Regions Financial Corporation

CEO : Mr. John M. Turner Jr.

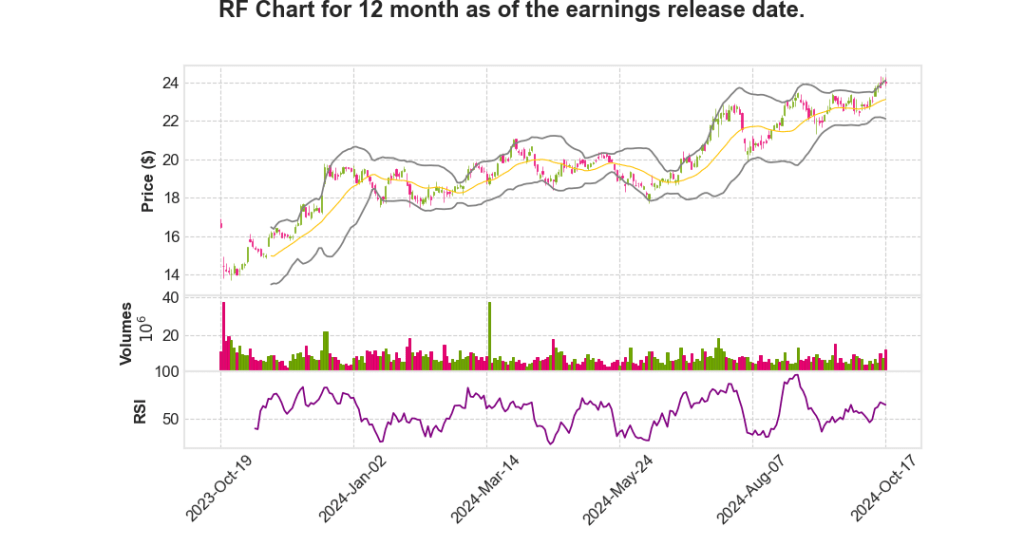

Quarterly earnings growth(YoY,%)

| Period | Revenue | Operating Income | EPS | Release Date |

|---|---|---|---|---|

| 2024 Q4 | -100.0% YoY | -100.0% | 48.7% | 2024-10-18 |

David Turner says,

Balance Sheet and Loans

- Average loans remained stable but showed a slight decline in ending loans on a sequential quarter basis.

- Average consumer loans were steady due to credit card growth being offset by declines in other areas.

- 2024 average loans are expected to be stable to down slightly compared to 2023.

- Deposit balances remained stable with a 1% decline in averages, aligning with typical consumer spending patterns.

Net Interest Income and Rate Management

- Net interest income rose by 3% from the previous quarter, reflecting stable deposit trends and asset yield improvements.

- Repositioning of $3.6 billion in securities resulted in $175 million pretax losses but is expected to pay off in 2.5 years.

- Interest-bearing deposit costs peaked at 2.34%, with a 43% beta, showcasing the strength of Regions’ deposit base.

- The exit rate for interest-bearing deposits at the quarter’s end was 2.2%, with the expectation of further reductions.

Adjusted Noninterest Income and Expense

- Adjusted noninterest income increased by 9%, with significant contributions from service charges, capital markets, and wealth management.

- Capital markets saw a 35% increase, primarily due to M&A advisory fees and securities underwriting improvements.

- Full-year 2024 adjusted noninterest income is anticipated to be between $2.45 billion and $2.5 billion.

- Adjusted noninterest expense grew by 4%, driven by a 6% rise in salaries and benefits.

- Full-year 2024 adjusted noninterest expenses are estimated at approximately $4.25 billion.

Asset Quality and Credit Performance

- Provision expense was $4 million less than net charge-offs at $113 million, with allowance for credit loss ratio increasing by one basis point to 1.79%.

- Net charge-offs as a percentage of average loans increased by 6 basis points to 48 basis points.

- Nonperforming loans as a percentage of total loans decreased by 2 basis points to 85 basis points.

- Full-year 2024 net charge-offs are expected to be at the upper end of the 40–50 basis point range.

Capital and Liquidity Management

- The estimated common equity Tier 1 ratio ended the quarter at 10.6%, with $101 million in share repurchases and $229 million in dividends.

- Adjusted common equity Tier 1 increased from 8.2% to 9.1%, showcasing the impact of lower interest rates and proactive duration management.

- A transfer of $2.5 billion from available-for-sale to held-to-maturity securities was made to reduce AOCI volatility.

- The maintained common equity Tier 1 ratio provides capital flexibility for regulatory changes and strategic growth.

John Turner says,

Earnings and Revenue Growth

- Third Quarter Earnings: Reported earnings of $446 million, resulting in earnings per share of $0.49.

- Total revenue grew on a reported and adjusted basis, driven by improvements in both net interest income and fee revenue.

- Most categories within fee revenue experienced growth compared to the second quarter, contributing to overall revenue increase.

Loan and Deposit Analysis

- Average loans remained stable, but ending loans declined slightly due to modest customer demand and portfolio adjustments.

- Average deposits saw a slight decline, while ending deposits remained steady, indicating stabilization in deposit remixing trends.

- Credit metrics have stabilized, despite some stress in certain corporate bank portfolios.

Customer Sentiment and Market Conditions

- Corporate customers are cautiously optimistic but are hesitating on capital expenditures due to economic and geopolitical uncertainties.

- Interest rate cuts are influencing customer behavior, yet many await further economic clarity post-election before making significant financial decisions.

Strategic Initiatives and Outlook

- Emphasis on understanding and meeting evolving customer needs through tailored solutions.

- Continued investment in talent, technology, and products to leverage future macroeconomic improvements.

- On track for a strong finish to 2024 with plans for sustained top-quartile results going into 2025.

Community Support and Disaster Response

- Active support in the recovery efforts for communities impacted by hurricanes Helene and Milton.

- Regions Bank has a history of aiding communities during natural disasters, reaffirming its commitment to support and recovery.

| Quarter | Earnings ($M) | Earnings Per Share ($) | Total Revenue Growth |

|---|---|---|---|

| Q3 2024 | 446 | 0.49 | Increased |

Overall, the report signals positive financial growth with stable credit conditions, while maintaining a strategic focus on future opportunities amidst external challenges.

Q & A sessions,

Deposit and Loan Performance

- Deposit Growth: Deposits have increased by 30% since pre-pandemic levels in 2019, highlighting a significant expansion in customer funds.

- Loans remained stable on average, with a slight decline in ending loans sequentially. Business loans also showed stability quarter-over-quarter.

- Deposit balances declined by 1% on average due to typical seasonal spending patterns.

- Noninterest-bearing deposits remained stable in the low 30% range, marking a consistent deposit structure.

Interest Income and Repositioning Strategy

- Net Interest Income Increase: A 3% increase in net interest income from the previous quarter surpassed expectations due to stable deposit trends and asset yield expansion.

- Repositioned $3.6 billion in securities, resulting in $175 million pretax losses with an expected 2.5-year payback period.

- Interest-bearing deposit costs remained flat at 2.34%, completing the rising rate cycle with a 43% deposit beta.

Noninterest Income and Expenses

- Noninterest Income Growth: A 9% increase in adjusted noninterest income, primarily driven by service charges (up 5%), capital markets (up 35%), and wealth management (up 5%).

- Full-year 2024 adjusted noninterest income is projected to be between $2.45 billion and $2.5 billion.

- Adjusted noninterest expenses rose by 4%, with a 6% increase in salaries and benefits due to one additional business day and performance-based incentives.

Asset Quality and Credit Performance

- Overall credit performance stabilized during the quarter, with nonperforming loans as a percentage of total loans declining by 2 basis points to 85 basis points.

- Provision expense was $4 million less than net charge-offs, with the allowance for credit loss ratio marginally increasing to 1.79%.

- Net charge-offs were towards the higher end of the 40-50 basis point range due to large credits within specific portfolios.

Capital and Liquidity Management

- Common Equity Tier 1 Ratio: Estimated at 10.6%, with improvements reflected in the AOCI adjustment from 8.2% to 9.1% from Q2 to Q3.

- $101 million in share repurchases and $229 million in common dividends were executed during the quarter.

- Transferred $2.5 billion of available-for-sale securities to held-to-maturity to reduce AOCI volatility.