The PNC Financial Services Group, Inc.

CEO : Mr. William S. Demchak

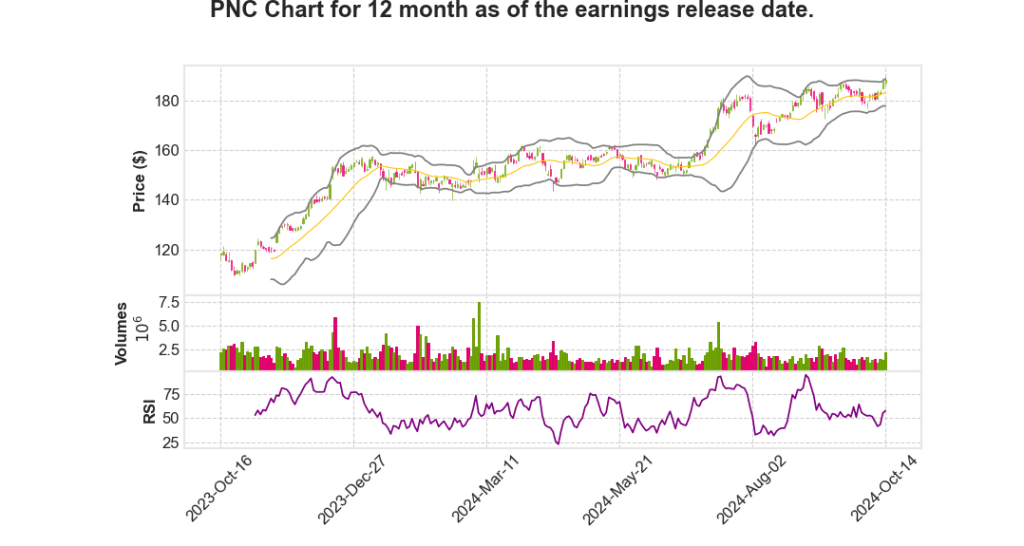

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q3 | 3.8% YoY | 203.0% | -2.8% | 2024-10-15 |

Rob Reilly says,

Balance Sheet and Capital Position

- Loans remained stable at $320 billion, while investment securities increased slightly by $1 billion or 1%.

- Cash balances at the Federal Reserve rose by $4 billion or 10% to $45 billion.

- Deposit balances grew by $5 billion or 1% to $422 billion, while borrowed funds decreased by $1 billion or 2%.

- Accumulated Other Comprehensive Income (AOCI) improved by $2.4 billion or 32%, ending the quarter at negative $5.1 billion.

- The estimated CET1 ratio increased to 10.3%, reflecting a strong capital position.

Loan Portfolio and Yields

- Average loan balances were stable at $320 billion, with commercial loans holding at $219 billion.

- The yield on total loans increased by 8 basis points to 6.13%.

- Investment securities yield rose by 24 basis points to 3.08%, influenced by higher rates on new purchases.

- Received fixed rate swaps totaled $33 billion, with the weighted average rate increasing by 58 basis points to 3.08%.

Income and Revenue Trends

- Net income for the third quarter was $1.5 billion or $3.49 per share.

- Total revenue increased by $21 million to $5.4 billion, driven by a 3% increase in net interest income.

- Fee income grew by $176 million or 10%, with capital markets and advisory fees increasing by 36%.

- Non-interest expense decreased by $30 million or 1%, resulting in positive operating leverage.

Credit and Reserve Metrics

- Non-performing loans increased by $75 million or 3%, primarily due to CRE office loans.

- Net loan charge-offs were $286 million, with an annualized net charge-offs ratio of 36 basis points.

- Allowance for credit loss was stable at $5.3 billion or 1.7% of total loans.

- CRE office criticized loans were stable, with NPLs rising slightly, and reserves on the office portfolio increased modestly.

Guidance and Outlook

- Expect continued economic growth in Q4 2024, with GDP growth of approximately 2% and unemployment slightly above 4%.

- Anticipate Federal Reserve rate cuts of 25 basis points in both November and December 2024.

- Forecast stable average loans in Q4 2024, with a 1% increase in net interest income and a 5% to 7% decrease in fee income.

- Expected non-interest expense to rise by 2% to 3%, with net charge-offs of approximately $300 million in Q4 2024.

| Quarter | Net Income ($ Billion) | Total Revenue ($ Billion) | Net Interest Income Increase | Fee Income Increase | Non-Interest Expense Change |

|---|---|---|---|---|---|

| Q3 2024 | 1.5 | 5.4 | 3% | 10% | -1% |

Overall, PNC’s solid performance in Q3 2024 and positive outlook for Q4 demonstrate strong financial management and strategic positioning in a challenging market environment.

Bill Demchak says,

Financial Performance Overview

- Net Income Achieved: PNC reported a net income of $1.5 billion for the third quarter, translating to $3.49 in diluted earnings per share.

- Positive Operating Leverage: This marks the third consecutive quarter of generating positive operating leverage, with expectations to maintain it for the full year of 2024.

- NII Growth: Net Interest Income (NII) grew by 3%, setting the pace for a projected record NII in 2025.

- Fee Income Increase: There was a notable 10% increase in fee income, bolstered by a robust performance in capital markets.

Franchise Growth and Activity

- CNIB Momentum: New loan production and commitments rose this quarter, with anticipated increased demand following recent Fed interest rate cuts.

- Retail Investments: Continued heavy investment in branch networks, particularly in high-growth Southwest markets, resulting in growing customer households and checking accounts.

- AMG Growth: Accelerated growth in markets with high opportunities, benefiting from favorable equity market conditions.

Credit Quality and Risk Management

- Stable Credit Quality: Overall credit quality remains stable due to strategic risk management and customer selection.

- CRE Office Segment: Despite expected additional charge-offs, reserves are deemed adequate.

Capital Strength and Strategic Outlook

- Tangible Book Value: An increase of 9% in tangible book value per share was achieved, supported by improvements in AOCI.

- Capital Levels: Strengthening of capital levels was noted during the quarter.

- Strategic Planning: Current organic growth opportunities are stated to be more attractive than ever, showing optimism in strategic outlook.

| Metric | Q3 2024 |

|---|---|

| Net Income | $1.5 billion |

| Diluted EPS | $3.49 |

| NII Growth | 3% |

| Fee Income Growth | 10% |

| Tangible Book Value Increase | 9% |

Q & A sessions,

Balance Sheet and Financial Position

- Loans remained stable at $320 billion, with no significant change from the previous quarter or year.

- Investment securities rose slightly by $1 billion or 1%.

- Cash balances at the Federal Reserve increased by $4 billion, reaching $45 billion, representing a 10% increase.

- Deposit balances grew by $5 billion or 1%, averaging $422 billion.

- Accumulated Other Comprehensive Income (AOCI) improved by $2.4 billion, or 32%, bringing it to negative $5.1 billion.

Income and Revenue Trends

- Net income for the third quarter was $1.5 billion or $3.49 per share.

- Total revenue increased by $21 million to $5.4 billion, driven by higher fee and net interest income.

- Net interest income grew by $108 million, or 3%, with a net interest margin of 2.64%, an increase of 4 basis points.

- Fee income increased significantly by $176 million, or 10%, linked quarter.

Future Guidance and Expectations

- Fourth quarter net interest income is expected to rise by approximately 1%.

- Fee income is predicted to decline by 5% to 7% due to elevated third-quarter capital markets and MSR levels.

- Other non-interest income is expected to range between $150 million and $200 million, excluding visa activity.

- Total non-interest expense is projected to increase by 2% to 3%.

- Fourth quarter net charge-offs are expected to be approximately $300 million.

Credit and Loan Quality

- Non-performing loans increased by $75 million or 3% linked quarter, mainly due to an increase in CRE office loans.

- Total delinquencies were stable at $1.3 billion, while net loan charge-offs rose to $286 million.

- Allowance for credit losses stood at $5.3 billion, or 1.7% of total loans.

- CRE office criticized loans remained stable, but NPLs increased due to loan migrations.

Capital and Shareholder Returns

- The CET1 ratio increased to 10.3% as of September 30.

- Approximately $800 million was returned to shareholders through dividends and share repurchases.

- Tangible book value per common share increased by 9% linked quarter, reaching approximately $97.

- The company remains well-capitalized and positioned for future growth with estimated positive operating leverage for the full year of 2024.