Roper Technologies, Inc.

CEO : Mr. Laurence Neil Hunn

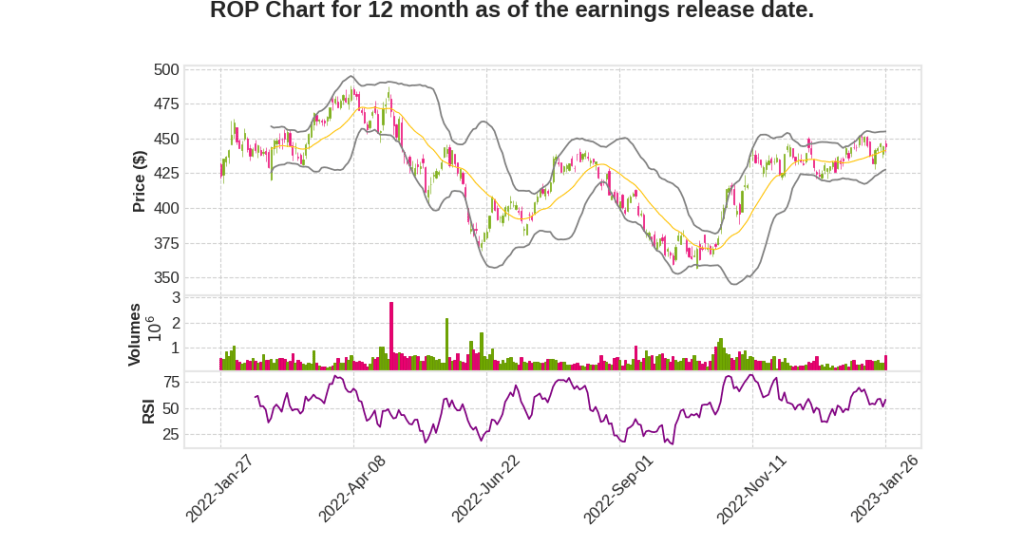

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2022 Q4 | -5.4% YoY | 28.7% | 23.3% | 2023-01-27 |

Jason Conley says,

Q4 2022 Financial Performance

- Revenue of over $1.4 billion, which was 14% higher than the prior year, with organic growth of 7% and acquisitions adding eight points of growth.

- EBITDA of $592 million, up 17% over the prior year with strong operating leverage across the enterprise and improving gross margins in the TEP segment.

- DEPS of $3.92, 17% higher than the prior year and $0.18 above the midpoint of guidance range.

- Free cash flow of $457 million, down 8% over the prior year, with a 3% increase if factoring out the $30 million Vertafore tax benefit in 2021 that doesn’t repeat.

Segment Performance

- Application Software: revenue up 22% to $740 million, with EBITDA margin increased to 45.6% in the quarter due to strong SaaS bookings growth and solid net retention throughout the year.

- Network Software: revenue up 9% to $350 million, with EBITDA up 9% to $189 million or 54% of revenue, led by freight matching business driving higher ARPU.

- Tech-enabled products: revenue of $340 million and grew 5% organically in the quarter, with strong demand and orders that didn’t get delivered towards the end of the quarter which will benefit Q1.

Full Year 2022 Performance

- Revenue of $5.4 billion, 11% higher than prior year with 9% organic growth.

- EBITDA of nearly $2.2 billion, 12% higher than prior year with EBITDA margin of 40.4%.

- EPS of $14.28, 15% higher than prior year, reflecting strong P&L leverage against the 11% revenue growth.

- Free cash flow of approximately $1.5 billion, down 7% versus prior year, but normalized for headwinds, it grew about 8%.

Financial Position

- Net debt-to-EBITDA ratio stands at 2.7 times, with undrawn revolver of $3.5 billion and $4 billion plus of M&A capacity.

- Completed the majority sale of industrial businesses, which yielded net proceeds of over $2.3 billion, and updated the fair value of the equity investment each quarter going forward.

Neil Hunn says,

Roper’s Strategic, Operational, and Financial Progress

- Roper concluded its multiyear divestiture program aimed at improving the quality of the remaining portfolio by emphasizing less cyclical, more asset-light, and higher-growth businesses.

- The company deployed $4.3 billion towards market-leading and application-specific software businesses.

- Roper grew organically just shy of 10% for the year while simultaneously improving the underlying quality of the enterprise.

- The businesses did a terrific job of innovating and capturing share, leading to another solid year of performance in 2023.

Roper’s Incoming CFO

- Jason Conley has been with Roper for 16 years and has recently been appointed as the company’s CFO.

- Conley has been a member of Roper’s capital allocation team and has attended every Board meeting.

- The team is excited to partner with Conley for the next leg of their evolution.

Q & A sessions,

Application Software Segment:

- Revenues for the segment were $2.64 billion, up 7% on an organic basis

- Vertafore, a software business that tech enables P&C insurance agencies, experienced accelerated growth

- Both Aderant and Deltek continued their SaaS migration momentum and grew nicely based on customer adds and strong retention

- PowerPlan crossed a meaningful milestone by launching a SaaS solution for their flagship product, tax fixed assets

- Clinisys and Data Innovations continue to win in the marketplace

- Frontline, a 2022 acquisition, is off to a solid start

Network Software Segment:

- Revenues for the segment were $1.38 billion, up 13% on an organic basis

- U.S. and Canadian freight matching businesses experienced exceptional growth

- iPipeline and iTrade network were stellar performers throughout 2022 and benefited from strong renewal and expansion activity

- Foundry had another great year as the market-leading software in postproduction media entertainment

- Growth in businesses focused on alternate site healthcare was led by SHP and SoftWriters, with high retention rates

Tech-enabled Products Segment:

- Revenues for the segment were $1.35 billion, up 10% on an organic basis

- Neptune, our water meter and technology product business, had a terrific year with strong growth and migration of customers to their newest data management solution

- Northern Digital continued to see terrific demand for their optical and EM solutions

- Verathon turned in another solid year performance, with growth based on momentum across their video innovation and single-use bronchoscope product lines

Organic Growth Outlook for 2023:

- Expected organic growth for the company in 2023 is in the mid-to-high single-digit area based on sustained growth across the group and normalization of market conditions for freight and logistics applications

- Expected organic growth for the Application Software segment is in the mid-single-digit area based on market positions and growth in recurring revenues

Financial Guidance for 2023 and Q1:

- DEPS guidance for 2023 is expected to be in the range of $15.90 and $16.20, with expected organic growth of 5% to 6% and a tax rate in the 21% to 22% area

- DEPS guidance for Q1 is expected to be in the $3.80 to $3.84 range