Warner Bros. Discovery, Inc.

CEO : Mr. David M. Zaslav

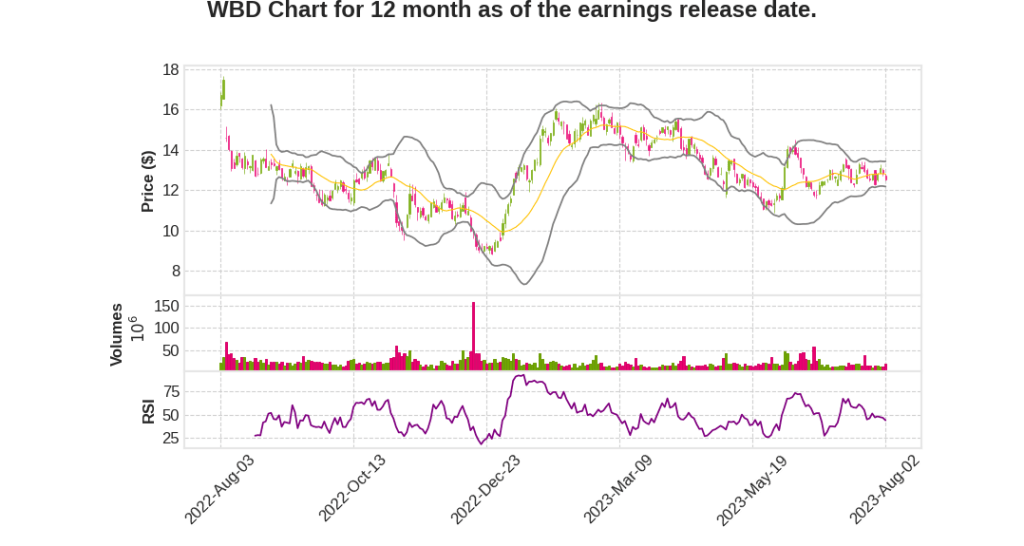

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2023 Q2 | 5.4% YoY | -65.9% | -65.8% | 2023-08-03 |

Gunnar Wiedenfels says,

Adjusted EBITDA Growth and Synergies

- Adjusted EBITDA grew 23% in Q2, marking the second consecutive quarter of meaningful year-over-year growth.

- Year-to-date, adjusted EBITDA is up more than $600 million.

- The company has accelerated the delivery of transformation initiatives and has already delivered more than $2 billion in incremental cost synergies this year.

- Expects to achieve $4 billion in total synergies sooner than previously thought and sees a clear path to achieving $5 billion or more through 2024 and beyond.

Cash Flow Focus and Debt Repayment

- Second-quarter free cash flow was over $1.7 billion, ahead of expectations.

- Repaid over $1.6 billion of debt, reducing net leverage significantly to 4.6x.

- Remains focused on debt pay down and expects to achieve target leverage of 2.5x growth by the end of 2024.

D2C Segment

- The D2C segment effectively broke even in terms of EBITDA and exceeded expectations.

- Growth seen across all revenue streams, with content being the standout.

- Saw a net subscriber loss of $1.8 million in Q2, impacted by overlapping subscriber bases and expected churn from the end of key series.

- Optimistic about the strategy of offering both Max and discovery+ to customers.

- Streaming advertising opportunity is gaining traction, supported by gains in ad-light subscribers, HBO and Max Originals, and increased engagement.

Studios Segment

- The Studios segment has been inconsistent.

- Overall content revenues declined 25% due to slate, timing of production, and fewer series orders.

- Barbie has been successful at the box office, approaching $1 billion in global revenue.

- Release dates and performance expectations for remaining films and television productions are uncertain due to ongoing strikes.

Networks Segment

- Advertising decreased 13%, impacted by tough comparisons and the absence of certain sporting events.

- Expect continued modest sequential improvement in advertising revenues through the end of the year.

- Distribution revenues decreased 1%, with a modest improvement compared to last quarter.

- AT&T Sports Nets expected to be sold or wound down by the end of the year, with a modest impact on Q3 and more significant impact in Q4 and 2024.

Guidance and Outlook

- Expects to generate free cash flow in the $1.7 billion range for Q3, with full-year free cash flow in the range of $4.5 billion to $5 billion.

- Expects adjusted EBITDA to settle towards the low end of the target range of $11 billion to $11.5 billion.

- Puts and takes for adjusted EBITDA include the timing and magnitude of potential ad market recovery, D2C profit growth, and uncertainties in the studio segment due to strikes.

David Zaslav says,

Free Cash Flow and Deleveraging

- Generated over $1.7 billion in free cash flow in Q2

- Anticipating about the same amount in Q3

- Paid down $1.6 billion in debt in Q2 and a total of $9 billion since the merger

- Expect to be comfortably below 4x levered by the end of the year

- Firmly within the investment-grade rating by midpoint next year

- Targeting 2.5 to 3x gross leverage by the close of 2024

Direct-to-Consumer Strategy

- Tracking ahead of financial projections in the direct-to-consumer business

- Global direct-to-consumer business was breakeven in Q2 and modestly EBITDA positive for the first half of the year

- U.S. direct-to-consumer business expected to be profitable for the year 2023, a year ahead of prior guidance

- Migration to Max platform has gone well with majority of subscribers successfully transferred

- Seeing early signs of stronger engagement and exploration of new genres

- Preparing to launch Max in markets globally

Gaming Business

- Warner Bros. Discovery is scaled in gaming among its peers

- Mortal Combat 1 and Hogwarts Legacy are highly anticipated titles

- Investing in gaming business to be more strategic and leveraging underutilized storytelling IP

- Positioning gaming business as a significant piece of IP and consumer engagement puzzle

Content and Production Business

- One of the largest makers and sellers of content in the world

- 181 Emmy nominations, including 127 for HBO and Max

- Expecting growth in production business as content is windowed globally

- Taking steps to improve performance of Warner Bros. Pictures Group and DC

- Planning to lean into underutilized storytelling IP and tentpole films

Sports Rights and Streaming

- Leader in sports with rights from top leagues in the U.S.

- Significant digital rights in the U.S. with plans to deploy them in the future

- Opportunity to leverage sports in streaming space for incremental growth

- Successful venture with BT in the U.K., merging BT Sport with Eurosport U.K.

Q & A sessions,

Sports Rights and Digital Platforms

- The company has good deals with sports rights domestically and globally, providing real value.

- They own the digital rights to their sports content, allowing them to put it on their platforms at no incremental cost.

- They have been expanding their digital sports offerings in Europe, both as an incremental tier and on the entire platform.

- The early results are promising, with more than 20% of viewership going to diverse content in different time periods.

Content Supersizing and Marketing

- The company is focusing on running their businesses as one company and leveraging their diverse assets to promote each other.

- They have been supersizing their content releases, such as House of the Dragon and The Last of Us, across all platforms globally.

- They are using their existing marketing platforms and assets to promote their content, rather than spending additional money on marketing.

- This unique approach is building the company’s muscle memory and confidence in the effectiveness of their assets.

Market Recovery and Advertising

- The market has shown some improvement, particularly outside the U.S., but the expected meaningful recovery in the second half of the year has not materialized.

- The upfronts were encouraging, with mid-single-digit price increases for sports and affinity networks.

- The company’s Max platform has been performing exceptionally well, with strong pricing and a significant demand.

- Viewership on their platforms remains strong, particularly for older content, which is now being monetized through the Max ad tier.

Transformation Initiatives and Cash Flow

- The company’s transformation initiatives have led to significant improvements in cash flow across the entire P&L.

- They have achieved $2 billion of incremental value capture so far, with a goal of reaching $5 billion or more.

- There is still more to come from ongoing systems transformation and pipeline savings.

- The company has shifted its mindset towards cash generation, focusing on reducing uncollected receivables and improving overall cash flow discipline.

Future Outlook and Opportunities

- There are multiple opportunities for further working capital improvements, as the company is still in the early stages of implementing new systems.

- Cost to achieve will come down over time, as well as interest and CapEx expenses.

- They are changing the way they operate and generate cash, aiming for a 60% cash conversion rate in the long term.

- The company sees enormous opportunity for continued growth and cash flow improvement beyond 2023.