Phillips 66

CEO : Mr. Mark E. Lashier

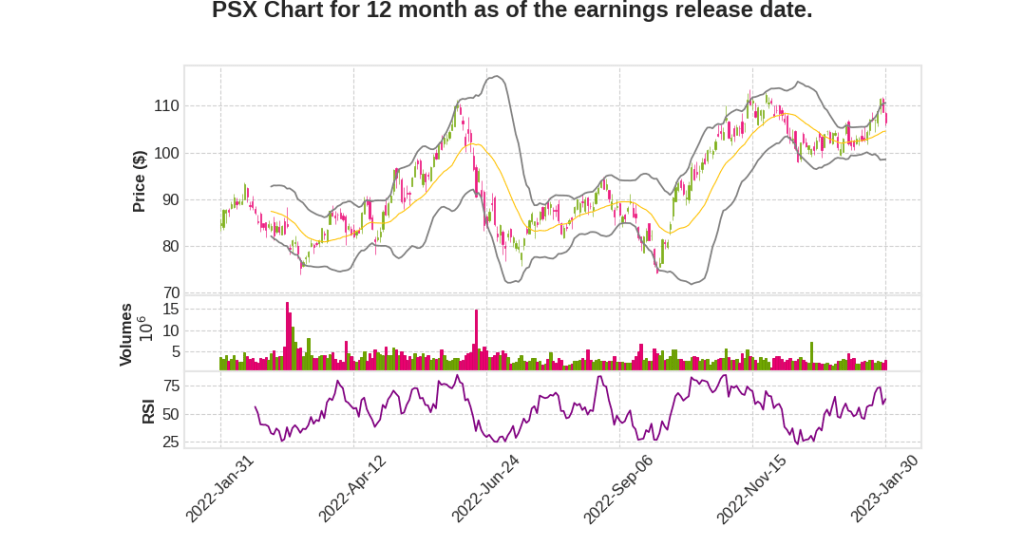

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | 41.1% YoY | 55.0% | 28.6% | 2023-01-31 |

Kevin Mitchell says,

Financial Results

- Adjusted earnings were $8.9 billion or $18.79 per share for the year, with fair value of investment in NOVONIX reducing earnings per share by $0.71.

- Operating cash flow was $10.8 billion, cash distributions from equity affiliates were $1.7 billion, and net debt-to-capital ratio was 24% at the end of 2022.

- Adjusted earnings were $1.9 billion or $4 per share for the fourth quarter, with fair value of investment in NOVONIX reducing earnings per share by $0.02.

- Capital spending for the quarter was $713 million, including $310 million for growth projects.

- Returned $1.2 billion to shareholders through $456 million of dividends and $753 million of share repurchases.

Midstream and Chemicals Results

- Fourth quarter adjusted pretax income for Midstream was $674 million, with Transportation contributing to pretax income of $237 million and NGL and Other adjusted pretax income of $448 million.

- Chemicals had fourth quarter adjusted pretax income of $52 million, mainly due to lower margins and volumes.

Refining Results

- Refining had fourth quarter adjusted pretax income of $1.6 billion, primarily due to lower realized margins. Realized margins decreased by 27% to $19.73 per barrel, while the composite 3 to 1 re-adjusted market crack decreased by 16%.

- Market capture was 84%, compared to 95% in the previous quarter.

- Refining turnaround expenses were $236 million in the fourth quarter, with expected expenses between $240 million and $270 million for the first quarter of 2023 and between $550 million and $600 million for the full year.

Financial Outlook

- Corporate and Other costs are expected to come in between $230 million and $260 million for the first quarter and in the range of $1 billion to $1.1 billion for the full year.

- Full year D&A is expected to be about $2 billion, and the effective income tax rate to be between 20% and 25%.

- The company expects to spend $310 million on growth projects, indicating a strong focus on growth and guidance for the future.

Tim Roberts says,

Expected Cost of $300 million to Capture Opportunities

- The company expects to see an expense of $300 million in the coming years to capture the opportunities in the market.

- It is estimated that around one third of the cost will be spent in the near future.

Commercial Side is Driving Growth

- Initial indications suggest that the commercial side of the business is likely to drive growth.

- The company foresees that it will take around two years to fully capture the growth.

Integration of Value Chain

- The company has integrated gas processing and fractionation capacity in key regions.

- Long-haul pipelines coming in and out of DJ and Permian are creating opportunities to place the barrel at the right place for maximum value.

Possible Additional Opportunities

- The company is hoping to find more opportunities as it digs deeper into the integration process.

- They plan to update investors on any new developments in the future.

Q & A sessions,

Expected Earnings and Cash Position

- The company achieved the high end of the range in Q4 2022 earnings

- Expectations to maintain earnings around that level

- Healthy cash position at the end of the year, over $6 billion

- Enhanced balance sheet by $4 billion since pre-pandemic

DCP Roll-Up and Impact on Debt and Dividend

- DCP roll-up expected sometime in Q2

- Transaction valued at $3.8 billion

- Expect to pay off incremental debt and increase dividends

- Flexibility to look at cash returns to shareholders, including potential buybacks

Structure Simplification and Industry Consolidation

- PSXP and DCP will simplify overall ownership structure

- Market evolving with consolidation in the industry

- Opportunities will be assessed, but focus is on successfully integrating DCP

- Expect DCP integration to take until end of 2022 or possibly 2024