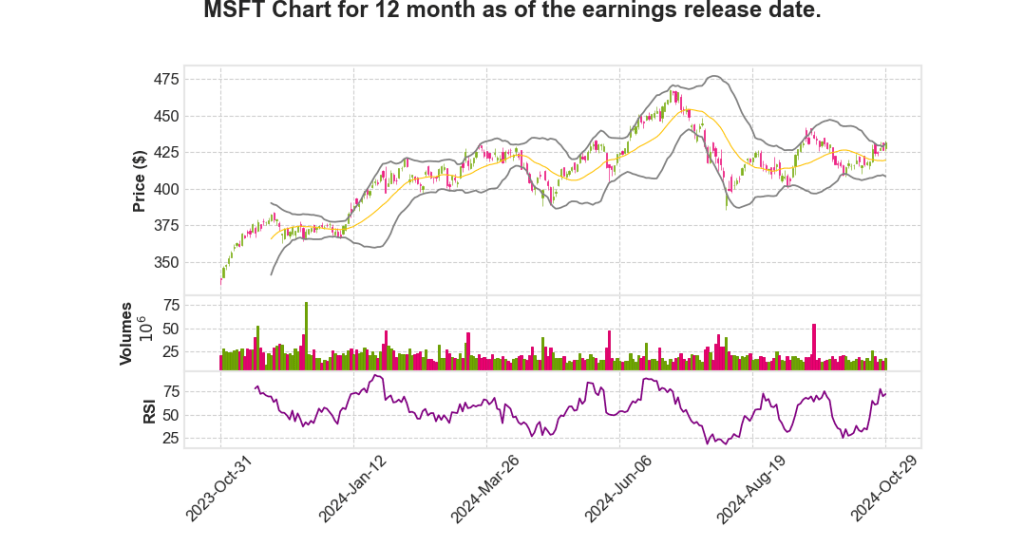

Microsoft Corporation

CEO : Mr. Satya Nadella

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2025 Q1 | 16.0% YoY | 13.6% | 10.7% | 2024-10-30 |

Amy Hood says,

Financial Performance Overview

- Quarterly revenue reached $65.6 billion, marking a 16% increase, and earnings per share rose by 10% to $3.30.

- Microsoft Cloud revenue grew 22% to $38.9 billion, aligning with company expectations.

- Gross margin percentage decreased 2 points to 69% year-over-year, influenced by scaling AI infrastructure.

- Operating income grew 14%, although operating margins decreased by 1 point to 47% year-over-year.

Key Business Segment Performance

- Productivity and Business Processes revenue was $28.3 billion, increasing by 12%.

- Intelligent Cloud revenue rose 20% to $24.1 billion, with Azure and other cloud services showing a 33% growth.

- More Personal Computing revenue increased by 17% to $13.2 billion, driven notably by a 43% growth in gaming revenue.

Impact of Activision Acquisition

- Activision contributed a net 3-point impact to revenue growth, with a 2-point deduction on operating income growth.

- Earnings per share saw a negative $0.05 impact due to transaction-related costs.

- Segment operating expenses increased by 49%, significantly influenced by the acquisition, leading to a 4% decrease in operating income.

Q2 Outlook and Future Projections

- Q2 revenue in the Intelligent Cloud is projected to be between $25.55 billion and $25.85 billion, a growth of 18% to 20% in constant currency.

- Expected growth in Azure Q2 revenue by 31% to 32% in constant currency.

- More Personal Computing revenue is forecasted to be between $13.85 billion and $14.25 billion, noting declines in OEM and devices.

- Operating expenses are expected to grow about 7% in constant currency, resulting in operating margin expansion.

Long-term Strategic Investments and AI Growth

- The AI business is projected to surpass a $10 billion annual revenue run rate by Q2, showcasing rapid growth only 2.5 years since inception.

- Continued investment in cloud and AI infrastructure to accommodate increasing demand.

- Strategic focus remains on maintaining leadership in the AI platform space while ensuring cost management across teams.

Satya Nadella says,

Microsoft Cloud and AI Business Growth

- Microsoft Cloud revenue reached $38.9 billion, marking a 22% increase.

- The AI business is projected to surpass a $10 billion annual revenue run rate next quarter, becoming the fastest business in company history to achieve this milestone.

- Azure Arc reported over 39,000 customers, representing an 80% year-over-year growth.

- New cloud and AI infrastructure investments announced for Brazil, Italy, Mexico, and Sweden, indicating a strategic geographic expansion.

Infrastructure and AI Advancements

- Introduction of new Cobalt 100 VMs offering up to 50% better price performance than previous generations.

- Microsoft is the first to implement NVIDIA’s Blackwell system with GB200-powered AI servers.

- Azure OpenAI usage more than doubled in six months, with prominent users like GE Aerospace conducting over 500,000 internal queries.

Developer Tools and Microsoft 365 Innovations

- GitHub Copilot enterprise customers grew by 55% quarter-over-quarter.

- Microsoft 365 Copilot adoption doubled quarter-over-quarter, highlighting substantial growth in user engagement.

- Vodafone and UBS deploying Microsoft 365 Copilot to significant employee bases (68,000 for Vodafone).

Dynamics 365 and Industry-specific Solutions

- Copilot active users in CRM and ERP increased over 60% quarter-over-quarter.

- Introduction of 10 out-of-the-box autonomous agents to Dynamics 365 for enhanced customer engagement.

- DAX Copilot documenting over 1.3 million physician-patient encounters monthly, exhibiting faster revenue growth than GitHub Copilot did in its first year.

Consumer Businesses and Gaming

- LinkedIn’s member growth in India and Brazil is accelerating at a double-digit rate.

- Gaming division set new records for monthly active users and Game Pass revenue, with the launch of Black Ops 6 being the biggest Call of Duty release ever.

- Unit sales on PlayStation and Steam rose over 60% year-over-year, indicating strong cross-platform performance.

| Business Segment | Key Metric | Growth/Impact |

|---|---|---|

| Cloud Revenue | $38.9 billion | 22% growth |

| AI Business | Projected $10 billion annual run rate | Fastest to reach milestone |

| GitHub Copilot | 55% customer growth | Quarter-over-quarter |

| Microsoft 365 Copilot | Double user adoption | Quarter-over-quarter |

This report underscores Microsoft’s strategic advancements in AI and cloud infrastructure, alongside significant growth in developer tools and consumer engagement, fostering a highly favorable outlook for the company’s stock movement.

Q & A sessions,

Capital Outlay and Inference Demand

- Investment in training is closely tied to the demand and monetization of inference capabilities.

- There is a need to refresh the technology fleet in alignment with Moore’s Law every year, impacting depreciation schedules and financial forecasting.

- Inference demand will dictate the amount of capital to be invested in training moving forward.

External Constraints and Infrastructure Development

- The company faces short-term constraints related to data centers (DCs) and power availability due to rapid demand increases.

- Expectations are set for supply-demand equilibrium improvements in the second half of the fiscal year, leveraging long-term infrastructure investments.

Partnership and Innovation with OpenAI

- The partnership with OpenAI has led to mutual successes, including infrastructure innovations and product development like GitHub Copilot.

- Microsoft has focused on high-quality revenue from enterprise demands rather than selling raw GPUs, emphasizing the quality of revenue streams.

Revenue Growth and Financial Performance

- The company’s new suite in M365, notably commercial Copilot products, experienced the fastest growth in history towards $10 billion in revenue.

- Significant revenue growth in segments like search, news, and ads, surpassing market expectations.

- AI investments are leveraged across various Microsoft business units, providing synergy benefits.

Future Outlook and Financial Guidance

- Q1 showed a 34% increase in constant currency, slightly above the guided 33%, due to revenue recognition benefits.

- Supply constraints are expected to ease, with AI supply-demand alignment anticipated to improve in the second half of the year.

- Microsoft’s $13 billion investment in OpenAI entails absorbing a percentage of the losses under equity method accounting, influencing financial entries.

| Item | Guidance/Performance |

|---|---|

| Q1 Revenue Growth | 34% in constant currency |

| Expected Deceleration | 1-2 points due to supply pushouts |

| OpenAI Investment | $13 billion |