Trimble Inc.

CEO : Mr. Robert G. Painter

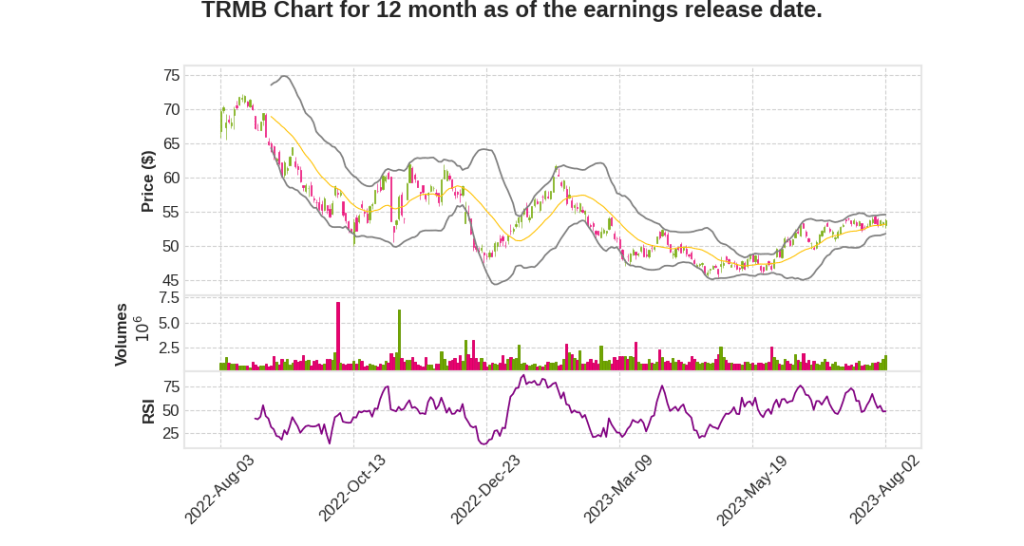

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | 5.6% YoY | -61.4% | -73.1% | 2023-08-03 |

David Barnes says,

Revenue Performance

- Second quarter revenue of $994 million grew three percent organically

- Revenue was above expectations, driven by earlier-than-expected shipment of a large Geospatial equipment order to the Federal Government

- Excluding the federal order, revenues were in-line with projections

- Total company revenue growth versus prior year was driven by recurring software

- Gross margins were strong with non-GAAP gross margins of 64.2%, tying record levels from the first quarter

- EBITDA margin of 25.3% in the second quarter was up 110 basis points year-over-year

- Operating and EBITDA margins continue to grow even as the company invests in digital transformation

Segment Performance

- Buildings and Infrastructure software portfolio had organic ARR growth of over 20%

- Bookings of recurring software offerings in the segment grew at a mid-20s percentage rate

- Geospatial segment experienced organic revenue growth driven by a $18 million shipment to the federal government

- Resources and Utilities segment revenues were down year-on-year, driven by agriculture business

- Transportation segment delivered 6% organic revenue growth, driven by North American Enterprise and Maps businesses

Guidance and Outlook

- Full year revenue guidance range is $3.845 billion to $3.925 billion, representing mid- to high single digit organic revenue growth in the second half of the year

- Expectation for gross and operating margins has increased by 50 basis points

- Full year EPS guidance range is $2.57 to $2.73

- Third quarter organic revenue growth expected in the range of 0% to 5%, with gross margins lower than the second quarter

- EPS projected in the range of $0.56 to $0.64

- Geospatial revenues expected to be down organically at a mid-to-high single-digit rate in the third quarter

- Resources and Utilities revenue expected to be down at a mid-single-digit organically

- Buildings and Infrastructure and Transportation revenues expected to continue growing organically in the third quarter

Rob Painter says,

Annualized Recurring Revenue (ARR)

- Trimble achieved 14% organic growth in the quarter, beating internal expectations by 100 basis points.

- Record ARR of $1.88 billion, compared to $1.2 billion in 2020.

- On track to achieve $2 billion of ARR by the end of the year.

Financial Performance

- EBITDA margin of 25.3%, slightly ahead of expectations.

- Gross margin of 64.2%, compared to 56.8% in 2015 and 58% in 2018.

- EPS at $0.64.

- Year-to-date free cash flow conversion rate to net income of nearly 100%.

Segment Performance – Buildings & Infrastructure

- ACV bookings accelerated, achieving a record level of bookings in the quarter.

- ARR grew over 20%.

- Trimble Construction One offering achieving higher win rates, larger deal sizes, and shorter sales cycles.

- Pivoting hardware offerings to adopt aspects of the subscription business model.

Segment Performance – Geospatial

- Revenue well ahead of internal expectations.

- Strong demand from US state departments of transportation.

- Saw ARR growth in the Trimble Catalyst product line, with over 10,000 cumulative units shipped.

- Expanded product line in the reality capture space with the launch of the X9 scanner.

Segment Performance – Resources and Utilities

- Farmer sentiment trending negative, but market fundamentals healthy.

- Strategic focus on building out aftermarket channel in agriculture.

- Positioning Services business winning customers in both on-road and off-road capacities.

- Launched cloud-based log inventory and management system in Forestry to expand addressable market.

Segment Performance – Transportation

- Soft freight market pressuring carriers to streamline operations.

- Increased operating income margin for six consecutive quarters.

- Grew organic ARR for the seventh consecutive quarter.

- Early indications of spot market bottoming out in Transporeon business in Europe.

AI and Technology

- Deploying artificial intelligence across Trimble for internal and customer-facing applications.

- A trial program showed upwards of 25% improvement in productivity using AI-assisted programming.

- Applying AI to sales process to coach sales reps and identify cross-sell opportunities.

- Using AI for improved positioning accuracy in harsh environments and video intelligence solutions in transportation and agriculture.

- Automating invoices by converting PDF data into usable accounts payable data.

Q & A sessions,

Company Culture and Talent

- Trimble won a number of culture awards, highlighting its ability to attract top talent in the industry.

- Trimble Labs sponsors 30 technology labs in 14 countries, demonstrating the company’s commitment to developing future talent.

Renewable Energy and Community

- Trimble announced the groundbreaking of a 1.7 megawatt solar array at its headquarters, showcasing its commitment to renewable energy.

- Trimble’s technology is being used to increase the productivity and quality of the solar installation.

Leadership Change

- Steve Berglund retired from Trimble’s Board of Directors after 24 years of service, and Borje Ekholm will now chair the Board of Directors.

Market Leadership and Opportunities

- Trimble is a market leader in providing high-accuracy positioning solutions in various industries such as agriculture, civil construction, and surveying.

- The on-road space, particularly in the automotive industry, is an emerging market that presents an expanded addressable market for Trimble.

- The on-road business is estimated to be a potential $1 billion market opportunity.

Productivity and Revenue Growth

- Trimble aims to improve internal productivity through initiatives like the copilot trial, which showed productivity benefits in R&D.

- Improved internal effectiveness and efficiency can lead to operational leverage and increased revenue growth in the future.

- Monetization of customer-facing solutions is expected through making Trimble’s solutions better and offering unique capabilities when buying a bundle or platform offering.

- Standalone analytics may not be able to monetize independently.

Market Trends and Outlook

- Infrastructure is a strong segment for Trimble, both in North America and globally.

- Pockets of strength are seen in non-residential sectors such as renewable energy projects, onshoring of manufacturing, and data centers.

- Residential construction has been mixed, with new homebuilding happening but challenges in Europe.

- The macroeconomic sentiment, changes in distribution networks, and lapping strong shipment numbers impacted the aftermarket business in the quarter.

- The long-term outlook for the aftermarket business remains positive.

Digital Transformation

- Trimble completed the next phase of its digital transformation, putting its North American construction enterprise software businesses on a common digital platform.

- This milestone enables cross-selling and enhances visibility into the pipeline and customer business across the Trimble portfolio.

- Further enhancements to the digital platform will continue to roll out in the coming quarters.