Ralph Lauren Corporation

CEO : Mr. Patrice Jean Louis Louvet

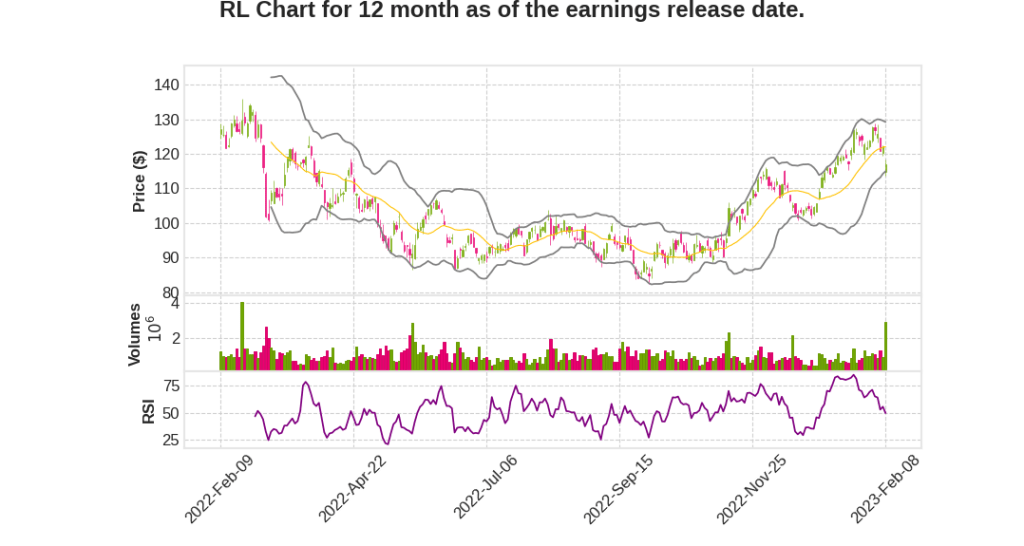

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | -13.0% YoY | -28.9% | -25.6% | 2023-02-09 |

Jane Nielsen says,

Q3 Revenue and Growth

- Q3 revenues up 1% on a reported basis and 7% in constant currency, above outlook.

- Total company revenues increased 7% in constant currency, led by double-digit growth in Asia and Europe.

Digital Sales and Ecosystem

- Ralph Lauren digital ecosystem sales grew high single digits in constant currency and more than 40% on a two-year stack.

- Sales from owned Ralph Lauren digital sites grew 10% on top of more than 30% growth last year.

- Digital margins strongly accretive to overall profitability.

Gross Margin

- Total company adjusted gross margin was 65.2%, down 80 basis points to last year on a reported basis, but up 80 basis points in constant currency.

- AUR up 10% on top of 19% growth last year and lower air freight reliance following last year’s supply chain disruptions.

- Gross margins were below expectations this holiday due to targeted outlet promotions, post-Christmas sale days, and higher duty costs in Europe.

Operating Margin

- Operating margin was at the high end of guidance range.

- Adjusted operating margin was 16% on a reported basis and 17.8% in constant currency representing a 190 basis point increase to last year.

- Adjusted operating expenses declined 1%, including a marketing expense decline of 8% over last year’s disproportionately back half-weighted spend.

Regional Performance

- North America: Third quarter revenues grew 1%, North America retail comps grew 2%, and wholesale declined 2% to last year.

- Europe: Third quarter revenue increased 1% on a reported basis and 13% in constant currency, and Europe wholesale declined 1% on a reported basis but grew 11% in constant currency.

- Asia: Third quarter revenue increased 1% on a reported basis and 16% in constant currency, with balanced growth across digital commerce and brick-and-mortar stores.

Patrice Louvet says,

Revenue Growth and Strategic Priorities

- Delivered better-than-expected performance with positive revenue growth from all three regions.

- Strong progress on the strategic priorities outlined in the Next Great Chapter plan.

- Maintaining flexibility to respond to consumer demand and market dynamics while elevating and energizing the lifestyle brand.

Brand and Product Elevation

- Investing in the brand’s desirability with consumers with global and localized brand activations and diverse range of campaigns.

- Growing market share and AUR with Polo lovers and attracting young full-price customers to the business.

- Added 1.6 million new consumers with over 51 million social media followers globally.

Core and High-Potential Categories

- Core products represent 70% of sales and continued to drive high single-digit growth in the third quarter.

- High-potential categories including women’s, outerwear, and emerging home business increased low teens.

- Women’s represents single largest long-term opportunity for market share gains and category growth as a company.

Winning in Key Cities with Consumer Ecosystem

- Third quarter sales for total Ralph Lauren digital ecosystem and own digital sites grew high single and low double digits globally.

- Opened 55 new stores in concessions focused on top cities globally, majority in Asia, particularly Mainland China.

- Reported third quarter Mainland sales up high single digits in constant currency despite widespread COVID disruptions.

Enablers

- Proud to be recognized on Fast Company’s 2022 Brands That Matter and Fortune’s World’s Most Admired Companies lists.

- Highlighted first cradle-to-cradle certified product with commitment to enable past and future products to live on responsibly.

Q & A sessions,

Resilient Core Consumer and Diverse Growth Strategy

- Core consumer remains resilient and less price-sensitive

- 1.6 million new consumers added, higher-value and younger

- Diverse growth strategy with significant opportunities across regions, including China, North America, and Europe

- Core products did well, with high single-digit growth, and also growth in high-potential categories like women’s and outerwear

Flexibility and Elevation Journey

- Flexibility in product portfolio enables the company to flex up and down based on consumer needs

- Elevation journey has built-in pricing flexibility to react to competitive environment without walking back brand elevation strategy

- 70% increase in AUR since start of elevation phase, with 10% growth this quarter

China Growth Opportunities

- Significant near and long-term growth opportunities in China

- 7% constant currency growth in Q3 despite store closures, reduced hours, and staffing shortages

- Strong brand building, relevant product offering, and connected ecosystem expansion in key markets

- Brand desirability resonating with Chinese consumers, leaving the brand into local fabric of the culture

Strategic Priorities and Progress

- Strong progress on strategic priorities outlined in Next Great Chapter: Accelerate plan

- Multiple levers of growth and broad lifestyle portfolio puts the company in a position of strength to become the world’s leading luxury lifestyle company

- Commitment to brand and product elevation while maintaining flexibility to respond to consumer demand and market dynamics

- Double-digit AUR growth despite more promotional marketplace

Cost Discipline and Operating Margin Targets

- Culture of operating and cost discipline enabled the company to meet operating margin targets in the period

- Pragmatic approach to merchandising, pricing, and inventory planning in choppy global environment