Caesars Entertainment, Inc.

CEO : Mr. Thomas Robert Reeg CFA

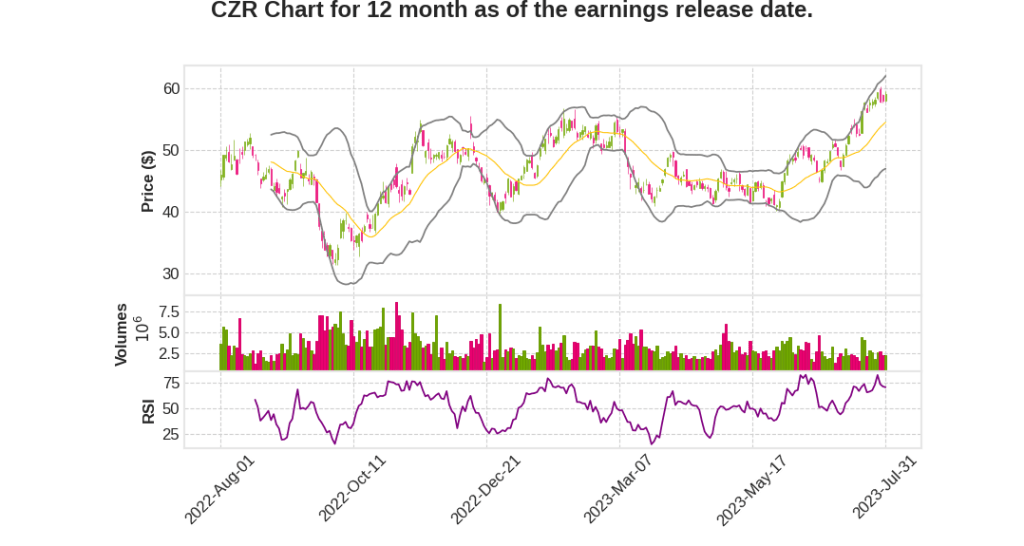

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | 2.1% YoY | 1.2% | 2411.8% | 2023-08-01 |

Tom Reeg says,

Las Vegas Performance

- Q2 was a strong quarter for Caesars in Las Vegas, despite missing a large group that usually comes every three years, impacting June hold and margins.

- Volumes came through the property, but hold impact in June affected margins.

- Group business is accretive to overall Vegas margin.

- Forward-looking, Vegas continues to look strong, with strong July performance and anticipation of Formula One and the Super Bowl in 2023.

Regional Portfolio

- There is competitive pressure in certain regional markets such as Tunica, Council Bluffs, and Chicago due to new casino openings.

- However, the fruits of the capital investment cycle, including new properties in Danville, Indianapolis, Lake Charles, and Atlantic City, have offset the competitive pressures.

- Regional EBITDA was flat year-over-year despite the strong comparison to last year.

Digital Business

- Caesars achieved its first full quarter of positive EBITDA in the digital vertical.

- The acquisition of William Hill has significantly improved Caesars’ digital capabilities and product offerings.

- Caesars expects to build market share in the iCasino space and leverage its Caesars Rewards program to drive growth.

- The launch of the Liberty app in Nevada is a significant milestone, providing a competitive edge and customer acquisition opportunity.

Financial Outlook

- Caesars continues to pay down debt and expects conventional leverage to decrease.

- The company is considering options for the free cash flow generated in 2024 and 2025, including potential return of capital or external opportunities.

- Caesars feels confident and well-positioned for future growth, with a strong cash flow machine, improving results, and reduced interest expenses.

Eric Hession says,

Improved Performance in Digital Segment

- Adjusted EBITDA of $11 million and net revenue of $216 million in Q2 2023.

- Significant improvement compared to a $69 million EBITDA loss in the same period last year.

Growth in Sports Betting and iCasino

- Sports betting hold improved by 180 basis points compared to last year.

- iCasino volume increased by 27% year-over-year.

New Technology Improvements

- Launch of the new iCasino product, Caesars Palace online, in multiple states.

- Transition to flagship Liberty product for the Caesars app in Nevada, with plans to convert William Hill product and retail sportsbooks later this year.

- Rolling out of a new native iOS Sportsbook app, with 100% adoption expected by August.

- Introducing an in-house player account management system, starting state by state later this year.

Expansion and Market Reach

- Offering sports betting in 30 North American jurisdictions, with 22 of them offering mobile wagering.

- Operating iCasino products in six jurisdictions.

Q & A sessions,

Reinvestment Levels

- Reinvestment levels as a percentage of volume were around 1%.

- Reinvestment as a percentage of gaming revenues was around 22%.

- Reinvestment for existing customers tends to be below the overall percentage.

- Reinvestment may range between 1% and 1.25% going forward.

iCasino Products

- Excitement about the iCasino products and the ability to grow market share.

- Competitive product in the market that can be used to attract existing database customers.

- Improved customer experience without needing to go through the sports betting app to access the casino.

- New system allows for segmented marketing and increased reinvestment on the casino side.

Standalone Caesars Palace App

- Higher percentage of slot business compared to table games.

- Standalone app will include live dealer and branded/customized games.

- Third-party partnerships for branded/customized games instead of in-house development.

Capital Allocation and Future Opportunities

- Expectation of generating significant free cash flow as capital projects wind down.

- Consideration of external opportunities for future growth.

- Confidence in the growth potential of the existing portfolio.

- Exploration of distributing cash flow or putting it to work elsewhere.

Growth Potential in Regional Portfolio

- Continued growth opportunities in regional properties, with examples of 2x and 3x improvements in EBITDA.

- Projects in progress and future investments to drive growth.

- Investment decisions based on the specific market and property circumstances.