NetApp, Inc.

CEO : Mr. George Kurian

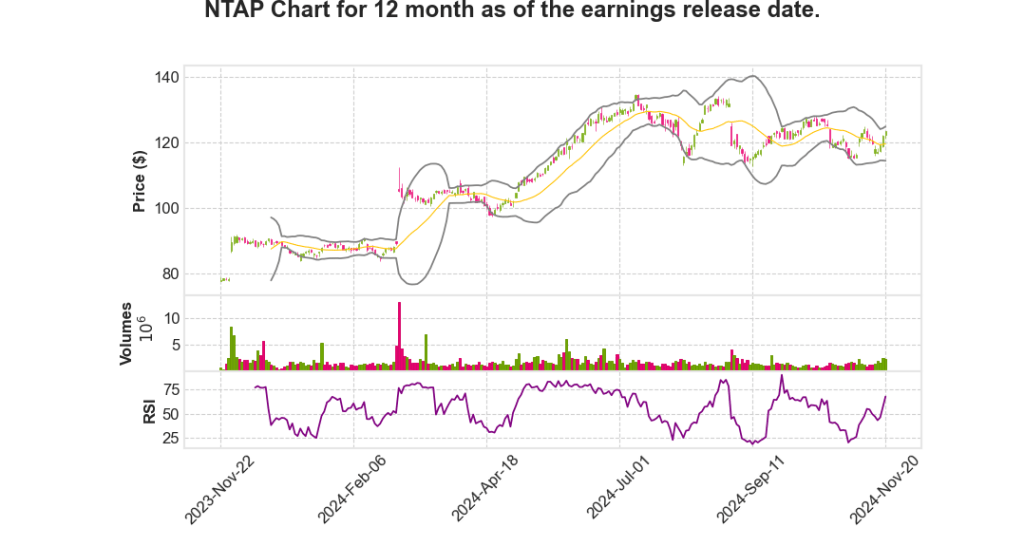

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2025 Q2 | 6.1% YoY | 13.5% | -208.0% | 2024-11-21 |

George Kurian says,

Q2 2025 Financial Performance Highlights

- Achieved record Q2 operating margin and EPS, surpassing expectations due to strong performance in all-flash storage and cloud services.

- Revenue growth was driven by a 19% year-over-year increase in all-flash storage.

- Hybrid Cloud segment revenue increased by 6%, with product revenue growing 9% due to all-flash storage strength.

Strategic Initiatives and Product Innovations

- Launched new products in ASA block-optimized all-flash and FAS hybrid flash array families, enhancing portfolio breadth and capability.

- Keystone Storage-as-a-Service offering recorded a 55% revenue growth year-over-year, integrating Cloud Insights for a holistic infrastructure view.

- Public Cloud segment revenue grew by 9% year-over-year to $168 million, with a 43% increase in cloud storage services.

AI and Data-driven Strategy

- NetApp’s AI business outperformed expectations with over 100 wins across various industries, indicating strong market momentum.

- Expanded AI partner ecosystem with partnerships including Domino Data Labs, NVIDIA, and Lenovo.

- Strengthened collaboration with Google Cloud to provide foundational data storage for Google Distributed Cloud, broadening AI-ready solutions.

Market Position and Recognition

- Maintained leadership position in the all-flash market with a 19% year-over-year increase in annualized revenue run rate, reaching $3.8 billion.

- Recognized as a leader in the 2024 Gartner Magic Quadrant for Primary Storage Platform for the 12th consecutive year.

- Broadened all-flash storage portfolio with high-performance and capacity flash options, enhancing market competitiveness.

Future Outlook and Strategic Focus

- Focused on innovation to meet evolving needs, emphasizing simplicity, capability, and affordability in storage solutions.

- Continuing robust execution and disciplined operational management to sustain earnings growth.

- Confident in delivering strong results for customers and shareholders, driven by strategic focus areas and market leadership.

Mike Berry says,

Financial Performance Overview

- Q2 revenue reached $1.66 billion, marking a 6% year-over-year increase, and aligning with the high-end of the guidance range.

- Billings increased by 9% year-over-year to $1.59 billion, marking the fourth consecutive quarter of growth.

- Q2 operating margin was 29%, which exceeded expectations.

- EPS for Q2 was $1.87, surpassing the high end of guidance due to higher revenues and gross margins.

- Free cash flow was $60 million, a decrease from $97 million in the previous year, mainly due to strategic SSD purchases.

Segment Performance and Growth

- Product revenue rose by 9% year-over-year to $768 million.

- Support revenue grew by 2% year-over-year to $635 million.

- Professional Services revenue, driven by Keystone, increased by 10% year-over-year to $87 million.

- Public Cloud revenue increased by 9% year-over-year to $168 million, with expectations for a return to double-digit growth in Q3.

Margin and Profitability Insights

- Consolidated gross margin was strong at 72%, near all-time highs.

- Product gross margin was 60%, with strategies in place to maintain margins in the high 50% range for the full fiscal year.

- Public Cloud gross margins improved significantly to 74% from 66% a year prior.

- Operating expenses were $719 million, a 2% increase year-over-year, showcasing disciplined operational execution.

Guidance and Future Projections

- Fiscal year ‘25 revenue guidance has been raised to between $6.54 billion and $6.74 billion, reflecting approximately 6% year-over-year growth at the midpoint.

- Consolidated gross margin for fiscal year ‘25 is expected to remain at 71% to 72%.

- EPS for fiscal year ‘25 is projected to range from $7.20 to $7.40, implying 13% growth year-over-year.

- Q3 revenue is expected to be between $1.61 billion and $1.76 billion, suggesting a 5% year-over-year growth at the midpoint.

- Q3 EPS is anticipated to be between $1.85 and $1.95, despite a year-over-year decline due to normalization factors.

Cash Flow and Capital Management

- Operating cash flow for Q2 was $105 million, lower than $135 million a year ago due to upfront SSD purchases.

- The company returned $406 million to stockholders through share repurchases and dividends in Q2.

- Approximately $800 million remains on the existing repurchase authorization.

- Debt of $400 million was repaid in the quarter, maintaining a healthy balance sheet with $2.2 billion in cash.

- Free cash flow for fiscal year ‘25 is expected to be slightly lower year-over-year due to timing of cash payments.

Q & A sessions,

Cloud Revenue Growth and Strategic Shift

- Total cloud revenue increased by 9% year-over-year, with first-party and marketplace services growing by 43%.

- Strategic shift from subscription models to first-party and marketplace services, which is approximately 20% of revenue and is intentionally declining.

- Expectations for consumption growth to surpass 80% in the coming quarters, solidifying the shift towards first-party and marketplace services.

Financial Performance and Guidance

- Q2 revenue was $1.66 billion, a 6% year-over-year increase.

- Billings increased by 9% year-over-year to $1.59 billion.

- EPS for Q2 was $1.87, exceeding guidance due to higher revenues and gross margins.

- Expect fiscal year ‘25 revenue to be between $6.54 billion and $6.74 billion, with EPS between $7.20 and $7.40.

Profitability Metrics and Cash Flow

- Q2 consolidated gross margin reached 72%, near all-time highs.

- Gross profit and operating profit dollars grew by 6% and 13% year-over-year, respectively.

- Operating cash flow was $105 million, and free cash flow was $60 million, impacted by strategic SSD purchases.

- Expectation for increased cash flow in the second half of fiscal year ‘25.

Market Position and Strategic Innovations

- All-flash storage revenue run rate reached $3.8 billion, growing 19% year-over-year.

- Keystone, the Storage-as-a-Service offering, saw a 55% revenue increase from the previous year.

- Notable advancements in AI and cloud storage segments, with significant wins in various industries.

Key Financial Figures

| Metric | Q2 2025 | Year-over-Year Change |

|---|---|---|

| Revenue | $1.66 billion | 6% |

| Billings | $1.59 billion | 9% |

| Gross Margin | 72% | – |

| EPS | $1.87 | N/A |