Arista Networks, Inc.

CEO : Ms. Jayshree V. Ullal

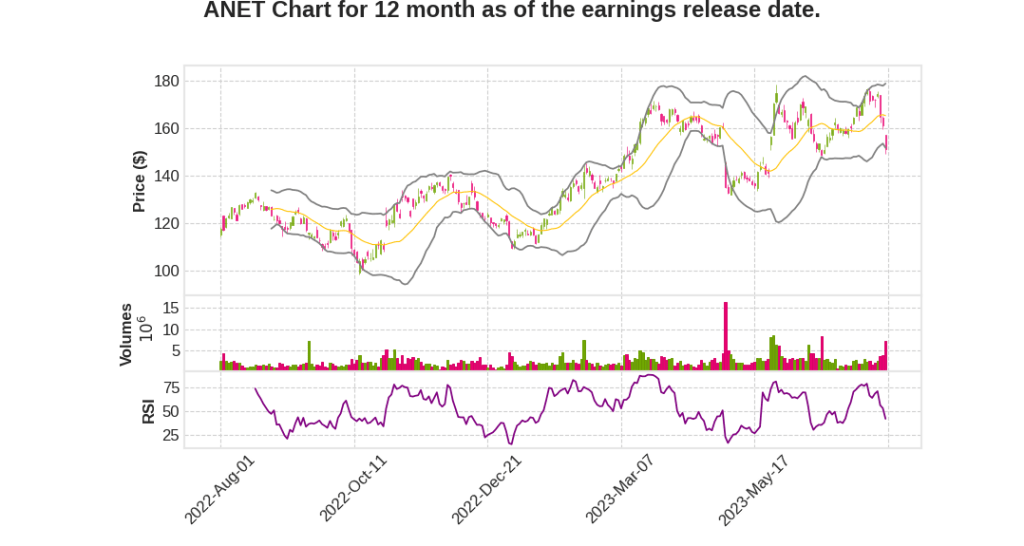

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | 38.7% YoY | 46.1% | 62.2% | 2023-07-31 |

Ita Brennan says,

Total Revenues

- Total revenues in Q2 were $1.46 billion, up 38.7% year-over-year, exceeding the upper end of the guidance range.

- Services and subscription software contributed approximately 15.2% of revenue in the quarter.

- International revenues for the quarter were $304.4 million or 20.9% of total revenue, reflecting growth in enterprise customers in EMEA and APAC.

Gross Margin

- Overall gross margin in Q2 was 61.3%, in line with guidance and up from the previous quarter.

- Incremental improvements in gross margin quarter-over-quarter were driven by higher enterprise shipments and better supply chain costs.

Operating Expenses

- Operating expenses for the quarter were $287.3 million or 19.7% of revenue, reflecting increased R&D spending and sales and marketing expenses.

- R&D spending came in at $188.5 million or 12.9% of revenue, primarily due to increased headcounts and higher new product introduction costs.

Net Income and Earnings Per Share

- Operating income for the quarter was $606.5 million or 41.6% of revenue.

- Net income for the quarter was $501.2 million or 34.4% of revenue.

- Diluted earnings per share for the quarter were $1.58, up 46% from the prior year.

Balance Sheet and Cash Flow

- Cash, cash equivalents, and investments ended the quarter at approximately $3.7 billion.

- Repurchased $30 million of common stock in the quarter, leaving $145 million available for future repurchases.

- Generated approximately $434.1 million of cash from operations in the period, reflecting strong earnings performance.

Outlook for Q3 and Beyond

- Expect year-over-year growth in excess of 30% for 2023.

- Continue to see progress in gross margin through the end of the year.

- Focus on targeted hires and R&D investments.

- Expect continued growth in inventory through the end of the year.

- Guidance for Q3: Revenues of approximately $1.45 billion to $1.50 billion, gross margin of approximately 62%, and operating margin at approximately 41%.

Jayshree Ullal says,

Revenue and Earnings

- Revenues for Q2 2023 were $1.46 billion.

- Non-GAAP earnings per share were $1.58.

Gross Margins

- Non-GAAP gross margins were 61.3%.

- Gross margins are expected to consistently improve every quarter this year and stabilize in 2024.

International and Americas Contribution

- International contribution accounted for 21% of revenue, while the Americas contributed 79%.

Cloud Networking Port Growth

- Arista has surpassed 75 million cumulative cloud networking ports.

- Experiencing three refresh cycles with customers: 100 gigabit migration in enterprises, 200 and 400 gigabit migration in the cloud, and 400 to 800 gigabit for AI workloads.

Cloud Titan Demand and AI Investments

- One specific cloud titan customer has signaled a slowdown in CapEx from previously elevated levels.

- Near-term cloud titan demand is expected to moderate, with spend favoring AI investments.

- Arista projects growth in excess of 30% annually versus the prior Analyst Day forecast of 25% in 2023.

- Arista is doubling down on investments in AI and adapting to changes in cloud and AI networking plans of their largest cloud customers.

Q & A sessions,

Impact of Arista’s participation in the back end of the network

- Arista’s entry into the back end of the network will have a significant impact on its participation in AI networks.

- There are three classes of networks in the back end – very small networks within a server, medium clusters for generative AI and inference, and extremely large clusters for language training models.

- Ethernet is expected to shine in the extremely large clusters, especially with the advent of ChatGPT-3 and ChatGPT-4, due to its scalability.

- Currently, InfiniBand is the only technology available for customers in the large clusters, but Ethernet is the right long-term technology for AI networks.

Change in Arista’s business diversification

- Arista has become a more diversified company compared to three years ago.

- Arista has doubled down on its cloud titans and is gaining market share in the enterprise.

- Arista has strengthened its presence in Tier 2 providers and the broader enterprise, offering AI opportunities in areas like campus, routing, and classical data centers.

- The total addressable market (TAM) has increased from $30 billion to well north of $50 billion in the past three years.

Reasons for Arista’s success in the enterprise

- Arista is chosen in the enterprise due to its high-quality, supportive, and friendly software experience.

- Arista’s common leaf spine architecture and modern cloud operating model appeal to customers seeking architectural shift.

- Arista’s hybrid strategy for shifting workloads between the cloud and on-premise is favored by customers, especially for mission-critical applications.

- Arista’s expansion into campus and routing, zero-trust security, and observability further contribute to its success in the enterprise.

Planning for AI in 2023

- 2023 is a year of planning for AI, as many GPUs are being purchased.

- The focus is on large-scale networks with over 200 or 1,000 GPUs.

- Planning involves considering the application, cluster size, time, language model datasets, and network foundation.

- In some cases, existing technologies like InfiniBand are bundled with GPUs for quick implementation, but for long-term deployments, pilots and trials with Arista’s solutions are expected in 2024.

- In 2025, a significant increase in GPU deployments is anticipated, with 4,000 to 8,000 GPUs projected for 2024.