Lululemon Athletica Inc.

CEO : Mr. Calvin R. McDonald

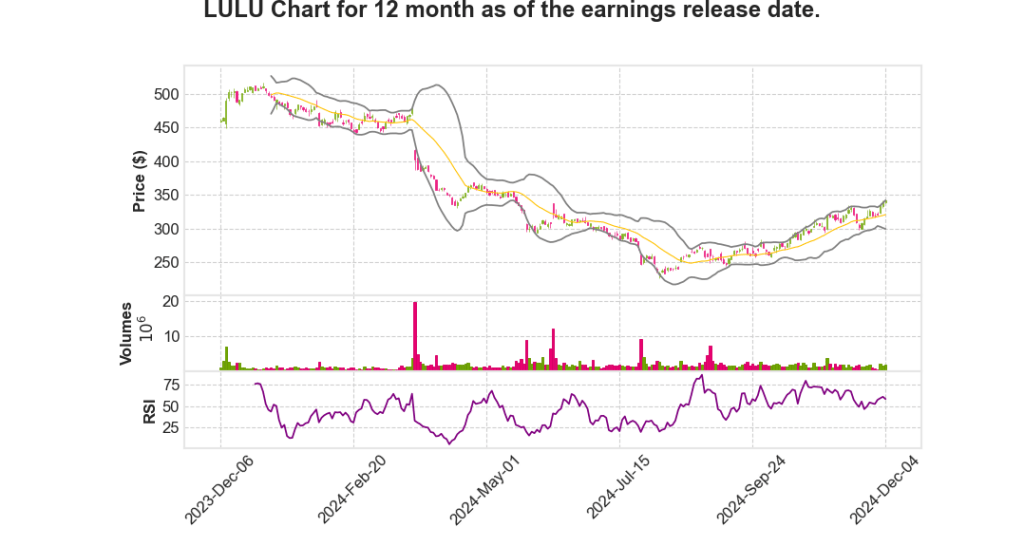

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q3 | 8.7% YoY | 45.1% | 45.7% | 2024-12-05 |

Calvin McDonald says,

Black Friday and Holiday Season Performance

- Record visits to Lululemon’s shop app and e-commerce site during Black Friday.

- Full-price sales were driven by key franchises, including Define.

- Strategic planning for the shorter holiday shopping season to maximize revenue.

- Lululemon leverages increased traffic to clear non-forward products while emphasizing full-price styles.

Quarter Three Financial Performance

- Total revenue increased by 9%, or 8% in constant currency.

- Adjusted operating margin rose by 70 basis points to 20.5%.

- Adjusted earnings per share saw a significant increase of 13%.

- An additional $1 billion authorized by the Board for the share repurchase program, with $1.8 billion still available.

Regional and Product Performance

| Region | Revenue Increase | Constant Currency Increase |

|---|---|---|

| China Mainland | 39% | 36% |

| Rest of World | 27% | 23% |

| Americas | 2% | 2% |

- Men’s merchandise increased by 9%, while women’s and accessories both increased by 8%.

- Integration of merchandising and brand teams enhances product innovation.

International Growth and Brand Strategy

- International revenue saw a substantial increase of 33%, or 30% in constant currency.

- Successful activations in China, including events for World Mental Health Day with 15,000 participants.

- Expansion plans include new countries such as Italy, Denmark, Belgium, Turkey, and the Czech Republic.

- Unaided brand awareness remains low in the U.S. at 36%, highlighting room for growth.

Product and Strategic Partnerships

- Strength in women’s shorts, skirts, and leggings in seasonal colors; Pace Breaker and Zeroed In franchises performing well in men’s.

- Success in play categories like tennis, with a shift towards consistent newness throughout the year.

- Strategic partnerships with Fanatics, NHL, and Disney to leverage iconic styles and expand reach.

- Lululemon remains on track to meet its Power of Three x2 revenue target of $12.5 billion by 2026, ahead of schedule.

Meghan Frank says,

Q3 2024 Financial Performance Overview

- Total net revenue rose by 9% to $2.4 billion, or 8% in constant currency.

- Comparable sales increased by 3% in constant currency.

- Gross profit for the third quarter was $1.4 billion, representing 58.5% of net revenue, an increase from 58.1% in Q3 2023.

- Net income for the quarter was $352 million, equating to $2.87 per diluted share, up from $2.53 in Q3 2023.

Geographical Revenue Breakdown

- Americas revenue increased by 2% despite a comparable sales decline of 2%.

- China Mainland saw a remarkable 39% revenue increase, or 36% in constant currency, with a 24% rise in comparable sales.

- Rest of World segment reported a 27% revenue growth, or 23% in constant currency, with a 20% increase in comparable sales.

Store and Digital Channel Performance

- Total sales in the store channel increased by 13%, with 749 stores globally at the end of the quarter.

- Square footage increased by 16% YoY, significantly driven by the addition of 63 net new stores.

- The digital channel contributed $945 million, making up 39% of total revenue with a 4% increase in revenue.

Guidance and Forward-Looking Statements

- Full year 2024 revenue is expected to be between $10.452 billion and $10.487 billion, a 9% increase over 2023.

- Q4 2024 revenue projection ranges from $3.475 billion to $3.51 billion, representing 8% to 10% growth.

- Diluted EPS for the full year 2024 is projected between $14.08 and $14.16, compared to $12.77 for 2023.

Capital Investments and Stock Repurchase Activity

- Capital expenditures for 2024 are anticipated to be approximately $670 million to $690 million.

- Share repurchase for Q3 totaled 1.58 million shares at an average price of $259, with $1.8 billion remaining under the repurchase program.

Q & A sessions,

Customer Engagement and Brand Loyalty

- Over 24 million members are part of the Essential membership program in North America, demonstrating strong brand loyalty.

- Engagement and retention are driven by membership perks and partnerships with third-party studio players.

- Core customers are responding well to product newness, indicating a return to historical engagement levels.

Product Newness and Assortment Strategy

- The level of newness in product assortment is below historical levels but is expected to reach past standards by Q1 2025.

- Efforts are focused on adding new colors, patterns, and prints to core franchises, which are key drivers of business.

- New product introductions such as defined jackets, Velvet Scuba collection, and Shine Align collection are performing well.

Geographic Expansion and Market Growth

| New Market | Model | Expected Opening |

|---|---|---|

| Italy | Owned Market | Next Year |

| Denmark, Belgium, Turkey, Czech Republic | Franchise Model | Next Year |

- International markets show balanced growth, with particular strength in North America and Canada.

- The business model focuses on brand momentum and market readiness, ensuring sustainable growth.

Financial Performance and Guidance

- Recent growth has been seen in both men’s and women’s premium activewear categories globally and in the U.S.

- There is optimism about Q1 2025, driven by new product launches and strong customer engagement metrics.

- International revenue is expected to increase, representing a higher percentage of overall company revenue.

Marketing and Guest Acquisition

- Utilizing Return on Ad Spend (ROAS) for evaluating marketing initiatives, with successful guest acquisition and brand awareness growth.

- The unaided brand awareness in the U.S. has increased to 36%, indicating effective top-of-funnel initiatives.

- Focus on community events and ambassador relationships to strengthen local market presence and customer engagement.