Broadcom Inc.

CEO : Mr. Hock E. Tan

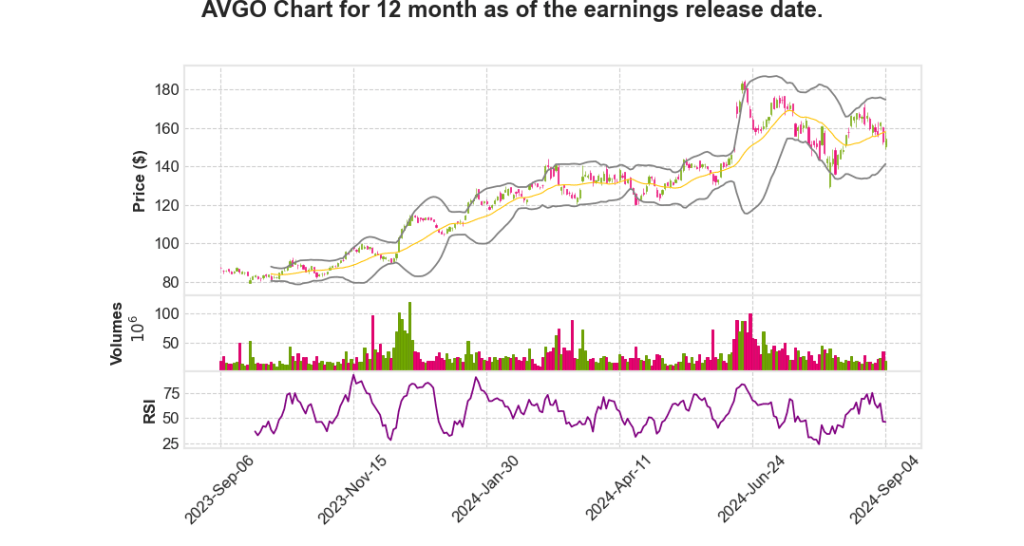

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q4 | 51.2% YoY | 9.1% | 8.2% | 2024-09-05 |

Hock Tan says,

Q3 2024 Financial Performance

- Consolidated net revenue was $13.1 billion, reflecting a 47% increase year-on-year.

- Operating profit saw a growth of 44% year-on-year.

- AI revenue, VMware bookings, and stabilized non-AI semiconductor revenue were highlighted as key drivers.

Guidance and Future Outlook

- Transitioned from providing annual guidance to quarterly guidance for Q4.

- Projected Q4 consolidated revenue is approximately $14 billion, up 51% year-on-year.

- Full fiscal 2024 revenue outlook raised to $51.5 billion; adjusted EBITDA for the year to 61.5%.

Software Segment Performance

- Infrastructure software revenue of $5.8 billion in Q3, a 200% year-on-year increase.

- VMware contributed $3.8 billion to the infrastructure software revenue.

- VMware’s annualized booking value (ABV) rose to $2.5 billion, up 32% from the previous quarter.

- Cost reduction in VMware spending, reduced to $1.3 million in Q3 from $1.6 million in Q2.

Semiconductor Segment Insights

- Networking revenue reached $4 billion in Q3, increasing 43% year-on-year.

- Non-AI networking revenue increased 17% sequentially in Q3.

- Q3 wireless revenue was $1.7 billion, up 1% year-on-year.

- Broadband and industrial resales faced year-on-year declines but are expected to recover.

AI Demand and Revenue Forecast

- AI revenue projected to grow sequentially by 10% in Q4 to exceed $3.5 billion.

- Total AI revenue for fiscal 2024 expected to be $12 billion, surpassing the prior guidance of over $11 billion.

- Q4 semiconductor revenue anticipated to be about $8 billion, marking a 9% year-on-year increase.

Kirsten Spears says,

Q3 2024 Financial Performance Overview

- Consolidated revenue reached $13.1 billion, marking a 47% year-over-year increase.

- Excluding VMware’s contribution, year-over-year revenue growth was 4%.

- Gross margins stood at 77.4% of revenue, with operating income at $7.9 billion, up 44% year-over-year.

- Adjusted EBITDA was $8.2 billion, representing 63% of revenue.

Segment Analysis

- Semiconductor Solutions:

- Revenue: $7.3 billion, up 5% year-on-year.

- Gross margins at approximately 68%, down 270 basis points year-on-year.

- Operating expenses increased by 11% to $881 million.

- Infrastructure Software:

- Revenue: $5.8 billion, up 200% year-on-year due to VMware’s contribution.

- Gross margins at 90%, with operating margin at 67%.

Cash Flow and Balance Sheet Highlights

- Free cash flow was $4.8 billion, or 37% of revenues, with adjustments leading to a 14% year-on-year increase to $5.3 billion.

- Capital expenditures totaled $172 million; inventory increased by 3% sequentially to $1.9 billion.

- Cash ended at $10 billion, with gross principal debt at $72.3 billion.

- Debt restructuring involved replacing $5 billion in floating rate notes and reducing floating rate debt by $4.2 billion.

Capital Allocation and Shareholder Returns

- Dividends paid totaled $2.5 billion, with a cash dividend increase to $0.53 per share for Q4.

- Eliminated 8.4 million AVGO shares due to vesting of employee equity, affecting the non-GAAP diluted share count.

Q4 2024 Guidance and Forward-Looking Statements

- Projected Q4 consolidated revenue of $14 billion, with adjusted EBITDA of approximately 64%.

- Expected consolidated gross margins to decrease by approximately 100 basis points sequentially.

- GAAP net income and cash flows to be impacted by higher taxes and restructuring costs.

| Key Metrics | Q3 2024 | Guidance for Q4 2024 |

|---|---|---|

| Consolidated Revenue | $13.1 billion | $14 billion (projected) |

| Adjusted EBITDA | $8.2 billion | Approx. 64% |

| Dividend per Share | $0.525 | $0.53 |

Q & A sessions,

Non-AI Semiconductor Market Recovery

- The company has passed through the bottom of the down cycle for non-AI semiconductors.

- Bookings for Q3 in non-AI semiconductor demand are up by 20%.

- Recovery is observed in enterprise sectors such as enterprise data centers and IT spending.

- Q4 is expected to continue this recovery trend, leading into 2025.

AI Infrastructure Demand

- As AI permeates enterprises, there is a need for upgrading servers, storage, and networking.

- An upcycle is projected, potentially surpassing previous cycles due to AI-induced hardware refresh requirements.

Software Segment Stability and Growth Prospects

- The software side has reached a level of stability, particularly in non-VMware revenue.

- Focus is on how VMware will perform over the next 1 to 1.5 years.

Custom Silicon and AI Accelerators

- Large hyperscalers are moving toward creating their own custom compute silicon and accelerators.

- This transition is expected to continue over the next several years, driven by the need to handle large language models and AI workloads.

- The company is well-positioned to provide accelerators and networking solutions to AI data centers of large hyperscalers.

Partnerships and Storage Technology

- The company is collaborating to sustain hard disk drive media as a long-term storage solution.

- There is an ambition to develop hard disk drives from 22-24 terabytes to 30, 40, and even 50 terabytes within five years.

- This involves integrating engineers and designers to enhance technology development.