Paychex, Inc.

CEO : Mr. John B. Gibson Jr.

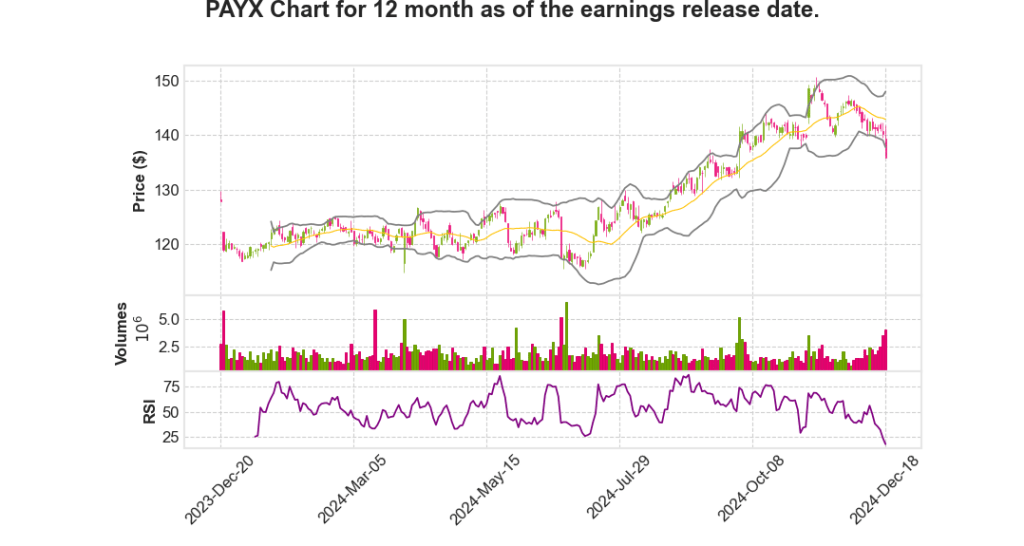

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2025 Q2 | 4.7% YoY | 6.3% | 5.5% | 2024-12-19 |

John Gibson says,

Revenue and Earnings Growth

- Revenue growth in the second quarter was 7%, excluding the impact of the expiration of the ERTC program.

- Diluted earnings per share grew by 6%, reflecting efficient operational strategies.

- The growth is attributed to the demand for Paychex’s comprehensive suite of HCM solutions and HR technology.

Market Demand and Investment

- Strong demand in HR technology and advisory solutions due to a challenging labor market and rising healthcare costs.

- Significant investments in advertising to drive awareness and product adoption, particularly in PEO and middle market HCM businesses.

- Fully staffed sales and service teams to capitalize on the key selling season.

Client Retention and Engagement

- Revenue retention improved and remains above pre-pandemic levels, with client retention near record levels.

- Client losses have decreased over the past year, showing improvements across all employee size segments.

- High engagement with the new HR analytics solution, with over 80% of early adopters actively engaging with the platform since its September launch.

Product and Technology Innovations

- Introduction of the Paychex Recruiting Copilot, a digitally AI-powered solution to assist in talent acquisition.

- Launch of Premium Plus, offering compensation benchmarks and AI-driven insights to help clients manage and develop talent strategies.

- Paychex Flex Perks, a digital marketplace offering affordable benefits to employees, already engaged over 100,000 client employees since September launch.

Awards and Industry Recognition

- Paychex Flex Perks received the Top HR Product of the Year Award and a Brandon Hall Excellence in HR Technology Silver Award.

- Paychex was named a leader in payroll services by NelsonHall for the eighth consecutive year.

- This industry recognition underscores Paychex’s ability to deliver immediate client benefits and meet future requirements.

| Key Metrics | Second Quarter (Q2) |

|---|---|

| Revenue Growth | 7% (excluding ERTC impact) |

| Earnings Per Share Growth | 6% |

Bob Schrader says,

Q2 2025 Financial Results

- Total revenue for the quarter increased by 5% to $1.3 billion, despite a 200 basis point headwind from the expiration of the ERTC program. Excluding this headwind, revenue grew 7%.

- Management Solutions revenue rose 3% to $963 million, driven by client growth and higher product penetration, although partially offset by lower ERTC revenues.

- PEO and Insurance Solutions revenue grew 7% to $318 million, supported by higher average worksite employees.

- Interest on funds held for clients increased by 15% to $36 million due to higher interest rates and invested balances.

- Operating income increased 6% to $538 million with a margin of 40.9%, up approximately 60 basis points year-over-year.

First Half Fiscal Year 2025 Performance

- Total revenue grew 4% to $2.6 billion, affected by a 300 basis point ERTC headwind and fewer processing days in Q1. Excluding these, revenue rose 7%.

- Operating margins expanded by approximately 20 basis points to 41.2%, demonstrating resilience against the ERTC impact.

- Diluted earnings per share increased 4% to $2.32, while adjusted diluted earnings per share rose 3% to $2.30.

- Cash flow from operations was robust at $841 million, supporting shareholder returns of $810 million through dividends and share repurchases.

Fiscal Year 2025 Guidance

- Total revenue is projected to grow between 4% and 5.5%, with a 200 basis point ERTC headwind accounted for.

- Management Solutions revenue is anticipated to rise 3% to 4%, while PEO and Insurance Solutions are forecasted to grow by 7% to 9%.

- Interest on funds held for clients is expected to be between $145 million and $155 million.

- Operating income margin is projected to be between 42% and 43%, with a potential to reach the higher end of this range.

- Adjusted diluted earnings per share is expected to grow between 5% and 7%.

Q3 2025 Outlook

- Total revenue growth is anticipated between 4.5% and 5%, with a 150 basis point ERTC headwind, marking the last quarter of its impact.

- Operating margin is expected to be between 46% and 47%, benefitting from annual form filings.

- All projections are based on current conditions and assumptions, with updates to follow in the next earnings call.

Key Financial Data

| Measure | Q2 2025 | First Half FY 2025 |

|---|---|---|

| Total Revenue | $1.3 billion | $2.6 billion |

| Operating Income | $538 million | — |

| Diluted EPS | $1.14 | $2.32 |

| Adjusted Diluted EPS | $1.14 | $2.30 |

| Cash flow from Operations | — | $841 million |

Q & A sessions,

PEO Performance and Market Dynamics

- Paychex’s PEO (Professional Employer Organization) is experiencing high double-digit growth in contracted revenue and client adds for the second consecutive year.

- Record retention rates are reported in the PEO segment, with proposals also rising in high double digits.

- Health inflation is prompting clients to reassess their options annually, providing opportunities for Paychex to stand out with a diverse range of offerings.

- The PEO has expanded insurance penetration, with increased attachment and participation levels, resulting in mid-single-digit growth in actual insurance within the PEO.

Use of AI and Technological Advancements

- The company is leveraging AI and analytics during insurance renewal periods to evaluate health insurance payments and target potential value propositions.

- Paychex has introduced products like the Paychex Flex Engage, an AI-based engagement tool, and Paychex Recruiting Copilot, an AI-assisted talent acquisition solution.

- AI-driven initiatives are significantly increasing customer engagement, with over 80% of early adopters engaging with new platforms.

- Investment in AI and digital HR tools is enhancing productivity and offering competitive advantages.

Insurance and Health Plan Strategies

- Despite flat growth in the Florida at-risk MPP insurance revenue, insurance penetration within the PEO remains strong.

- Employees are increasingly opting for lower-cost health plans, doubling the percentage of downgrades compared to typical single-digit trends.

- Health inflation is acknowledged as a critical issue, with disciplined management needed to balance growth and risk.

Market Trends and Strategic Positioning

- Paychex is experiencing increased proposal volumes and call activities, indicating a return to pre-COVID market conditions.

- The company’s comprehensive suite of offerings allows for long-term client relationships, reducing the need for multiple vendors.

- Emphasis on value and consistent service is helping retain clients and grow revenue across market segments.

- There is a notable shift towards rationality in market pricing and profitability, aligning with Paychex’s disciplined growth strategy.

Future Growth Opportunities

- Paychex is not planning any mergers or acquisitions, focusing instead on organic growth and disciplined expansion.

- There’s a substantial pipeline of opportunities for scale in both new and existing markets.

- Continued investment in digital HR and data analytics is expected to drive future growth and enhance product offerings.

- Client retention and revenue retention have improved, with hiring intentions rebounding to the highest level since last November.

| Metric | Growth | Remarks |

|---|---|---|

| PEO Contracted Revenue | High Double Digits | Second consecutive year of growth |

| Insurance Penetration | Mid-Single Digits | Expansion despite flat revenue in Florida |

| Downgrade in Health Plans | Double Percentage | Indicative of cost control measures |

| Client Engagement with AI Platforms | 80%+ | Strong early adoption |