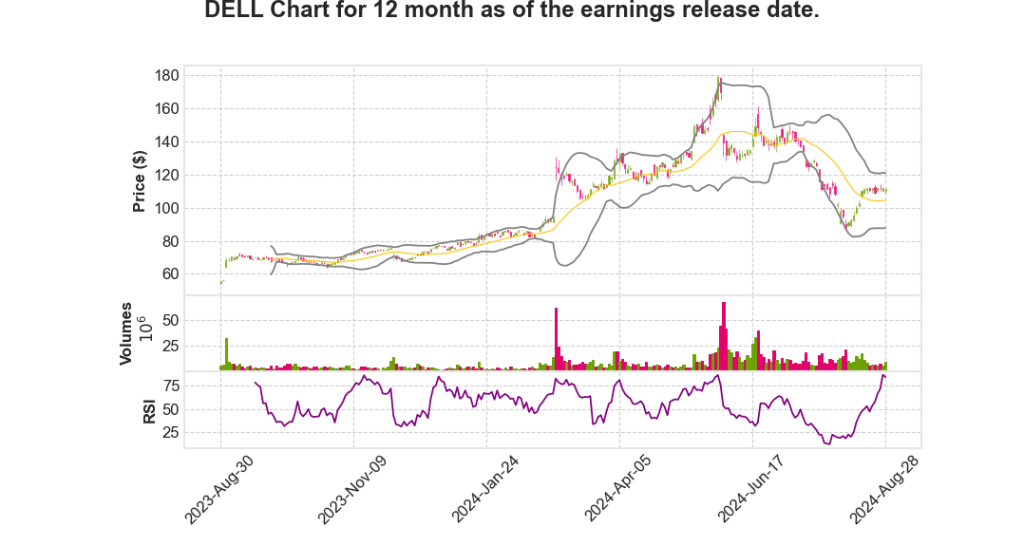

Dell Technologies Inc.

CEO : Mr. Michael Saul Dell

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2025 Q3 | 9.5% YoY | 11.8% | -283.5% | 2024-08-29 |

Yvonne McGill says,

Overall Performance and Financial Highlights

- Total revenue rose by 9% to $25 billion, despite challenges from exiting the VMware resale business.

- Gross margin decreased by 230 basis points to 21.8% of revenue, totaling $5.5 billion.

- Operating expenses were reduced by 4% to $3.4 billion, equating to 13.7% of revenue.

- Q2 net income increased by 7% to $1.37 billion, with diluted EPS up by 9% to $1.89.

Infrastructure Solutions Group (ISG) Performance

- ISG revenue reached a record $11.6 billion, marking a 38% increase.

- Server and networking revenue also set a record at $7.7 billion, up 80%.

- Storage revenue was down 5% to $4 billion, with mixed results across different product lines.

- ISG operating income rose 22% to $1.3 billion, with an improvement of 300 basis points in the operating income rate.

Client Solutions Group (CSG) Performance

- Overall CSG revenue decreased by 4% to $12.4 billion.

- Commercial revenue remained flat at $10.6 billion, but consumer revenue dropped 22% to $1.9 billion.

- CSG operating income reached $767 million, reflecting a 6.2% share of revenue.

- Future growth is anticipated, especially in Q4, driven by the PC refresh cycle and AI advancements.

Guidance and Projections

- FY ’25 revenue is projected to be between $95.5 billion and $98.5 billion, aiming for 10% growth.

- ISG is expected to grow roughly 30%, while CSG could see flat to low single-digit growth.

- Gross margin rate may decline by about 180 basis points due to competitive pressures and a higher AI server mix.

- Diluted non-GAAP EPS is anticipated to be $7.80 ± $0.25, representing a 9% increase at the midpoint.

Cash Flow, Share Repurchase, and Debt Management

- Q2 cash flow from operations was $1.3 billion, influenced by revenue growth and profitability.

- $1 billion was allocated towards capital returns, while another $1 billion was used for net debt reduction.

- 5.5 million shares were repurchased at an average price of $130.03.

- The core leverage ratio stands at 1.4x following these financial maneuvers.

Table of Key Financial Metrics

| Metric | Q2 2025 |

|---|---|

| Total Revenue | $25 billion |

| Gross Margin | $5.5 billion (21.8%) |

| Net Income | $1.37 billion |

| Diluted EPS | $1.89 |

| Cash Flow from Operations | $1.3 billion |

Jeff Clarke says,

Q2 2025 Financial Performance

- Revenue reached $25 billion, marking a 9% increase year-over-year.

- Diluted Earnings Per Share (EPS) increased by 9%, reaching $1.89.

- Generated cash flow from operations amounted to $1.3 billion.

- AI server shipments contributed significantly with $3.1 billion shipped in Q2.

AI Market Position and Outlook

- AI server orders and shipments continued sequential growth, with $3.2 billion in orders, largely from Tier-2 cloud service providers.

- The AI server backlog remains robust at $3.8 billion, indicating sustained demand.

- The pipeline of AI server opportunities expanded, now several multiples of the current backlog.

- The AI hardware and services TAM is projected to grow from $152 billion to $174 billion, with a 22% CAGR.

Expansion and Strategy in AI

- Optimized sales coverage to target AI opportunities across CSPs, enterprise, and sovereign AI markets.

- Added engineering capabilities, focusing on data center networking and design.

- Engaged in significant AI deals, achieving major deployments and gaining new customers consistently.

- Anticipate growth in AI adoption, with emerging AI opportunities in government sectors.

Traditional and AI Infrastructure Demand

- Traditional server demand experienced its third consecutive quarter of growth.

- Dell IP core storage (PowerMax, PowerScale, PowerStore, and PowerProtect Data Domain) saw double-digit growth.

Customer Solutions Group (CSG) Performance

- Commercial PC demand saw modest growth with healthy operating profitability.

- Expect further growth due to the upcoming PC refresh cycle and the end-of-life of Windows 10.

- Focus remains on profitable segments: commercial PCs, high-end consumer, and gaming markets.

Q & A sessions,

AI and Server Margins

- AI server margins improved sequentially, driven by enhanced value propositions beyond box sales to rack-level solutions.

- Growth attributed to selling networking, integration, and L11/L12 capabilities, allowing for value extraction from competition.

- Shipments of AI infrastructure nearly doubled quarter-over-quarter, with $6.5 billion shipped over the past 12 months against a demand of $9.5 billion.

- Backlog has a five-quarter pipeline, remaining healthy, with a significant potential for conversion to sales.

Enterprise Customer Growth and Pipeline

- Enterprise customers in the pipeline are increasing, indicating a shift from experimental to pilot testing of AI technology.

- Large Tier-2 CSP deployments remain a significant portion of the backlog and pipeline, reflecting scale needs.

- Expansion seen across various sectors, including life sciences, higher education, and financial services.

- Backlog includes shipments possible for Q3 and Q4, extending into the next year.

Product Growth and Margin Performance

- Double-digit growth in demand for Dell’s high-end, mid-range, unstructured, and data protection products.

- Improved margin rates attributed to better pricing discipline and a favorable product mix towards Dell IP products.

- Partner IP business saw a decline, shifting focus to more profitable Dell IP offerings.

- Geographic product mix saw significant contributions from North America.

Market Outlook and Refresh Expectations

- Optimism remains for a market refresh, particularly with the approaching end-of-life for Windows 10 driving new AI-integrated product demands.

- Predicted refresh now expected toward the end of 2024 into 2025, with potential for a rapid market snap-back.

- Growing opportunity seen in deploying AI at the Edge, with small language models enhancing productivity.

- Newer AI applications and PC enhancements expected to drive significant market opportunities.

Financial Guidance and Market Conditions

- Q3 expectations set for CSG and ISG to grow 14% with total revenue at $24.5 billion, up 10% year-over-year.

- ISG projected to grow 30% year-over-year, led by AI servers and steady traditional server performance.

- Gross margin rates anticipated to rise slightly, despite the competitive and inflationary environment.

- Operating expenses forecasted to decrease by 2% quarter-over-quarter, driven by ISG and storage performance improvements.

| Quarter | Revenue Growth | ISG Growth | CSG Growth | OpEx Change |

|---|---|---|---|---|

| Q3 | 10% YoY | 30% YoY | Flat to low-single digits | -2% QoQ |