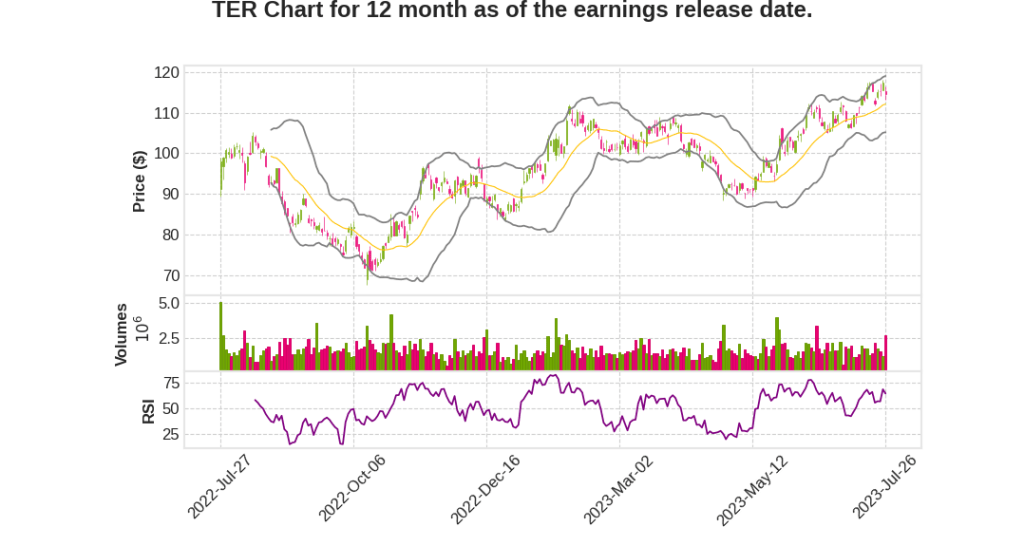

Teradyne, Inc.

CEO : Mr. Gregory S. Smith

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | -18.6% YoY | -43.6% | -37.1% | 2023-07-27 |

Greg Smith says,

Q2 Sales and Earnings

- Second quarter sales were at the top of the guidance range as supply constraints eased.

- Earnings were above guidance due to higher gross margins.

Semiconductor Tester Segment

- Semiconductor tester segment has been in a correction cycle driven by excess inventory, particularly in the mobility part of the market.

- Automotive demand remains strong in semiconductor test.

- Growth in DDR5 and HBM devices for data center applications are driving retooling in memory test.

Wireless and System Test Businesses

- Demand remains muted and unchanged in wireless and system test businesses.

- New standards like Wi-Fi 6 and 7 require new or upgraded test equipment in wireless test.

- Increased device complexity is leading to broader adoption of system-level test (SLT).

- Defense and aerospace sectors have a solid pipeline, providing a foundation for growth in system test.

Robotics Segment

- Robotics demand has softened due to challenging economic conditions, particularly low PMIs in Europe and the US.

- Transformation of the UR distribution channel has had a short-term impact on pipeline conversion.

- Shift to complementing existing distribution channel with direct touch coverage and adding OEM partners is slowing sales from distributors, but expected to yield long-term benefits.

- New product shipments include UR20 for welding and metal fabrication, and MiR insights for fleet monitoring and optimization.

Outlook for 2023

- Estimate of the 2023 SOC test market to be $3.7 billion to $4.1 billion, down 13% to 21% from 2022, but up from previous outlook in April.

- Expect HBM DRAM segment to drive incrementally stronger test demand for Magnum products in the second half of 2023.

- Overall memory test market expected to be at the low end of $900 million to $1 billion range described in April.

- Confident about the future of the semiconductor test market due to increasing device complexity and growth in automotive market.

- Expect VIP portion of the compute segment to grow faster than the overall compute segment, with Teradyne’s share higher than in traditional compute customers.

- Full year revenue for robotics group projected to be flat to down 10% from last year.

Greg Smith says,

Underperformance and projected loss

- The group has consistently underperformed profit targets.

- This is the first year where a loss is projected for the group.

Misunderstanding of market size and early adopters

- There was a misunderstanding of how large the potential end market is.

- Early years of the business were driven by sophisticated early adopters.

- As the company moved into a larger market, customers were more focused on buying solutions instead of being robot enthusiasts.

Skills gap and solution providers

- Customers in the larger market lacked the skills needed to put the robots into operation.

- The company is shifting emphasis towards solution providers like OEMs.

- This shift will allow the company to provide solutions that cater to the capabilities of its customers.

- Directly connecting with larger customers who can maintain and implement the robots is a part of the transformation strategy.

Go-to-market and product market fit challenge

- The main challenge in robotics is not technology but go-to-market and product market fit.

- Evidence shows that the company’s products do deliver value.

- The focus is on finding the best way to get the products into the hands of customers for easy adoption.

Q & A sessions,

Competitive Environment

- The UR is a clear leader in its space with more than 3x the market share of the nearest competitor.

- Shares in the mid-30s worldwide, but over 50% worldwide if you exclude China.

- Lost a few points of share to Chinese pure play cobot companies, mostly in China.

- Struggling to gain share in China due to serving the market at unprofitable prices.

AMR Market

- Total AMR market is about $2 billion per year.

- UR’s share is around 3%, with many other companies in the 1% to 6% range.

- Working on establishing strategic relationships with global customers to adopt large fleets.

- Believes competition is fragmented and can outperform.

Improvement and Profitability

- Expects significant improvement in Q4 2023 results due to the release of UR20 and 12 months of direct account coverage in large accounts.

- Target for the group is 5% to 15% profit, aiming to return to that range in 2023.

- Expect profitability to increase a couple of points by the end of the midterm (2022-2026).

- If business is growing 20% to 30% per year, aiming for 10% to 20% profit range.

- Planning for the group to operate at a rule of 40.

Sustainability and Automotive Demand

- Increasing attach rate of semiconductors in cars, driven by the growth of electric vehicles (EVs).

- Dollar value of semiconductors in each car shift is increasing at about a 12% rate.

- Automotive demand may cycle, but the strong underlying driver of increasing attach rate sustains.

- Industrial sector shows strength in clean energy and manufacturing infrastructure for EVs and batteries.

Macroeconomic Headwinds and Growth

- UR’s order rates are down roughly 10% year-on-year, compared to industrial robotics peers down 20% or greater.

- Facing broad economic headwinds, but as a disruptor, expect significantly higher growth than main players.

- Current distribution is vulnerable to macroeconomic cycles, but moving towards a distribution setup for consistent results.

- Build out of OEM and large account coverage will provide better immunity in future headwinds.