JPMorgan Chase & Co.

CEO : Mr. James Dimon

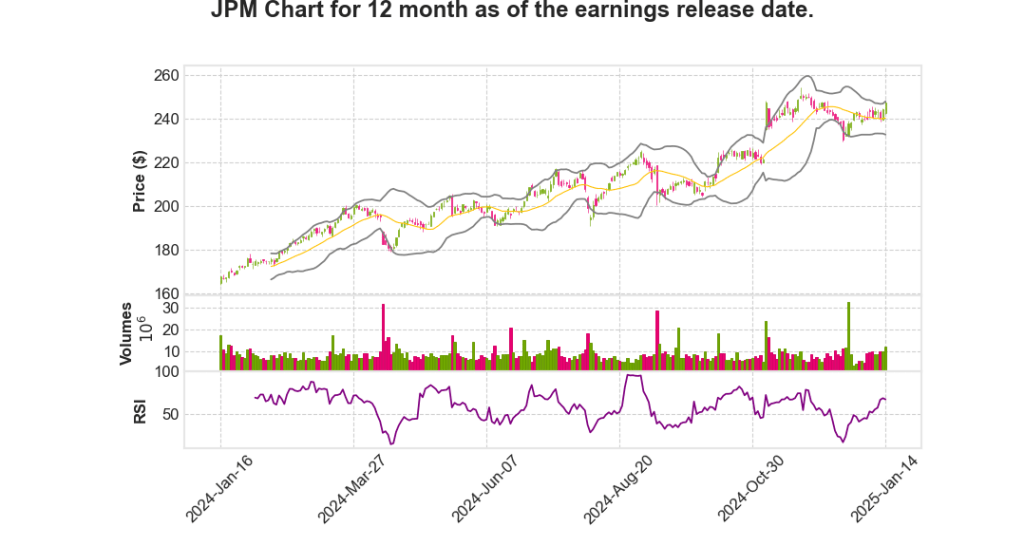

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q3 | -0.5% YoY | 94.9% | 1.2% | 2025-01-15 |

Jeremy Barnum says,

Financial Performance Overview

- The firm reported a net income of $14 billion for Q4 2024, with EPS at $4.81 on revenue of $43.7 billion, reflecting a 10% increase year-on-year.

- Return on tangible common equity (ROTCE) was at 21% for the quarter.

- Total revenue for the year was $173 billion, with net income reaching $54 billion and EPS of $18.22.

- Expenses for the quarter were $22.8 billion, marking a 7% decline year-on-year, although excluding the prior year’s FDIC special assessment, expenses rose by 5%.

Segment Performance and Highlights

- Consumer & Community Banking (CCB) reported a net income of $4.5 billion, with revenues up 1% year-on-year.

- Commercial & Investment Bank (CIB) achieved net income of $6.6 billion, with investment banking fees up 49% year-on-year.

- Asset & Wealth Management (AWM) recorded net income of $1.5 billion, driven by a 13% increase in revenue year-on-year.

- Corporate revenues were up $223 million year-on-year, with net income at $1.3 billion.

Balance Sheet and Capital Ratios

- The Common Equity Tier 1 (CET1) ratio improved to 15.7%, a 40 basis points increase from the prior quarter.

- The firm conducted $4 billion in net common share repurchases during the quarter.

- Long-term net inflows for AWM were $76 billion for the quarter and $140 billion for the full year.

Guidance and Outlook for 2025

- 2025 Net Interest Income (NII) ex-markets is projected to be approximately $90 billion, influenced by anticipated rate cuts.

- Firm-wide expenses are expected to reach about $95 billion, driven by growth in auto leasing and capital markets.

- Card net charge-off rate is anticipated to align with previous guidance at approximately 3.6%.

- The firm expects a visible growth trend in deposits during the second half of 2025.

Environmental and Social Responsibility

- In response to the Los Angeles wildfires, the firm is actively supporting local communities and employees.

- Actions include waiving banking fees and contributing to relief efforts, along with employee donation matching and volunteer support.

Betsy Graseck says,

Net Interest Income (NII) Outlook and Net Interest Margin (NIM) Pressure

- The speaker highlights the pressure on Net Interest Margin, which is a key focus area as it could impact profitability.

- Despite NIM pressure, there is an expectation of increasing loan balances, suggesting positive momentum in loan growth.

- The potential removal of Quantitative Tightening (QT) and an increase in deposits are viewed as positive factors for NII.

- Investments in securities are being considered as part of the strategy to manage balance sheets effectively.

Loan Growth Opportunities

- The speaker inquires about sectors within the franchise that may experience loan growth inflection in the coming year.

- Identifying areas with potential for loan growth is critical to strategizing future expansion and maximizing returns.

- Understanding the order of drivers influencing loan growth will aid in prioritizing strategic investments.

Market Share and Strategic Positioning

- The speaker references the company’s market share as strong (“green”), indicating a leading position in several areas.

- They also point out areas with caution (“yellow”) and concern (“red”), which require strategic attention to improve market positioning.

- Identifying and addressing these ‘yellow’ and ‘red’ areas is crucial for maintaining competitive advantage and growth.

Balance Sheet and Fee Generative Opportunities

- Discussion includes identifying opportunities across the company’s balance sheet to optimize asset utilization.

- The speaker is interested in distinguishing whether growth will be more balance sheet-based or fee generative.

- Understanding the balance between these two growth avenues is vital for long-term financial health and strategic planning.

Q & A sessions,

Capital Strategy and Excess Utilization

- JPMorgan is focused on maintaining a significant reserve of extra capital, positioning for better deployment opportunities in the future.

- Despite having surplus capital now, the firm plans to prevent further growth in excess, potentially increasing capital returns through stock buybacks.

- While the current plan is to increase buybacks, the firm retains flexibility to change this strategy based on evolving market conditions.

Efficiency and Resource Allocation

- JPMorgan is optimizing productivity within technology teams to drive incremental efficiency.

- The company is focusing on maintaining a flat headcount to generate internal efficiencies, while exceptions remain in critical growth and risk areas.

- Efforts are ongoing to eliminate inefficiencies introduced by headcount growth over recent years.

Regulatory Framework and Compliance

- The firm advocates for a balanced regulatory environment that is supportive of economic growth and not overly burdensome on banks.

- JPMorgan is managing the Global Systemically Important Bank (G-SIB) buffer within acceptable limits, with little concern over seasonal variations.

- There’s an optimistic outlook towards improvements in the supervisory framework, especially around transparency and reducing bureaucratic burdens.

Financial Performance and Outlook

- Q4 net income reported at $14 billion, with an EPS of $4.81 and total revenue of $43.7 billion.

- Net Interest Income (NII) guidance for 2025 is approximately $90 billion, with potential sequential growth in H2 2025.

- The firm anticipates expense growth in 2025 driven by volume-related expenses, technology investments, and inflation pressures.

Loan Growth and Market Opportunities

- Potential loan growth is identified in acquisition finance, contingent on M&A activity resurgence.

- Card loan growth is expected to continue but at a slower pace compared to 2024.

- The affluent wealth management sector is targeted for expansion due to under-penetration.

| Metric | Q4 2024 |

|---|---|

| Net Income | $14 billion |

| EPS | $4.81 |

| Total Revenue | $43.7 billion |

| CET1 Ratio | 15.7% |

The analysis provided suggests a positive outlook for JPMorgan’s stock, driven by strategic capital management, robust efficiency measures, and potential loan growth opportunities, despite a challenging regulatory landscape.