Maintenance spend and replacement upgrade behavior

- Replacement upgrade behavior is still going on, and the company has not seen a major shift in the parts business.

- The maintenance business is a function of usage and the aging of the installed base, with weather affecting the operating season on the pool.

- The replacement market is behaving as it normally has, and the company has not seen trends of deferring or repairing versus replacing.