Fastenal Company

CEO : Mr. Daniel L. Florness

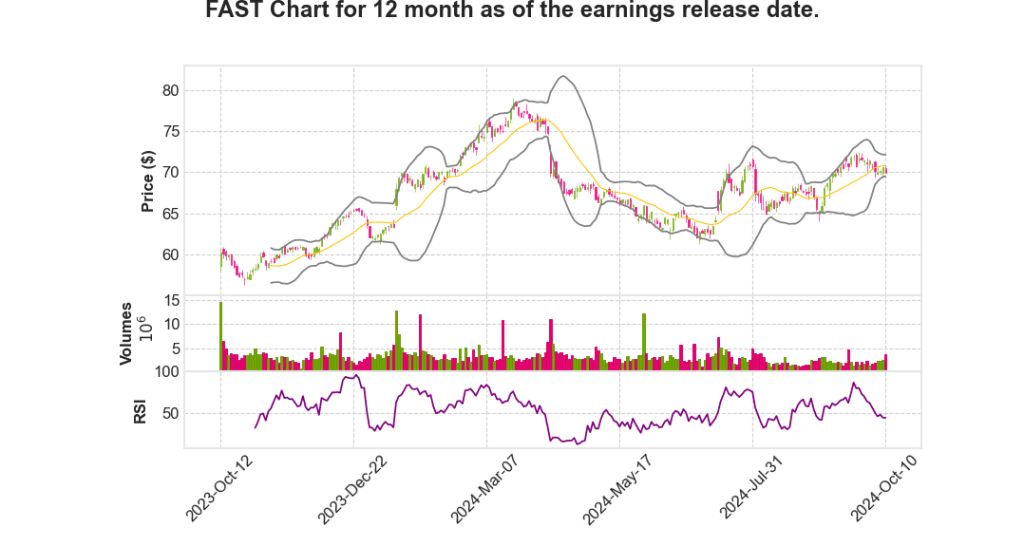

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q4 | 3.7% YoY | -2.6% | -2.1% | 2024-10-11 |

Dan Florness says,

Financial Performance and Guidance

- Third-quarter net sales increased by 3.5%, with earnings per share (EPS) rising to $0.52, marking a 1% growth from the previous year.

- Daily sales rate growth was at 1.9%, indicating a modest increase in business activity.

- The quarter ended on a strong note despite hurricane impacts, showcasing resilience in operations and adaptability in logistics strategies.

- Active sites have increased by about 12% since the end of Q3 2023, with 93 Onsites signed in the quarter, although the goal of reaching 375 to 400 active sites is projected to be at the lower end of that range.

Operational Flexibility and Strategic Developments

- Flexibility in transportation and distribution has been critical, with successful adjustments in truck routes during the hurricane to meet customer demands.

- Enhanced asset efficiency and inventory strategies are expected to improve supply chain costs and margins, potentially accelerating growth.

- Fastenal’s IT and business analytics capabilities are expanding, providing valuable insights through the FMI platform.

Customer Engagement and Growth Strategy

- The focus has shifted from opening more branches to enhancing customer engagement through Onsite expansions and key account acquisitions.

- From 2007 to 2023, Fastenal added approximately 9,400 customer sites sourcing more than $10,000 monthly, representing 93% of growth.

- 78% of current sales originate from customer sites with over $10,000 monthly sourcing, illustrating a focus on increasing wallet share.

Digital and eCommerce Initiatives

- The digital footprint now encompasses 61.1% of sales, up from 57% a year ago, indicating a significant shift towards digital engagement.

- eCommerce grew by 25.5%, driven primarily by eProcurement services with a growth rate of over 30%, while web-centric eCommerce grew in single digits.

- Realignment of digital strategy has been undertaken, with all digital aspects including eCommerce and FMI technologies now under the FMI digital solutions group.

Leadership and Organizational Changes

- Donnalee Papenfuss has been elected as a new officer after 25 years at Fastenal, reflecting internal recognition and promotion.

- Jeff Watts’ team is credited for strategic personnel moves that have positively impacted operational alignment and sales performance.

Holden Lewis says,

Sales Performance and Market Conditions

- The daily sales rate in Q3 2024 increased by 1.9%, despite setbacks from Hurricane Helene, which reduced the rate by 5 to 25 basis points.

- Industrial market challenges persist, with the Purchasing Manager’s Index indicating manufacturing contraction for 22 of the last 23 months.

- Reseller end market sales declined significantly by 11.3% compared to a 6.4% decline in Q2 2024, indicative of channel destocking.

- September’s daily sales rate saw an improvement to 3.2% despite adverse hurricane impacts and moderating growth in warehousing.

- Strong contract, FMI, and Onsite signings build momentum for improved customer acquisition.

Financial Metrics and Margins

- Operating margin in Q3 2024 was 20.3%, down 70 basis points from the previous year.

- Gross margin was 44.9%, a decrease of 100 basis points year-over-year.

- SG&A expenses comprised 24.6% of sales, improved from 25% in the same period last year due to increased supplier marketing credits.

- Discretionary costs rose by 3.7% in Q3 2024, exceeding the daily sales rate growth.

- EPS remained steady at $0.52, matching Q3 2023 figures.

Cash Flow and Capital Expenditure

- Operating cash generated in Q3 2024 was $297 million, representing 100% of net income.

- Debt decreased to 6.3% of total capital, down from 7% in the previous year.

- Accounts receivable increased by 2.5%, aligning with sales growth and a shift towards larger customers.

- Net capital spending was $55.8 million, higher than $42.9 million in Q3 2023, driven by investments in hub automation and distribution centers.

- The full-year net capital spending is expected to range between $235 million and $255 million, trending towards the lower end.

Inventory and Supply Chain Management

- Inventories increased by 3%, marking the first annual increase since Q1 2023 as the company moves past the supply chain crisis.

- Efforts to add incremental inventory, particularly fasteners, aim to improve availability and support efficiency in distribution centers.

- An additional $25 million in new inventory was added in Q3 2024, with plans for another $5 million to $10 million in Q4 2024.

Outlook and Strategic Initiatives

- No significant changes in underlying business activity expected in Q4 2024 due to continued weak market demand.

- Focus remains on balancing cost management with growth investments, particularly in Onsite personnel, IT, and business analytics.

- Efforts in reducing sales-related travel costs while enhancing customer acquisition strategies are underway.

- Inventory and capital spending initiatives are aimed at long-term growth and operational efficiency improvements.

- Future growth is expected as market conditions stabilize and signings momentum supports sales trends into 2025.

Q & A sessions,

Market Outlook and Business Environment

- The speaker remains cautiously optimistic about 2025, predicting a higher probability that business conditions will stabilize or marginally improve, rather than decline further.

- The ISM (Institute for Supply Management) index, a key visibility indicator for the company, is currently not providing favorable insights, adding uncertainty to the forecast.

- Customer business performance has declined since November 2022, but there is confidence that the trend may plateau or slightly improve.

- The company’s growth is expected to shine through if business conditions remain stable or improve slightly.

Order and Revenue Metrics

- In January, the company processed 16,387 orders per day, with an average order value of $224. By May, the average order value dropped to $214 and slightly rebounded to $216 by September.

- Order volume increased by 11.5% from January to September, with a rise in daily scans from 16,387 to 18,290.

- If the average order value returns to $224, it could add an estimated $3 million in monthly revenue.

Sector Performance and Growth Factors

- Construction business saw a marginal growth of 0.9% in September after a series of negative quarters, marking a positive change in trend.

- Government accounts, which comprise 4% of sales, experienced a notable growth in September, driven by strong Onsite signings.

- Regional performance varied, with Eastern US business growing nearly 5%, while Western US business remained slightly negative.

Strategic Initiatives and Implementation

- The company plans to shift its focus to customer acquisition and maturity, emphasizing the growth of customer accounts of varying sizes.

- Infrastructure improvements continue, with a focus on aligning national accounts and enhancing customer service capabilities in local markets.

- Investment strategy targets 3% of sales, with a third allocated to FMI, 40% to distribution and transportation, and the remainder to IT.

Growth Strategy and Future Plans

- The company aims to increase revenue by $1 billion annually, with strategic initiatives to support this goal.

- Upcoming Analyst Day planned for April to further discuss growth strategies and KPIs.

- Leadership changes and organizational alignments are geared towards achieving ambitious growth targets.