Carnival Corporation & plc

CEO : Mr. Joshua Ian Weinstein

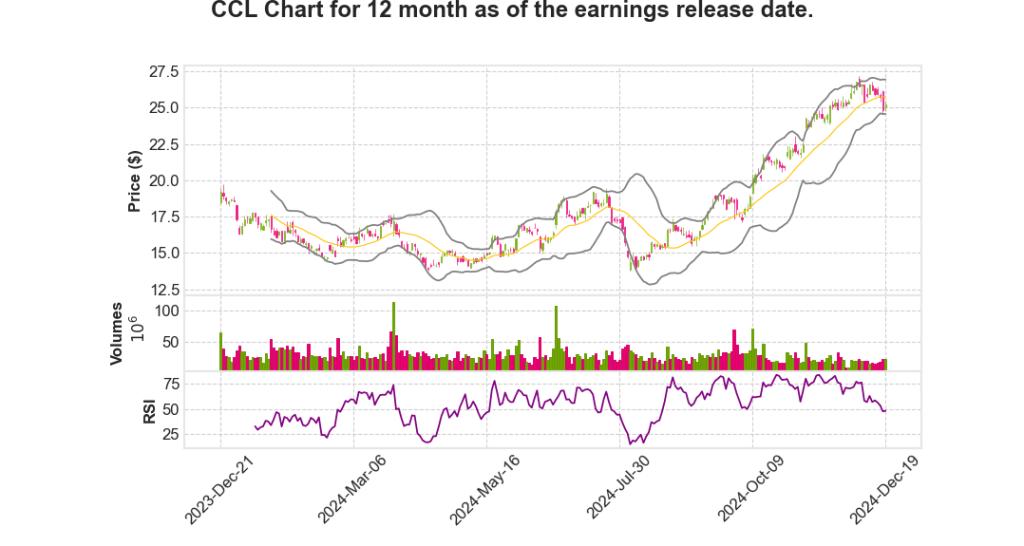

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q4 | -28.6% YoY | 46.1% | -705.3% | 2024-12-20 |

David Bernstein says,

Fourth Quarter 2024 Financial Highlights

- Net income exceeded September guidance by $126 million.

- Revenue favorability contributed $77 million due to a 6.7% increase in yields compared to the prior year.

- Cruise costs without fuel per ALBD increased by 7.4% from the previous year, bettering guidance by $13 million.

- Per diems improved by over 5% versus the previous year, driven by higher ticket prices and onboard spending.

- Record performance in revenues, yields, per diems, and customer deposits for the fourth quarter.

Refinancing and Deleveraging Efforts

- Full-year yield improvement at 11% outpaced the 3.5% increase in costs.

- EBITDA reached $6.1 billion with cash from operations at approximately $6 billion.

- Over $5 billion in debt payments made during 2024, including over $3 billion in prepayments.

- Net debt to EBITDA ratio improved to 4.3 times, progressing towards investment-grade leverage.

- Plans to capitalize on improved interest rates and manage debt maturity for 2027 onwards.

2025 Full-Year Guidance

- Yield improvements projected to increase earnings by over 60 cents per share compared to 2024.

- Cruise costs (excluding fuel) expected to rise by approximately 3.7%, impacting earnings by 28 cents per share.

- Celebration Key, a new Bahamian destination, expected to contribute positively despite increased operational costs.

- Projected net income for 2025 is over $2.3 billion, a $400 million improvement from 2024.

Cost and Revenue Implications

- Fuel prices expected to favorably impact 2025 by approximately nine cents per share.

- Foreign currency exchange rates projected to negatively impact earnings by five cents per share.

- EUA regulation changes will increase carbon emission costs, impacting fuel expenses by about $0.03 per share.

- Higher depreciation and lower interest income offset by improvements in interest expense due to refinancing efforts.

Strategic Outlook

- Anticipated strong demand and operational execution driving robust financial performance.

- Continuing to focus on rebuilding financial strength and transferring value from debt holders to shareholders.

- Confidence in achieving investment-grade leverage metrics in the coming years.

Josh Weinstein says,

Record Revenue and Improved Financial Performance

- Fourth quarter net income improved by over $250 million year-over-year, exceeding expectations by $125 million.

- The company achieved record revenues for the seventh consecutive quarter, driven by strong demand across its global portfolio.

- Full-year revenues reached an all-time high of $25 billion.

- Cash from operations for the year was nearly $6 billion, marking another all-time high.

Yield and Pricing Trends

- Full-year 2024 yield increased by 11%, with over 250 basis points improvement on original guidance.

- The yield increase was primarily due to higher prices driven by strong demand.

- Prices for 2024 were up across all major brands, ranging from mid-single-digit to mid-teen percentage increases.

- Onboard spending levels continued to rise sequentially each quarter.

Cost Management and Operational Efficiency

- Unit costs were 100 basis points better than the original guidance for the year.

- Cost savings initiatives and easing inflation contributed to improved cost management.

- The company saw an additional $700 million added to its bottom line compared to December guidance.

Progress Towards 2026 Financial Targets

- Significant progress was made towards the 2026 sea change targets.

- EBITDA per ALBD target calls for a 50% increase from the 2023 baseline.

- ROIC target of 12% aims to be the highest in almost 20 years; ended 2024 at 11%.

- The company is already over 80% of the way toward achieving these targets.

Long-term Shareholder Value

- Current ROIC comfortably exceeds the company’s cost of capital.

- Delivering long-term value and setting a strong foundation for 2025 and beyond.

- The company is focused on continuing momentum to build further shareholder value in future years.

Q & A sessions,

Financial Performance and Guidance

- Projected Yield Growth: 2025’s yield growth is expected to exceed 4%, contributing more than $400 million to the bottom line.

- 2024’s yield growth, even without the addition of new ships, was nearly 10% over 2023.

- Booking trends accelerated despite reduced inventory, with 2025 booking volumes higher year-on-year at increased prices.

- 2026 EBITDA per ALBD target is expected to be achieved a year early.

- ROIC is projected to approach the 12% target by 2026.

Operational Highlights

- Introduction of three new ships in 2024, including Carnival Jubilee and Cunard’s Queen Anne, bolstering the fleet.

- Company’s strategy focuses on existing ships, driving demand growth through improved operational execution.

- Continued investment in talent and tools to enhance commercial execution and yield management.

- Significant double-digit growth in both new-to-cruise and repeat guests in 2024.

Marketing and Destination Strategy

- Launch of new marketing campaigns across all brands to boost awareness and consideration for cruise travel.

- Enhancement of destination strategies, including the opening of Celebration Key in six months and renaming Half Moon Key to Relax Away Half Moon Key.

- Plans to expand and capitalize on Caribbean destinations to attract new-to-cruise guests.

- Efforts to entice potential guests to choose cruises by emphasizing unique destination experiences.

Sustainability and Financial Position

- Significant reduction in greenhouse gas emissions: 17.5% reduction in emissions intensity versus 2019, on track to achieve a 20% reduction by 2026.

- Debt reduction of over $8 billion in under two years, resulting in improved leverage metrics.

- 2025 guidance targets a 3.8 times net debt to EBITDA, aiming for investment-grade leverage metrics by 2026.

Challenges and Strategic Adjustments

- Potential tax changes in Mexico, though not yet factored into 2025 forecasts.

- Strategic adjustments in cruise itineraries to mitigate potential impacts from geopolitical changes.

- Continuous portfolio management and allocation of ships to optimize returns.

- Focus on enhancing the appeal of owned destinations to attract both cruise and non-cruise guests.